AFRICA ENERGY SERIES: Misaligned Transition

Part 1 of 5: The Taxonomy Problem

AI-generated illustration: Firm Power With Time. Firm Power With Speed. Pick a Lane.

Misaligned Transition is a five-part series. Part 2: The China Ceiling (20 May). Part 3: Two Lanes (25 May). Part 4: Misaligned Capital (27 May). Part 5: Whose Transition? (1 June).

The series argues that capital labelled climate finance conflates four distinct functions, and that the conflation channels investment away from the firm power Africa requires to industrialise. It builds a corrective taxonomy, tests it against China’s energy stack and African firm power options, specifies what climate finance architecture for industrialisation actually requires, and examines whether instruments marketed as green transition capital serve African productive capacity or external consumption.

Capital labelled climate finance is arriving in African economies at growing scale. The World Bank Group and African Development Bank's joint Mission 300 programme targets 300 million new electricity connections by 2030. Just Energy Transition Partnerships have mobilised USD8.5 billion for South Africa alone, the vast majority as concessional loans, with approximately USD330 million in grants. The Loss and Damage Fund was operationalised at COP28. Clean energy investment in Africa reached approximately 2 per cent of the global total in 2024 (IEA, World Energy Investment 2025). Private sector clean energy investment rose from USD17 billion in 2019 to nearly USD40 billion in 2024, yet public and development finance institution funding fell by a third over the same period. The label is climate finance, and the flows are growing.

The outcomes are not following. Many African utilities remain financially weak because tariff structures, collection efficiency, losses, debt, and political pricing do not produce viable cash flows. Industrial energy capacity has not expanded at the pace the commitments imply. The IMF’s 2024 Staff Climate Note documents that electricity generation per capita in sub-Saharan Africa has trended downward over the past two decades, even as total installed capacity rose. More megawatts on paper. Yet fewer kilowatt-hours generated per person. From 2014 through 2023, African countries averaged only 1.4 gigawatts per year in new renewable energy offtake contracts procured through competitive auctions. Latin America averaged 4.4 gigawatts, India 14.9 gigawatts, and China 45 gigawatts over the same period. The arithmetic does not resolve unless the capital is building something other than what the label suggests.

The diagnosis is capital function mismatch. Climate finance is doing four distinct jobs that current architecture treats as one. The conflation produces outcomes inconsistent with any single one of those jobs done well. This essay builds the taxonomy that separates them and establishes the analytical scaffold against which the rest of this series reads empirical and policy material.

The question that governs all five parts is narrow: can Africa industrialise with the energy finance architecture currently on offer?

1. The Firm-Versus-Variable Distinction

The load-bearing distinction in energy economics is between firm power and variable energy. Current climate finance architecture does not make this distinction. The consequences are visible across the continent.

Firm power is electricity that can be dispatched on command, for as long as the system requires it. Combined-cycle gas turbines, hydroelectric reservoirs with storage capacity, nuclear reactors, geothermal plants, and coal-fired baseload all produce firm power. So do diesel generators, which remain the de facto firm power source for much of African industry. When the grid fails, the mine and the factory run on diesel at three to five times the cost of grid power. The operator calls on the generation asset and the asset delivers. The operator controls the schedule. Biomass and biogas provide dispatchable generation where feedstock supply is reliable, with approximately 1.9 gigawatts installed across Africa, concentrated in sugar mills and agricultural waste processing in Kenya, South Africa, and Mauritius. Seasonal feedstock availability and transport logistics constrain scaling beyond niche applications.

Variable energy is electricity that arrives when ambient conditions permit. Solar photovoltaic generates when the sun shines. Wind turbines generate when the wind blows. Run-of-river hydro generates when the river flows. The resource controls the schedule. Offshore wind is planned in South Africa but has no operational capacity on the continent. High capital cost, the absence of local fabrication and port infrastructure, and deep-water conditions along most of the African coastline have prevented deployment. Concentrated solar power with thermal storage, such as Morocco’s 580 megawatt Noor-Ouarzazate complex, partially bridges the gap by storing heat for dispatch after sunset, but the technology remains limited to a handful of sites globally.

The distinction matters because industrial production requires firm power. A copper smelter in Kitwe cannot pause its furnace when clouds roll over the Copperbelt. Large Zambian mines already rely on ZESCO hydro plus diesel backup precisely because variable supply alone cannot meet process-heat schedules. No credible energy planner proposes running smelters on unfirmed solar. The question is whether climate finance architecture directs sufficient capital toward the firm power that smelters require. Or whether the green label channels capital exclusively into variable generation and leaves the firm power gap to diesel.

Ferrochrome, steel, cement, fertiliser, glass, paper: every absorption industry that transforms raw material into intermediate or finished product runs on scheduled, dispatchable electricity. Industrial demand is constant or programmable. Variable supply against constant demand requires either storage at durations and costs not yet viable for continuous industrial loads in African grid conditions, or backup firm power running alongside the variable source. The backup defeats the cost logic of the variable investment.

Battery technology is advancing on multiple fronts. Lithium iron phosphate already commands 40 per cent of the global battery market with zero cobalt content. Sodium-ion eliminates lithium entirely. Iron-air systems capable of 100-hour storage completed their first grid-connected pilot in 2026. At 4-hour duration, solar plus storage is already cost-competitive with gas peakers for grid balancing, with IRENA reporting levelised costs of USD54 to USD82 per megawatt-hour in high-irradiance regions. Gas peaking plants in African markets run at USD100 to USD150 per megawatt-hour depending on fuel logistics and sovereign risk premiums. Industrial diesel backup, the actual baseline for most African manufacturers when the grid fails, costs USD200 to USD400 per megawatt-hour. The spread is the argument: firm gas at a third of diesel cost is immediate improvement, and solar plus storage undercuts both for grid balancing. At 8-hour duration, it displaces diesel backup for commercial premises at lower lifetime cost. Africa’s installed battery storage capacity reached 1.64 gigawatt-hours in 2024, a tenfold increase in a single year. The cost trajectory is steep and the direction is clear.

But extending the dispatch window does not eliminate the resource dependency. A battery stores energy that the sun must first generate. During Zambia’s rainy season, consecutive days of heavy cloud cover deplete any economically sized battery bank with no mechanism to recharge. Geothermal taps continuous subsurface heat. Nuclear carries fuel loaded for 18 to 24 months. Gas stores fuel in tanks and pipelines. These three are genuinely weather-independent. Hydro with reservoir is firm on daily and weekly dispatch but vulnerable on seasonal timescales. Zambia’s 2024 drought reduced Kariba and Kafue Gorge water levels to crisis points, triggering over 12 hours of daily load-shedding despite decades of reservoir storage. The lesson is that dependence on any single firm power source creates fragility, and extreme weather events are growing more frequent across the continent. Diversified firm power (gas alongside hydro, geothermal alongside both) is the architecture that weathers daily intermittency, multi-year drought, and the severe weather patterns that operating conditions increasingly demand. Solar plus storage carries hours of autonomy and a dependency on tomorrow’s sun.

Pumped hydroelectric storage provides grid-scale storage with minimal weather dependency: it cycles the same water between upper and lower reservoirs rather than consuming river flow, making it far less drought-sensitive than conventional hydro. Closed-loop systems that use artificial reservoirs are largely insulated from seasonal rainfall variation, though open-loop systems connected to rivers retain some exposure. Africa has 3,726 megawatts of installed pumped storage capacity, predominantly in South Africa (Ingula at 1,332 megawatts, Drakensberg at 1,000 megawatts, Palmiet, Steenbras) and Morocco (Afourer). Egypt’s 2,400 megawatt Ataqa project and Lesotho’s 1,200 megawatt Kobong scheme are under development. Suitable sites are more broadly available than commonly assumed. Closed-loop systems build two artificial reservoirs connected by a tunnel and need elevation differential and stable geology rather than a flowing river. Global mapping studies have identified thousands of potential sites across African highlands. The constraint is project-level preparation. The detailed feasibility studies, geological assessments, and engineering design that turn an identified site into a bankable project have been completed for very few locations outside South Africa and Morocco.

The question for African policymakers is whether industrialisation decisions can wait for long-duration storage to close the firmness gap. A gas plant commissioned in 2027 operates for 20 years. During its first decade, it provides firm power that no storage technology yet delivers at scale for continuous industrial loads. During its second decade, it may face competition from maturing storage. The stranded asset risk in the final years is a genuine constraint. But the stranded economy risk, deferring industrialisation while waiting for a cost crossover that keeps moving, is worse. China and India are building both simultaneously: gas and coal for industrialisation today, battery manufacturing for the system that replaces it tomorrow. The climate finance architecture asks Africa to build neither the firm power it needs now nor the storage manufacturing capacity it will need later. When long-duration storage reaches the cost and duration threshold to serve continuous industrial loads through multi-day weather events, that technology belongs in Firm Power Finance. The category follows the function, not the fuel.

China demonstrates the complementarity empirically. In 2024, Chinese industrial planners approved USD625 billion in clean energy investment alongside USD54 billion in new coal capacity. Both at scale. Both simultaneously. Part 2 of this series develops the case in full.

Germany demonstrates what happens when the complementarity is broken. The Energiewende invested heavily in solar and wind while shutting down the country’s nuclear fleet and increasing dependence on Russian gas for firm backup. When Russian gas was severed in 2022, Germany restarted coal plants, built emergency LNG terminals, and watched industrial electricity prices drive manufacturing investment offshore. The taxonomy names the error precisely: Germany funded Energy Volume Finance while dismantling Firm Power Finance, and the consequences were industrial. The United States runs the opposite approach: the Inflation Reduction Act channels USD369 billion into clean energy while nuclear plant operating licences are extended to 80 years and the gas fleet is maintained. The US funds both lanes.

Household consumption is fundamentally different. Domestic lighting, refrigeration, mobile phone charging, and small appliance use can tolerate intermittency or operate on storage at household scale. A 5 kWh lithium battery paired with a rooftop solar panel serves a household in Kisumu or Lusaka at meaningful penetration. Kenya’s electrification rate rose from 36 per cent in 2014 to over 75 per cent by 2024. The breakdown: 65 per cent on-grid, 0.84 per cent mini-grid, and 9.2 per cent standalone solar (World Bank, Tracking SDG7; Kenya Mission 300 Compact). That is Access Finance delivering household access.

Consider what this means operationally. Kenya has positioned itself as East Africa’s data centre hub. In May 2024, Microsoft and G42 announced a USD1 billion geothermal-powered data centre at Olkaria, with Phase 1 at 100 megawatts and a long-term target of 1 gigawatt. By May 2026, the project had stalled. President Ruto told the Kenyan diaspora: “One data centre requires 1,000 megawatts. Yet, as a whole country, we only have 2,300 megawatts.” Kenya’s total grid-connected installed capacity stands at 3,192 megawatts. Peak demand reached 2,444 megawatts in January 2026. A single hyperscale campus at full build-out would have drawn roughly 41 per cent of national peak demand, or a third of total installed capacity.

The pitch rested on geothermal expansion. The East African Rift holds an estimated 10,000 megawatts of geothermal resource. The Kenyan government targets 5,000 megawatts by 2030, building on the existing 950 megawatts at Olkaria and surrounding fields. Geothermal runs at over 90 per cent capacity factor regardless of weather. The promise of future firm power attracted the investment. The capital to build that expansion has not followed.

At 950 megawatts, existing geothermal accounts for approximately 40 per cent of national generation but cannot serve current demand and a gigawatt-scale facility simultaneously. Kenya Power’s financial and operational constraints compound the problem. Customers averaged 8.39 hours of outages per month in the second half of 2025, more than five times the regulatory benchmark of 1.50 hours (EPRA Biannual Report, March 2026). The grid cannot deliver reliably what the existing fleet generates, let alone what a hyperscale campus would require.

The payment and guarantee negotiations that stalled the project trace directly to the Firm Power Finance gap. Microsoft needed a bankable power purchase agreement backed by guaranteed geothermal supply. KenGen cannot guarantee power from capacity that has not been built. The Treasury has not approved the capital to build it. The chain broke at the firm power link.

Smaller projects are proceeding where the math holds. EcoCloud is developing a 60 megawatt geothermal-powered facility at the same Olkaria site, sized to current generation. Nxtra is building a 44 megawatt data centre at Tatu City in Kiambu County just outside Nairobi. Both fit within existing capacity. Neither anchors hyperscale ambition.

Existing firm power enabled the pitch. Expanding that firm power to match industrial ambition required Firm Power Finance at a scale that has not arrived.

Solar photovoltaic levelised costs have fallen 90 per cent since 2010 (IRENA), the most dramatic cost decline in energy history. Solar can be cheapest at plant gate and still insufficient at system level if dispatchability, storage, transmission, and backup are not priced. Africa’s cumulative installed solar photovoltaic capacity (excluding residential off-grid systems) reached 19.2 gigawatts by end-2024. Wind capacity stood at approximately 8.7 gigawatts across only 15 of 42 tracked African countries, with South Africa, Egypt, Morocco, and Kenya accounting for 90 per cent of the total. Africa added approximately 2.5 gigawatts of solar in 2024, roughly 0.5 per cent of the more than 500 gigawatts deployed globally that year. Nearly 80 per cent of those African solar additions came from two countries: South Africa and Egypt.

South Africa’s dominance is instructive. Before the crisis, renewable deployment was orderly and modest, procured through the REIPPPP auction programme. Then Eskom’s ageing coal fleet degraded. Availability dropped below 60 per cent. Stage 6 load shedding became routine from 2022 to 2024. The government responded by removing generator licensing thresholds in January 2023. In March 2023 it introduced Section 12BA, a two-year emergency tax incentive allowing 125 per cent first-year deduction of renewables investment costs. The incentive expired in February 2025 and was not renewed. At the 27 per cent corporate tax rate, the incentive covered roughly a third of the capital cost through foregone revenue. The C&I solar and battery boom that followed was a crisis response funded by private capital but subsidised through the tax code. Firms installed solar because the grid could not keep the lights on, and the fiscus bore part of the cost through the tax code. Variable energy scaled as a direct consequence of firm power failure.

The taxonomy reads this correctly: when firm power collapses, private capital fills the gap with whatever is fastest to deploy. That is an emergency response to institutional failure. If the deployment produces household access and commercial self-consumption, it is well-targeted. If it is supposed to produce industrial firm power for the absorption industries that drive economic transformation, it is categorically misaligned.

2. A Corrective Finance Taxonomy

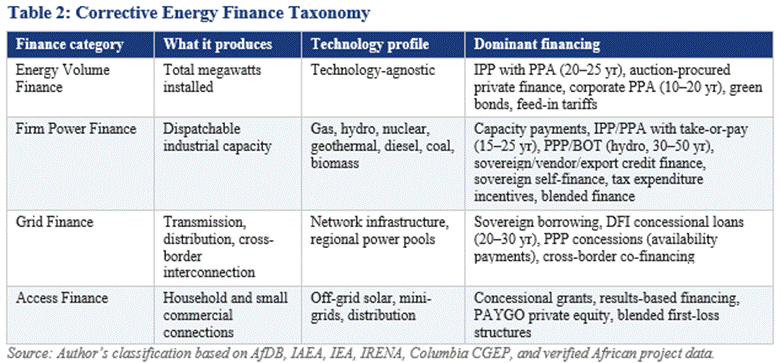

Current climate finance labelling conflates four functions that require different capital structures and risk profiles, operate on different time horizons, and demand different institutional architectures. The firm-versus-variable distinction is established in energy economics. The IEA, IRENA, and AfDB already separate baseload from variable and grid-connected from off-grid in their research frameworks. The contribution is the financial mapping. It maps each energy function to its capital structure, risk bearer, tenor, and industrialisation outcome. The conflation the taxonomy addresses is a capital allocation problem that existing research classifications leave unaddressed. A green bond or blended finance vehicle does not ask whether its proceeds finance firm power or variable energy. It asks whether the project qualifies under the green taxonomy. Naming the four functions is the first step toward capital flows that match mechanism to outcome.

Energy Volume Finance is capital for total energy supply expansion. It targets megawatts installed across all generation types. It does not distinguish between firm and variable. Mission 300 sits primarily in this category. The African Union, building on the African Development Bank’s energy compact, has endorsed a target of 300 gigawatts of renewable capacity online by 2030. Total installed renewable capacity (including large hydropower, which accounts for approximately half the total) stood at 72 gigawatts at the end of 2023. Annual renewable capacity additions averaged approximately 8 gigawatts in 2023. Meeting the target requires annual deployment to rise to over 30 gigawatts per year for the remainder of the decade. The ambition is clear, and the gap is vast. The category does not specify what the megawatts produce once installed.

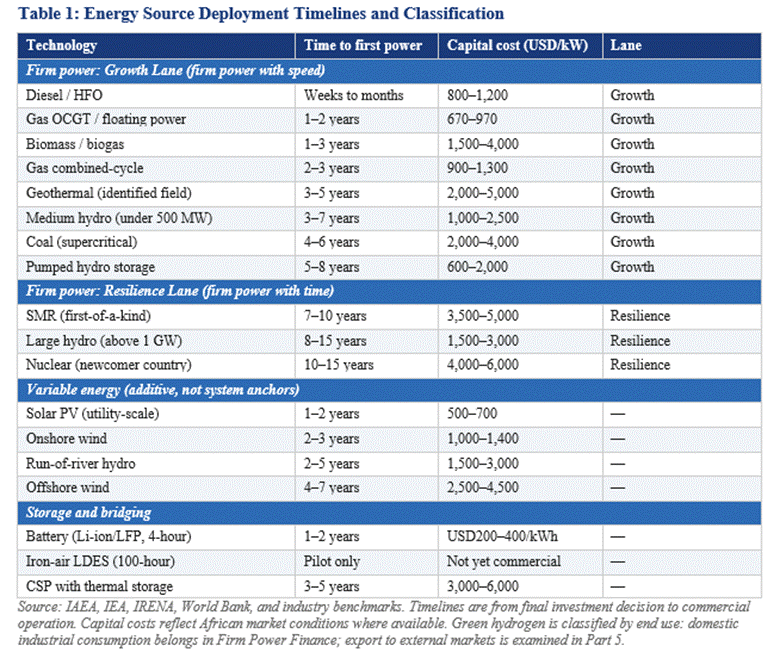

Firm Power Finance is capital for dispatchable generation that runs on command. Gas, hydro with storage, nuclear, geothermal. It targets industrial demand, grid reliability, and the absorption-industry capacity that drives economic transformation. Within this category, deployment timelines differ by an order of magnitude. Gas open-cycle turbines and floating power ships can deliver in 1 to 2 years. Gas combined-cycle plants commission in 2 to 3 years. Geothermal fields with completed exploration produce power in 3 to 5 years. Pumped hydroelectric storage takes 5 to 8 years. Nuclear programmes in newcomer countries take 10 to 15 years from decision to first power. This creates two lanes within firm power. The Growth Lane delivers firm power with speed: gas, geothermal from identified fields, medium hydro, and pumped hydro can serve industrialisation decisions being made this decade. The Resilience Lane delivers firm power with time: nuclear and large-scale hydro above 1 gigawatt position economies for sovereign energy security in the decades beyond.

Firm Power Finance is currently the most underfunded category in African climate finance flows. The green label discourages investment in dispatchable fossil generation regardless of African industrial context. It also underweights nuclear and geothermal, which carry long development timelines that do not match the disbursement cycles of most climate finance vehicles. Gas carries an additional vulnerability: fuel supply. Countries with domestic gas production (Nigeria, Mozambique, Senegal, Algeria, Angola, Ghana) can draw on an internal resource. Countries without domestic gas must import LNG, exposing them to global price volatility, maritime supply chain disruption, and hard currency drain. The Strait of Hormuz crisis demonstrated how fast LNG supply can be constrained. This fuel dependency reinforces the case for sources that carry their energy input on the continent. Nuclear fuel is loaded for 18 to 24 months. Pumped hydro uses water. Geothermal draws on subsurface heat, but only where the geology permits (principally the East African Rift). Countries without domestic gas, without geothermal potential, and without suitable pumped hydro sites face the hardest version of the firm power problem. Their fastest path to industrialisation runs through imported fuel that the global system can disrupt at any time.

The institutional intent for firm power is present in every African sub-region. More than 20 African countries are engaging the nuclear pathway at different levels of seriousness through the IAEA Milestones framework. This count excludes South Africa, which already operates nuclear power, and Egypt, which is constructing a four-unit 4.8 gigawatt plant at El Dabaa with the first unit expected operational in 2028. Ghana, Kenya, and Nigeria have taken firm decisions to pursue nuclear power. Ten more countries are in the decision-making stage. Small modular reactors offer potentially shorter construction timelines and smaller capital commitments. The IAEA tracks more than 80 designs, with only 4 units operational globally across 2 designs (Russia and China). First-of-a-kind deployment in newcomer countries remains 7 to 10 years away. In June 2025, the IAEA and the World Bank formalised a partnership for nuclear energy for development, the World Bank’s first formal engagement with nuclear power in decades. The institutional architecture is shifting. The capital labelling has not. Climate finance vehicles that exclude nuclear and restrict gas do not finance the firm power options that several African countries are now actively pursuing.

Grid Finance is capital for transmission, distribution, and grid integration infrastructure. It is the connective tissue that allows generation to reach demand, including across borders. Variable energy at scale requires grid investment that variable energy projects themselves do not finance. A 50 megawatt solar farm in southern Zambia produces electrons. Without transmission infrastructure connecting the farm to the Copperbelt industrial load 400 kilometres north, the electrons do not reach the smelter. The generation asset exists. The industrial demand exists. The grid between them does not. This constraint binds across most sub-Saharan African power systems where generation investment has outpaced network investment for over a decade. Transmission and distribution losses average approximately 19 per cent across the 43 markets tracked by the AfDB Electricity Regulatory Index, with the weakest systems exceeding 30 per cent.

Cross-border interconnectors and regional power pools (SAPP, EAPP, WAPP) are the mechanism through which countries without domestic firm power can access it from neighbours. The Ethiopia-Kenya HVDC interconnector carries GERD hydro to East African demand. Mozambique’s gas-fired generation can serve Zambia and Zimbabwe through SAPP. These regional links directly address the trap named above: countries can import firm power from a neighbour that has it. Grid Finance at the regional scale is as critical as Grid Finance at the national scale, and both are chronically underfunded.

Private industrial self-generation is emerging as a parallel path. Dangote’s Lagos refinery built its own 435 megawatt CCGT rather than depending on Nigeria’s grid. If a similar refinery is developed in Mombasa or Tanga, as is being discussed, it would likely build its own gas-fired power from East African gas reserves. This is Firm Power Finance delivered through private industrial capital, bypassing the insolvent utility entirely.

Access Finance is capital for last-mile connection of households and small commercial users to electricity service. Mission 300 sits partially here. Off-grid solar, mini-grids, distribution network extension, metering and billing infrastructure. The connections are different from the upstream generation question. Access Finance is concessional capital because household connection economics do not support commercial returns at the lowest-income tiers. Commercial and industrial self-consumption has become a significant part of Africa’s solar deployment, with behind-the-meter systems bypassing grid constraints. Access Finance deserves continued and expanded funding on its own terms.

What it does not deserve is the label of industrialisation finance. According to IRENA and the AfDB (2022), only 2 per cent of global renewable energy investment over the past two decades was directed to Africa. Even within that thin slice, the allocation is concentrated in Energy Volume and Access categories. Firm Power Finance and Grid Finance together receive a fraction of the fraction. Table 2 summarises the four categories.

The financing mechanisms matter because they determine who bears the risk and at what price. The Independent Power Producer model, in which a private developer builds and operates generation under a long-term Power Purchase Agreement with a government utility, has become the dominant structure for new renewable capacity across Africa. South Africa’s REIPPPP has procured over 6 gigawatts through competitive auctions. Kenya’s geothermal expansion was financed through IPP structures. Egypt’s solar and wind auctions follow the same model. But the IPP model depends on the creditworthiness of the off-taking utility. When the utility is insolvent, the PPA is a sovereign contingent liability, not a bankable contract. Capital cannot flow into generation faster than the utility can absorb it without creating stranded contractual obligations.

Nuclear and large hydro require different structures entirely. Egypt’s El Dabaa plant is financed through sovereign vendor finance from the Russian Federation, with concessional terms that no private capital market would offer for a first nuclear programme. Ethiopia’s Grand Ethiopian Renaissance Dam, inaugurated in September 2025 with over 5 gigawatts of firm hydroelectric capacity, was financed primarily through domestic sovereign resources and bonds. Large hydroelectric concessions in Zambia and Mozambique operate under PPP or build-operate-transfer structures with 30 to 50 year horizons. Grid Finance has its own models. In December 2025, the Kenya Electricity Transmission Company signed a USD311 million PPP with Africa50 and Power Grid Corporation of India. The deal finances, builds, and operates high-voltage transmission lines under a 30-year concession with availability payments. That project does not finance generation. It finances the connective tissue without which generation assets remain stranded. Table 2 reflects what is actually being deployed in African energy markets.

The sequencing argument that runs through this series is not new to Canary Compass. In December 2025, “EVs Are the Last Mile, Not the First Mile” made the case that binding constraints must close before consumer technologies deploy. The same logic applies here. Firm power and grid infrastructure must close before the label architecture that finances variable deployment can produce industrialisation outcomes.

A taxonomy that classifies gas, coal, and diesel alongside nuclear and geothermal in Firm Power Finance invites the emission question, and it should be answered directly. Africa contributes roughly 3 to 4 per cent of cumulative global greenhouse gas emissions while bearing disproportionate climate impact. Requiring African economies to decarbonise their industrial energy supply before they have industrialised is a constraint that no currently industrialised economy accepted during its own transformation. The taxonomy sequences emission reduction inside the industrialisation pathway. Gas displacing diesel today produces an immediate reduction in emission intensity per kilowatt-hour delivered. Nuclear and geothermal displacing gas over the medium term produces decarbonisation at the generation level. Variable renewables scale as grid capacity and storage economics permit. The emission pathway sits inside the industrialisation pathway.

Green hydrogen illustrates the taxonomy at work. Namibia, Egypt, Mauritania, Kenya, and Morocco all have active hydrogen strategies, and several of the largest single investment commitments on the continent are hydrogen projects classified as climate finance. The taxonomy classifies hydrogen by function: produced in Africa and consumed in African industry (fertiliser, steel, stored firm power), it belongs in Firm Power Finance. Produced in Africa and exported to Europe, it is resource extraction under a green label, converting African land, solar irradiance, and water into an energy commodity for external consumption. The distinction between domestic industrial use and export extraction determines whether hydrogen investment builds African productive capacity or repeats the mineral pattern this series diagnoses.

3. The Regulatory Parallel

The African Development Bank’s Electricity Regulatory Index offers an instructive parallel. The ERI tracks governance and regulatory reform across 43 African electricity markets. The 2024 edition documents meaningful progress: 41 of 43 countries scored above 0.5 on the governance index, up from 24 in 2022, and the regulatory outcomes index improved from 0.40 to 0.62. Tariff reforms have been implemented and governance structures established across most markets.

Yet utility financial performance has not closed the gap. Financial viability remains elusive. Enforcement remains weak.

The ERI finding is that reform implementation does not equal performance outcome. Both regulatory reform and climate finance deployment can show visible progress while leaving the binding constraint intact. For the ERI, the underlying constraint is utility financial viability: tariff reform without collection efficiency improvement produces a reformed tariff that nobody pays. Governance reform without financial viability produces a well-governed utility that cannot service its debt. The utility remains dependent on government transfers that compete with health, education, and infrastructure spending.

For climate finance, the equivalent constraint is the conflation of four functions that require different capital. Capital labelled climate finance enters Energy Volume and Access categories because the green label accommodates them. Firm Power Finance and Grid Finance, the categories that industrialisation requires, remain chronically underfunded because the label architecture does not accommodate them. In both cases, the mechanism addresses the visible surface while leaving the underlying constraint in place. The failure is one of sequence.

4. What the Taxonomy Holds

The taxonomy names a mismatch that aggregate labels conceal. Capital that enters Africa under the climate finance label funds four distinct functions. Two of those functions serve industrialisation. The current architecture systematically underfunds both. That is Part 1’s finding.

The firm-versus-variable distinction is not a technology preference. It is an analytical instrument. The corrective finance taxonomy operates as a diagnostic framework built for the decade in which African industrialisation either happens or does not. Climate finance cannot be assessed by label or megawatts alone. It must be assessed by the function it finances.

Part 2 tests the taxonomy against China’s energy system, where USD625 billion in clean energy investment and USD54 billion in new coal capacity were approved in the same year, both serving functions the taxonomy names. Part 3 applies it to African firm power options across both lanes, naming five fallacies that dominate current energy transition discourse. Part 4 diagnoses the capital architecture and specifies what climate finance for African industrialisation actually requires if it is taken at its word. Part 5 tests the taxonomy against three instruments that channel capital into Africa under green labels: carbon credits, hydrogen export corridors, and external land acquisitions.

The taxonomy is the scaffold. What follows is the test.

Sources

African Development Bank, Electricity Regulatory Index for Africa 2024 (Abidjan, 2024).

Africa Solar Industry Association, Africa Solar Outlook 2025 (Brussels, January 2025).

Bloomberg New Energy Finance, Africa Power Transition Factbook 2024 (London, September 2024).

Columbia University SIPA Center on Global Energy Policy, Public-Private Partnerships in the African Energy Sector (New York, September 2025).

Global Wind Energy Council, Global Wind Report 2025 (Brussels, April 2025).

International Atomic Energy Agency, Outlook for Nuclear Energy in Africa (Vienna, July 2025).

International Energy Agency, World Energy Investment 2025 (Paris, 2025).

International Monetary Fund, Harnessing Renewables in Sub-Saharan Africa: Barriers, Reforms, and Economic Prospects, Staff Climate Note 2024/005 (Washington, DC, 2024).

IRENA, 24/7 Renewables: The Economics of Firm Solar and Wind (Abu Dhabi, May 2026).

IRENA, Renewable Power Generation Costs in 2024 (Abu Dhabi, 2025).

IRENA and AfDB, Renewable Energy Market Analysis: Africa and Its Regions (Abu Dhabi and Abidjan, January 2022).

World Bank, Tracking SDG7: The Energy Progress Report (Washington, DC, various years).

Disclaimer

This article does not constitute legal, financial, or investment advice. The author shares views for perspective and discussion only. Do not rely on them as a substitute for professional advice tailored to your specific circumstances. Always consult a qualified legal, financial, investment, or other professional adviser before making decisions based on this content. The analysis reflects proprietary research undertaken by Canary Compass and the author.

Canary Compass and the author accept no liability for actions taken or not taken based on the information in this article.

The views expressed in this article represent the author’s independent professional analysis and do not constitute an endorsement of any individual, institution, or position. Canary Compass and the author accept no responsibility for how this content is interpreted, excerpted, or recontextualised by third parties not involved in its production and publication. Reproducing any portion of this work in isolation, or in combination with other material, in a manner that misrepresents the author’s original meaning constitutes a distortion of the published record.

The author may hold positions in financial instruments, currencies, or assets discussed or referenced in this publication. Such positions do not constitute a recommendation to buy or sell.

All views, projections, and forecasts reflect the author’s assessment at the time of writing. Data sourced from third parties is believed to be reliable but has not been independently verified. Past performance does not indicate future results.

All content published by Canary Compass is the intellectual property of the author. Reproduction, adaptation, or redistribution, in whole or in part, requires written permission.

About the Author

Dean N. Onyambu is the Founder and Chief Editor of Canary Compass, a financial research publication focused on African monetary architecture and financial sovereignty. He brings 18 years of experience across trading, fund leadership, and economic policy, with senior roles at Standard Bank, First Capital Bank, and Opportunik Global Fund.

Read and subscribe at www.canarycompass.com.

The Canary Compass Channel is available on @CanaryCompassWhatsApp for economic and financial market updates on the go.

For more insights from Dean, you can follow him on LinkedIn @DeanNOnyambu or X @InfinitelyDean.