AFRICA ENERGY SERIES: Misaligned Transition

Part 4 of 5: Misaligned Capital

AI-illustration: Two Rivers, One Desert

Misaligned Transition is a five-part series. Part 1: The Taxonomy Problem (18 May). Part 2: The China Ceiling (22 May). Part 3: Two Lanes (26 May). Part 5: Whose Transition? (1 June).

In 2024, Zambia’s worst drought in two decades reduced Kariba and Kafue Gorge to crisis levels. CNMC (China Nonferrous Metal Mining) Chambishi copper smelter, with annual output of a reported 250,000 tonnes, lost an estimated 20 per cent of production capacity during the crisis. Part 1 stated the principle: a copper smelter cannot pause its furnace when clouds roll over the Copperbelt. The operational reality is more precise. A furnace operating above 1,100 degrees Celsius cannot be switched off without risking permanent damage to the refractory lining. Operators reduce feed rate and processing volume while keeping the furnace hot. The cost at Chambishi was not a diesel fuel bill. It was lost copper: output that was never smelted, revenue that was never earned, industrial capacity that sat idle because the firm power base did not hold.

Part 1 documented diesel as the de facto firm power source for much of African industry. The continental picture is more precise than that formulation allowed. In Nigeria, where the grid delivers roughly a third of 13 installed gigawatts and collapsed around 12 times in 2024, an estimated 22 million generators operate across the economy. Industrial and commercial users run diesel as primary power rather than backup. In most other African economies, diesel serves as backup during grid failures. Chambishi did not run diesel. It lost output. Part 2 estimated the cost at USD1.3 billion per decade for a single facility running entirely on diesel versus gas. That figure is an upper bound. The real cost combines production losses during outages, diesel backup when the grid fails, and capital diverted from productive investment into energy self-provision. Across the border from Chambishi, the Kamoa-Kakula copper complex invested in 180 megawatts of diesel backup alongside 250 megawatts of refurbished hydro and 60 megawatts of solar-plus-storage under construction. The firm power gap costs African industry in two currencies: lost production for those who cannot afford backup, and capital diverted from productive investment for those who can.

Nigeria holds 215 trillion cubic feet of proven gas reserves. In 2025, the Nigerian government issued its Series III sovereign green bond, targeting 50 billion naira for renewable mini-grids, afforestation, and solar utilities. Not for gas-to-power. The bond worked as designed. The design does not match the need. Parts 1 through 3 built the diagnosis. This essay specifies the corrective. It requires both international architecture reform and domestic governance reform. The binding constraint is not identical across countries. Label reform is the cross-border capital architecture constraint. Utility reform, payment discipline, project preparation, transmission, and fuel infrastructure determine whether that capital can land. The label restricts the supply of capital. Governance determines the absorption of capital.

1. Three Reforms

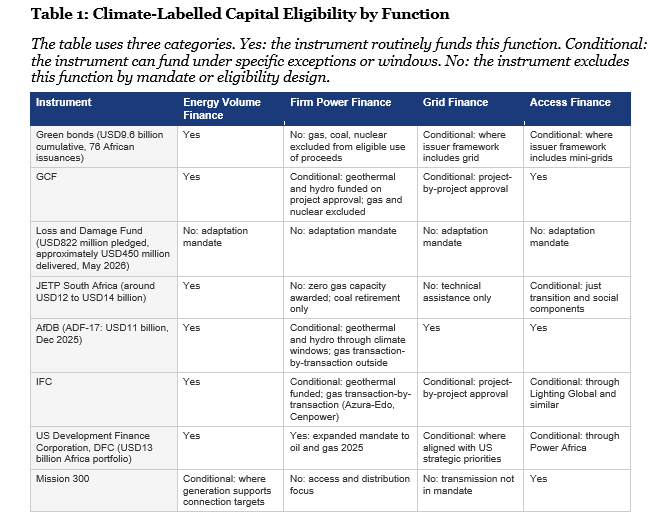

Part 1’s Table 2 specified the instruments Firm Power Finance requires. Capacity payments. Independent power producer and power purchase agreement (IPP/PPA) structures with take-or-pay at 15 to 25 year tenor. Public-private partnership and build-operate-transfer (PPP/BOT) structures for hydro at 30 to 50 years. Sovereign and vendor finance. Sovereign self-finance. Tax expenditure incentives. Blended finance. These instruments exist. The label architecture that would permit their deployment at programmatic scale does not. Three reforms unlock it. The green bond market has mobilised USD9.6 billion across 76 African issuances. Together with the Green Climate Fund (GCF), the Climate Investment Funds (CIF), and Just Energy Transition Partnership (JETP) vehicles, these instruments represent the fastest-growing pool of labelled climate capital available to African energy. Label reform would make Firm Power Finance eligible for this pool.

Label reform. Most climate-labelled capital pools either exclude unabated gas outright, treat it as politically unbankable, or lack a function-based transition category under which African gas-to-power can qualify. The International Finance Corporation (IFC) and Social Investment Managers and Advisors (SIMA) issued a USD150 million solar green bond for Africa. The Copperbelt Energy Corporation (CEC) green bond on the Zambian Copperbelt and Nigeria’s sovereign green bond also deployed in Energy Volume Finance. The green bond market’s eligibility conventions exclude gas from the credible use of proceeds. The label architecture comprises multiple governance structures: EU taxonomy criteria, GCF investment policy, CIF allocation rules, International Capital Market Association (ICMA) green bond principles, and individual development finance institution (DFI) board mandates. Reform must operate across them.

The exclusion is not universal. Individual DFIs maintain gas windows outside their climate-labelled portfolios. IFC backed Azura-Edo in Nigeria (461 megawatts). The AfDB financed Kribi in Cameroon (216 megawatts) and Kpone in Ghana (300 megawatts). Three named projects across a decade, totalling under 1,000 megawatts. Variable energy procurement through South Africa’s Renewable Energy Independent Power Producer Procurement Programme (REIPPPP) alone produced six times that in one country. The instruments growing fastest are the instruments that exclude Firm Power Finance most completely.

The corrective is time-bound transition finance for gas-to-power in countries with domestic reserves. The parameters must be specific. A window of no more than 15 years during which new gas-to-power projects can qualify for the reformed label. Fifteen years is long enough for three project cycles from conception to commissioning and short enough for the window to close as clean firm alternatives approach bankability at African WACC. An emission intensity threshold that demonstrates material improvement over the generation source being displaced or over the realistic alternative the country would otherwise deploy. Eligibility that extends until clean firm alternatives reach bankability at African weighted average cost of capital (WACC), with the 15-year window as a minimum guarantee to investors. Flexible power purchase agreement (PPA) structures with early-retirement provisions, including termination payments covering outstanding debt and a reasonable equity return, would protect investors against early retirement.

This is not an external prescription. The African Union’s Common Position on Energy Access and Transition explicitly identifies natural gas and nuclear as playing a crucial role in expanding modern energy access. The Position was shaped principally by gas-producing member states, but it was endorsed by the full AU membership including non-producers. The series articulates at instrument level what African institutional voices have already stated at the political level.

Within the current architecture, capital allocators directing funds toward variable energy are acting rationally. Variable projects are faster to permit, carry lower execution risk, and access favourable terms that gas cannot. The EU taxonomy already accommodates transitional activities. Extending comparable treatment to African gas within climate-labelled instruments would open the fastest-growing capital pool to a category it currently excludes. Eligibility should require satellite methane monitoring, no routine flaring, lifecycle emissions disclosure, and procurement disqualification for non-compliance.

Within the gas pathway, the instrument design distinguishes bridge from baseload. Open-cycle gas turbines deploy in one to two years for peaking: short-duration power covering demand spikes and supply gaps. Combined-cycle gas turbines commission in two to three years for industrial baseload: continuous power serving loads that run around the clock. The financing tenor, risk profile, and capacity payment structure differ between the two. The implementation pathway for label reform across these governance structures is a separate institutional undertaking that this series frames but does not blueprint. A longer-term structural response is an African Transition Taxonomy, designed by African institutions, that defines transition on African terms and establishes sovereign authority over what qualifies as transition investment. The constraints on domestic institutional capital are the subject of the 2026 Inflection series referenced in Section 4.

Counter-arguments.

The carbon budget. The carbon budget is finite. African gas at scale adds cumulative emissions. The sequencing argument has been used by every fossil fuel incumbent to delay transition. Africa contributes 3 to 4 per cent of cumulative global greenhouse gas emissions while holding 17 per cent of the world’s population. Per capita emissions in sub-Saharan Africa are approximately one-tenth of the OECD average. The equity argument is clear. The carbon budget is a physical constraint, indifferent to historical responsibility. The empirical case is made here because it is strong, not because Africa owes a justification.

The emission profile differs by function. Gas replacing continuous diesel self-generation in Nigeria reduces emissions: diesel emits approximately 0.8 kilograms of CO2 per kilowatt-hour, gas combined-cycle approximately 0.4, cutting intensity by half. Gas replacing coal or avoiding new coal in South Africa and some Tier 3 countries also reduces or avoids emissions. Gas serving new industrial demand where no prior generation exists adds emissions. The carbon arithmetic depends on which function the gas serves.

Industry projections place total African gas-fired capacity at 144 gigawatts by 2035 (GlobalData, 2026), implying roughly 50 gigawatts of new capacity over the next decade. At 60 per cent capacity factor, that build-out would produce roughly 100 million tonnes of CO2 annually. Methane leakage adds to this. At a global average upstream intensity of 1 per cent (IEA Global Methane Tracker 2025) and GWP100 of 28, the annual total rises to approximately 115 to 130 million tonnes of CO2 equivalent. Over a 30-year asset life, the cumulative addition would be approximately 3,500 to 4,000 million tonnes of CO2 equivalent. The Global Carbon Budget 2025 estimates the remaining 1.5 degree carbon budget at 50 per cent probability at approximately 170 GtCO2 from January 2026. Against that figure, the cumulative addition is closer to 2 per cent than 1 per cent (the direct CO2 component alone, excluding methane, would be approximately 1.8 per cent). Africa holds 17 per cent of the world’s population. Even at the upper bound of this scenario, the direct CO2 component would consume roughly one-ninth of the continent’s proportional share of the remaining budget. The equity case and the empirical case point in the same direction. Disciplined deployment is consistent with both. The conditions are institutional design requirements, not moral prescriptions. Both the annual and cumulative framings are presented here so the reader can assess both.

The methane risk is real and must be managed. In countries with functioning regulatory capacity (Mozambique liquefied natural gas (LNG), Tanzania, Senegal), modern infrastructure with satellite monitoring can achieve leakage rates at the lower end of the global range. In Nigeria, where this essay has documented sovereign payment default and infrastructure vandalism, the governance failure that prevents the payment chain from functioning also threatens methane monitoring and maintenance. The methane risk is country-specific, not continental.

The distinction from fossil incumbents is precise. A European oil major arguing for continued extraction is delaying an existing transition in an industrialised economy. An African government arguing for gas-to-power is building the industrial base that makes transition structurally possible. No industrialised economy built its industrial base on variable energy alone. Every one used dispatchable power first and decarbonised later.

Cost and fiscal space. This counter-argument is stronger than the carbon budget. African solar PV runs USD40 to USD80 per megawatt-hour at African WACC, cheaper than gas combined-cycle at USD100 to USD150. African governments choose variable because it costs less. The binding constraint, the argument runs, is fiscal space rather than the label.

The cost claim requires decomposition. Levelised cost of energy (LCOE) folds capital costs, operating costs, fuel costs, and the cost of capital into a single number per megawatt-hour. The cost of capital, expressed as the weighted average cost of capital (WACC), is the critical variable. When Parts 2 and 3 established African solar at USD40 to USD80 versus a global range of USD34 to USD43, the primary difference was the WACC. Same panels. Same irradiation. Different cost of capital. The African WACC already prices in country risk, currency depreciation, political and regulatory risk, off-taker credit risk, and liquidity premiums. The same risks are embedded in gas combined-cycle LCOE. Currency risk, sovereign risk, and governance risk are not separate problems sitting outside the comparison. They are inside it.

What LCOE does not capture is system value: the economic worth of dispatchability and availability. This is Part 1’s taxonomy. A megawatt-hour from solar and a megawatt-hour from gas are not the same product. A government powering a copper smelter at 1,100 degrees around the clock does not choose between solar and gas. It needs both. Solar alone leaves the smelter without power at night. Grid-balancing storage at four to eight hours is scaling across Africa, including Eskom’s procurement programme and mining-sector deployments. Multi-day storage for continuous industrial loads at smelter or fertiliser scale through weather events does not yet provide a bankable substitute in African financing conditions. Within Firm Power Finance, gas is cheaper than diesel, cheaper than multi-day storage where it exists, and cheaper than lost industrial output. Private industry already absorbs firm power costs through diesel expenditure and production losses.

The question is why concessional capital does not flow to gas if the economics within firm power are clear. African sovereign risk premiums mean commercial lending rates are three to five times higher than in OECD markets. A solar project in Nigeria costs three times more to finance than an identical one in Madrid (IEA, 2025). The DFI anchor that de-risks the transaction for commercial lenders reduced the financing cost of African solar deployment. Solar capex fell from approximately USD4,000 per kilowatt in 2010 to USD600 today, driven primarily by Chinese manufacturing scale and industrial policy. The green taxonomy did not lower panel prices. But DFI concessional terms, standardised procurement, and green bond eligibility reduced the cost of deploying them. Gas combined-cycle capex runs USD800 to USD1,200 per kilowatt before pipeline and fuel supply, with ongoing fuel cost on top. Gas has not received the same financing treatment. The financing cost gap has multiple sources. Inherent differences in project risk: fuel supply exposure, construction complexity, and longer tenors. Sovereign risk premiums that bite harder on longer commitments. And the architecture that provides concessional terms for one and withholds them from the other. The architecture did not create the entire gap. It widened it. The relative weight of taxonomy exclusion versus inherent project risk is an empirical question this essay frames but does not resolve. A finance minister choosing the lower-capex option when it does not deliver the function her economy requires is responding rationally to a skewed architecture.

Three structural solutions work together because no single one is sufficient. The DFI anchor reduces the effective WACC for gas, but gas LCOE is split between capital cost and ongoing fuel cost, making it less WACC-sensitive than solar. The DFI anchor narrows the financing gap. It does not close it. The incremental currency exposure is the ongoing fuel cost. Dollar-indexed fuel cost pass-through clauses in PPAs, standard in gas structures in Turkey, Bangladesh, and Pakistan, manage the investor’s exposure but transfer it to the utility. If the local currency depreciates, the utility’s fuel payment rises, increasing off-taker default risk.

The primary structural solution is cost-reflective tariff pricing embedded in the PPA contract. Where tariffs adjust to reflect actual generation costs, the utility’s revenue tracks its fuel obligations and the currency mismatch closes at the consumer level. Kenya applies this to electricity through Energy and Petroleum Regulatory Authority (EPRA) approved tariff adjustments. A fuel cost charge per kilowatt-hour reimburses thermal generators for fuel expenditure, and a foreign exchange fluctuation adjustment per kilowatt-hour passes currency movements directly to consumer electricity bills. Other regulators operate tariff adjustment frameworks at various stages of implementation: South Africa’s National Energy Regulator (NERSA) sets multi-year tariff trajectories and Ghana’s Public Utilities Regulatory Commission (PURC) applies quarterly fuel cost adjustments. Neither has yet achieved full cost-reflectivity across the value chain. The International Monetary Fund (IMF) has advocated cost-reflective pricing across African electricity markets for years. The reforms are politically sensitive in every jurisdiction. But the alternative is the Nigerian pattern: suppressed tariffs, sovereign subsidy default, and a payment chain that makes every investment unbankable. Something must give. Countries that do not implement cost-reflective pricing cannot access firm power finance through the reformed architecture because the PPA is unbankable against an off-taker whose revenue does not cover its obligations. The condition is structural, not punitive. Cost-reflective pricing reduces the WACC independently, on top of whatever the DFI anchor provides, because a creditworthy utility is a lower-risk off-taker. The currency problem in gas has two components. Tariff governance determines whether the utility collects enough local currency revenue. Hard currency access determines whether that revenue can settle dollar-indexed fuel contracts. Cost-reflective tariffs address the first.

For the second, The Acid Test (April 2026) asked why Dangote has not moved to settle intra-African fuel trade through PAPSS, given that both refining capacity and settlement infrastructure now exist at scale. The same question applies to gas: where cross-border pipeline infrastructure exists, there is no reason intra-African gas trade should settle in dollars. The Pan-African Payment and Settlement System (PAPSS), operated by Afreximbank, settles cross-border transactions in local currencies. A Zambian power plant importing Mozambican gas through PAPSS pays in kwacha, settled to meticais, with no dollar exposure on the fuel transaction. This mechanism does not help countries importing LNG from non-African sources, where dollar pricing remains. But for the cross-border pipelines the Tier 3 pathway requires, PAPSS removes the dollar exposure from the utility’s fuel payment. The net trade balance between the two countries still requires settlement, and PAPSS currently operates across 19 countries with over 160 commercial banks connected. The system is scaling but has not yet been tested at the volumes large energy trade requires. For intra-African trade, the currency risk should no longer sit in the cross-border fuel contract where it originates. If the gas supply agreement settles in local currencies through PAPSS, the dollar exposure that would otherwise flow through to the PPA disappears at source. The same principle extends to refined petroleum, LPG, and any intra-African fuel transaction where both buyer and seller operate within the PAPSS network.

The fiscal space claim does not survive contact with the evidence at the supply level. Variable energy is scaling at unprecedented pace across the continent. CEC issued a green bond. Nigeria issued a sovereign green bond. The REIPPPP deployed over 6,000 megawatts. On 26 May 2026, Kenya’s National Treasury announced a target of KSh100 billion (USD772 million) in green bonds by the end of 2027 for solar-powered cold chains, regenerative farming, and climate adaptation. Solar-powered cold chains with battery storage are the right instrument for agricultural access: they work with variable energy at moderate scale. The bond is correctly designed for its stated purpose. The point is what sits beside it. The same government is mobilising three-quarters of a billion dollars through a green instrument for agriculture. No comparable instrument exists for the firm power its industrial sector requires. The fiscal space is there. The label determines where it goes. This is an observation about allocation, not a claim about capacity.

The institutional consensus supports expanded risk appetite. The G20 Independent Expert Group’s 2023 report called for multilateral development banks (MDBs) to shift from risk avoidance to informed risk-taking, endorsed by G20 leaders in the New Delhi Declaration. The subsequent Capital Adequacy Framework review found that MDBs have overestimated their financial risks and underestimated their lending capacity by hundreds of billions of dollars. The question this essay poses is narrower: whether that expanded appetite should include firm power or whether the label architecture confines it to variable energy and access.

For nuclear, bilateral vendor finance dominates. Rosatom finances Egypt’s El Dabaa at approximately 3 per cent over 22 years with tied Russian procurement. Korea Electric Power Corporation (KEPCO) built the United Arab Emirates (UAE) Barakah project. These are evidence that the multilateral architecture chooses not to fund nuclear, and bilateral providers fill the space. The Forced Choice does not mean every sovereign reluctantly accepts bilateral finance. Some prefer it. The point is narrower: when multilateral channels exclude firm power by design, bilateral channels become the only available option rather than one among several.

The coal retirement gap. The sharpest evidence against the current architecture is not what it fails to fund. It is what it actively removes without replacement.

South Africa operates approximately 39 gigawatts of coal. Eskom plans reduction to 18 gigawatts by 2040, with 8.4 gigawatts scheduled for retirement by 2029 to 2030. The JETP was designed to fund coal retirement and a just transition. Its design did not include gas financing. The critique is not that the JETP failed to do what it never promised. It is that the architecture which excludes gas from JETP-style vehicles leaves a Firm Power Finance gap the JETP does not address. Total commitments sit around USD12 to USD14 billion depending on whether MDB and wider bilateral pledges are included. The original USD8.5 billion pledged at COP26 was restructured, with the EU contributing a USD5.1 billion package in May 2025 and Germany raising its commitment to EUR2.68 billion, of which EUR1.4 billion has been disbursed. Capital is arriving for coal retirement. It is not arriving for firm power replacement. The Gas Independent Power Producer Procurement Programme (GASIPPPP) launched in December 2023. It has been extended twice: the original August 2024 deadline moved to October 2025, then to May 2026. The delays were driven by fuel supply dependency on an unbuilt LNG terminal at Richards Bay, project-on-project risk, and repeated scope and load factor changes during the bid window. Under the amended timetable, bid submission is scheduled for 29 May 2026, with preferred bidders following approximately three months later. Commercial close follows approximately twelve months after preferred bidder announcement, and financial close carries a three-month long stop after commercial close. Commissioning follows two to three years after financial close, placing the earliest operational date beyond 2030. The programme’s track record of repeated extensions makes further delays likely. Against 8,400 megawatts of coal retirement by 2029 to 2030, the timeline cannot close the replacement gap. No nuclear procurement programme exists despite the Integrated Resource Plan (IRP) 2025 allocating 5,200 megawatts.

Eskom delayed decommissioning of the Camden, Grootvlei, Hendrina, Arnot, and Kriel coal plants from 2027 to 2030 because replacement capacity does not exist. A JETP designed with a Firm Power Finance lane would have funded replacement alongside retirement. The current design funds retirement alone. The architecture operates on firm power in two ways. For gas, it excludes capital from flowing to new firm power that does not yet exist. For coal retirement, it funds the removal of firm power that already exists without funding what replaces it. The second is sharper: it actively widens the firm power gap rather than merely leaving it unfilled.

The US contrast is dispositive. In 2025, the US government simultaneously withdrew from the JETP and expanded the US International Development Finance Corporation (DFC) scope to include oil and gas infrastructure in Africa. At home, the Inflation Reduction Act funds both variable energy and firm power. Abroad, the multilateral architecture restricts firm power while the bilateral channel expands into it. The DFC, Chinese development finance, Gulf sovereign investment, and Indian bilateral lending compete for the space. The DFC’s expansion demonstrates that a development finance institution can include firm power when its principals choose to. That one institutional change produced the only unqualified “Yes” in the Firm Power column. But one bilateral channel expanding does not solve the structural problem.

Every bilateral channel carries conditions set by its principals. The DFC ties to US strategic positioning and private sector involvement. Chinese development finance has built firm power across the continent, from general grid infrastructure to power serving Chinese-operated extraction and processing. Gulf sovereign investment and Indian bilateral lending carry their own commercial terms. Each provider sets terms without competitive pressure from alternatives. A reformed multilateral architecture offering firm power on concessional terms with untied procurement would give African governments both sovereign control over what that energy powers and competitive alternatives where currently none exist. The Forced Choice is not only about who finances. It is about what the financing is designed to produce. Firm power that enables mineral processing and manufacturing for absorber markets builds the purchasing power that makes eventual intra-African trade viable. Firm power that serves only extraction keeps the continent at the intermediate stage. Whether the multilateral restriction of firm power and the simultaneous bilateral expansion into it reflect institutional inertia or structural incentive is a question Part 5 addresses.

Programmatic procurement. Three DFI gas projects in a decade is not a programme. The mechanism through which firm power capital deploys at project level is the banking syndicate. A DFI provides anchor investment or a guarantee. Commercial banks participate in syndicated senior debt at rates the anchor makes viable. This is how Azura-Edo was financed and how every REIPPPP project deployed. Label reform permits the anchor. The anchor unlocks the syndicate. The syndicate deploys the capital.

What Firm Power Finance requires is the equivalent of the REIPPPP for gas, geothermal, medium hydro, and pumped hydro. Competitive procurement, standardised PPAs, transparent auctions, and a project pipeline institutional capital can assess at portfolio scale. The AfDB’s seventeenth African Development Fund replenishment (ADF-17, USD11 billion, December 2025) and Africa Finance Corporation have the institutional architecture to host such a programme. Calibrating it to each country’s resource endowment closes the gap between transaction-specific exceptions and continental deployment. The REIPPPP mobilised over USD16 billion in private investment for variable energy in a single country. A comparable programmatic framework for firm power, even at a fraction of that scale, would represent a material change in capital availability for African industrialisation.

Capacity payments. China established a benchmark fixed cost of CNY330 per kilowatt per year for coal plants, with eligible plants compensated for a rising share of that cost, reaching 50 per cent from 2026. The mechanism covers both existing fleet and new build, separating the availability function from the generation function. China’s benchmark compensates coal plants for remaining available as renewables dispatch first. Africa’s challenge is different. The capacity payment must be high enough and certain enough to attract new investment at African WACC, where the cost of capital is three to five times higher. The plant has not yet been built. China can enforce capacity payments within a state-owned, centrally planned system. Most African electricity markets remain vertically integrated and state-owned. Nigeria and South Africa are partially unbundled and privatised, with payment chain failures the Nigeria section documents. Transplanting the mechanism requires the payment chain to function first.

For new firm power investment, the PPA must include a capacity payment from the start. For existing firm power plants, the same mechanism ensures continued availability as the generation mix evolves. Cost-reflective tariffs and PAPSS address the utility’s revenue and the fuel contract’s currency exposure. The capacity payment addresses a different risk: fixed cost recovery over the PPA life. In most African markets today, the immediate constraint is not enough generation of any kind. Variable energy and firm power complement each other rather than compete: solar provides daytime energy, firm power provides the rest. For dedicated industrial off-take serving continuous loads, the plant runs around the clock regardless of solar availability. The PPA must guarantee minimum revenue through take-or-pay obligations covering fixed costs, the mechanism Part 1 specified. Where cost-reflective tariffs and PAPSS are in place, the required capacity payment is lower because the off-taker and currency risks are already managed. But it is not zero. Without guaranteed fixed cost recovery, the investment does not close.

Payment security beneath the capacity payment requires escrow structures, partial risk guarantees, tariff adjustment formulas, and subsidy payment covenants. Models exist: ring-fenced escrow accounts in Pakistan and Bangladesh power sectors have enabled gas IPP financial close despite weak utility balance sheets. Though Pakistan’s subsequent circular debt crisis illustrates why the utility gate this essay prescribes alongside the mechanism is essential. The capacity payment is necessary but not sufficient without the utility restructuring Section 3 addresses.

2. Where Capital Must Land

Part 3 mapped Africa’s firm power options across two lanes: the Growth Lane (firm power with speed) and the Resilience Lane (firm power with time). This essay focuses on the Growth Lane because the industrialisation constraint is immediate. Resilience Lane technologies (small modular reactors, large nuclear, large hydro at Grand Inga scale) operate on seven to fifteen year timelines. They matter for the long term. They do not solve the Chambishi production cut or the 22 million Nigerian generators this decade. The three tiers below translate the Growth Lane into country-specific financing prescriptions. The tiers reflect resource endowment, not hierarchy. As Part 3 established, gas combined-cycle is the most broadly deployable Growth Lane technology because it combines speed, dispatchability, and resource availability across more African jurisdictions than any alternative. Where the geology permits, geothermal is cheaper and carries zero operational emissions. The ordering is contextual: geothermal where the geology permits, medium hydro and pumped hydro where the hydrology permits, gas where those are unavailable or insufficient, coal only as last resort where no alternative exists. The technologies are not always sequential. A country with both gas reserves and geothermal potential may deploy gas open-cycle gas turbines (OCGT) in one to two years while developing geothermal over three to five. Kenya’s own system operates gas peaking alongside geothermal baseload. The tiers are a spectrum, not fixed categories. Zambia lacks domestic gas but is building domestic firm power across multiple technologies. Ngonye Falls (180 megawatts) and Lunsemfwa Lower (255 megawatts) are medium hydro projects in development. Cross-border pipelines from Mozambique and Namibia would feed a gas-to-power plant on the Copperbelt, serving the copper mining industry directly. The plant is Zambian. The fuel is imported. Tier 3 economies build domestic firm power where their resource endowment permits and import fuel through cross-border infrastructure where it does not.

For Tier 1 countries with domestic gas (Nigeria, Mozambique, Senegal, Tanzania, Algeria, Egypt, and at least nine others): label reform unlocks the binding constraint on Firm Power Finance. The condition is that energy sector governance is functional enough to absorb the capital. Gas combined-cycle at USD100 to USD150 per megawatt-hour replaces diesel self-generation and provides industrial baseload. Nigeria is the largest and most prominent exception: label reform is necessary but governance reform must come first.

For Tier 2 countries with geothermal or hydro resources: climate finance is available but the binding constraint is upstream.

Kenya has deployed over 1,000 megawatts of geothermal at Olkaria and Menengai, where KenGen and the Geothermal Development Company operate the largest geothermal complex in Africa. Ethiopia has operational capacity at Aluto Langano and is developing further sites along the Rift. At USD50 to USD80 per megawatt-hour in the East African Rift, geothermal is the cheapest firm power source where the geology permits, outperforming gas on cost and reliability at capacity factors exceeding 90 per cent. This is firm power: 24/7, weather-independent, zero operational emissions. The East African Rift holds an estimated 15,000 megawatts of geothermal potential across Kenya, Ethiopia, Djibouti, Tanzania, Uganda, and Rwanda. Deployment stands at approximately 1,000 megawatts against 15,000 megawatts of potential: 7 per cent, after decades of development. The constraint is exploration risk. Drilling a geothermal well costs USD5 to USD7 million with failure rates of 20 to 40 per cent. No commercial bank absorbs that risk. The Geothermal Risk Mitigation Facility for East Africa disbursed approximately USD115 million across its lifetime, a fraction of what exploration at 15,000 megawatt scale requires. Once a resource is confirmed, the project becomes bankable and conventional DFI and commercial finance can close the deal. The bottleneck is upstream, not downstream. The corrective for geothermal is not label reform. It is scaled-up concessional first-loss exploration facilities at an order of magnitude beyond current provision.

Africa’s installed hydro capacity stands at approximately 40 gigawatts against an estimated exploitable potential of 350 gigawatts. Approximately 10 per cent developed. Major facilities operate across the continent: Cahora Bassa in Mozambique (2,075 megawatts), the Grand Ethiopian Renaissance Dam (GERD) in Ethiopia (5.15 gigawatts, operational), Kariba shared between Zambia and Zimbabwe (1,626 megawatts). Medium hydro at 50 to 300 megawatts, where hundreds of identified sites exist across West, Central, and East Africa, rarely reaches feasibility study stage. A medium hydro project requires three to seven years from pre-feasibility through environmental and social assessment to bankable design, at a cost of USD2 to USD10 million per stage before construction financing is mobilised. Africa50 and the AfDB’s New Partnership for Africa’s Development (NEPAD) Infrastructure Project Preparation Facility were designed for this gap. Both are underfunded relative to the scale. Hydro is also climate-vulnerable: the Chambishi story is a hydro story. Drought reduced Kariba and Kafue Gorge output, causing the production cut the opening describes. The preference ordering places geothermal above hydro for this reason: geothermal is weather-independent. But both are zero-emission firm power, both are label-eligible, and both are constrained by risk capital and project preparation, not by the taxonomy.

For Tier 3 countries without domestic gas, geothermal, or viable hydro: four parallel pathways operate. Cross-border Grid Finance imports electricity from neighbours. Cross-border fuel import brings pipeline gas to a domestic power plant, keeping the generation asset and its industrial value chain inside the country. Both require sovereign borrowing, DFI concessional loans, and PPP concessions with availability payments. Cross-border infrastructure introduces multi-sovereign risk that requires regional guarantee instruments, potentially backed by the Southern African Development Community (SADC), the Economic Community of West African States (ECOWAS), or the AfDB’s concessional windows. Where domestic coal reserves exist and no lower-emission alternative is accessible, coal provides firm power as a last resort within the Growth Lane. Over the longer term, small modular reactors, large nuclear, and large hydro operate through the Resilience Lane at seven to fifteen year timelines. The four pathways are not sequential. A Tier 3 country may pursue a cross-border pipeline, develop domestic coal, and plan for nuclear simultaneously.

Within the preference ordering, trade exposure reinforces the emission logic. Gas avoids coal’s Carbon Border Adjustment Mechanism (CBAM) exposure. If the architecture had financed gas through cross-border pipelines at concessional terms, some coal capacity plans might not be necessary.

3. Who Carries the Architecture

Capital does not land in a vacuum. It lands in an institutional environment. Two conditions must hold: the utility that off-takes must be creditworthy, and the institutional architecture that deploys must be African.

On utilities: the pattern across the continent is consistent. Reform happened. Investment arrived for variable energy where the off-taker risk was manageable. Firm power investment carries higher annual obligations, longer tenors, and fuel cost pass-through. Distressed utilities cannot guarantee these.

Nigeria’s unbundled sector reveals the deepest structural failure, and the conventional narrative misplaces the blame. Under the DisCo Remittance Obligation framework introduced in January 2024, DISCOs paid 93 per cent of their reduced remittance obligation in Q4 2025 (author analysis of Nigerian Electricity Regulatory Commission (NERC) quarterly reporting). The DRO represents the share of the generation invoice that allowed tariffs can cover. The Federal Government is responsible for the remainder as subsidy. In 2025, that subsidy obligation totalled N1.93 trillion. The government paid N76.95 billion. Less than 4 per cent. By December 2025, the sector’s total accumulated debt had crossed N6 trillion. The Federal Government launched a N4 trillion Power Sector Debt Reduction Programme in August 2025 to securitise legacy GenCo and gas supplier arrears accumulated since 2015. The first tranche of N501 billion was fully subscribed in December 2025. The programme addresses the accumulated stock. The annual subsidy shortfall that created it continues. Aggregate technical, commercial, and collection (ATC&C) losses averaged 34.9 per cent in Q4 2025, with Kaduna DISCO recording 69.45 per cent. Suppressed tariffs combined with sovereign subsidy defaults create the primary liquidity drain. Where tariffs do not cover costs, the utility accumulates debt that eventually migrates onto the sovereign balance sheet. Zambia’s ZESCO illustrates the pattern: utility losses become fiscal liabilities that constrain the sovereign’s capacity to invest in the very infrastructure that would resolve the energy gap. Concessional capital arriving in a payment chain where the sovereign does not pay its own bills produces the same outcome as bilateral capital in the same chain. The sequencing is country-specific. For Nigeria, payment chain reform comes first, potentially through ring-fenced escrow structures and subsidy pre-funding covenants tied to DFI tranching. For Senegal, Tanzania, Mozambique, and selected mining corridors, the governance constraint is different and label reform can operate earlier.

The South Africa comparison makes the architecture argument’s independence from governance visible. The same sovereign, the same institutions, the same regulatory environment produced over 6,000 megawatts of variable energy through the REIPPPP and zero megawatts of gas through the GASIPPPP. Eskom received R254 billion in debt relief, recorded over 365 consecutive days without load-shedding by May 2026, and reported a pre-tax profit of R23.9 billion for FY2025. An 8.76 per cent tariff increase was approved by the National Energy Regulator of South Africa (NERSA) for FY2026/27. The recovery relied on coal fleet maintenance and over 5,000 megawatts of private renewable energy, predominantly solar. It did not produce a single megawatt of new gas or nuclear. No commercial gas-to-power PPA has been signed against Eskom offtake. Municipal debt exceeding R105 billion as of late 2025 and growing keeps the payment chain broken at distribution. The variable energy PPA closed. The gas PPA did not. The governance environment is identical. The taxonomy eligibility is not. Gas also carries fuel supply and construction risks that solar does not. But the REIPPPP provided an architecture designed for variable energy. No equivalent exists for gas.

The architecture’s reach extends beyond the instrument label. It operates through at least three channels. Taxonomy labels restrict what instruments can fund. DFI board policies restrict what institutions will finance. And advocacy informed by the same intellectual framework shapes domestic regulatory outcomes. In South Africa, the Risk Mitigation Independent Power Producer Procurement Programme (RMIPPPP) selected Karpowership as a preferred gas bidder. Environmental litigation, drawing on arguments consistent with the international position against new fossil fuel development, prevented the project from reaching financial close. Legitimate environmental regulation and categorical opposition to gas as a fuel are different phenomena and should be distinguished. But the pattern is observable across multiple African jurisdictions. The climate finance architecture does not only restrict capital allocation. It shapes the regulatory environment in which capital must operate. Part 5 examines whose interests this architecture serves.

Kenya Power improved to profitability in FY2025 (KSh24.47 billion after tax) but carries 73 per cent gearing, a KSh19 billion working capital deficit, and system losses at 21 per cent. Customer outages averaged 8.39 hours per month. Hyperscale data centre expansion has been constrained by the absence of bankable firm power guarantees.

Tanzania holds 57 trillion cubic feet of gas, managed upstream by the Tanzania Petroleum Development Corporation (TPDC). The country’s USD42 billion LNG project targets a Host Government Agreement by mid-2026. Without utility reform at TANESCO, the gas remains offshore.

Senegal’s firm power gap takes a different form. SENELEC manages a grid where 25 per cent of national supply comes from floating power vessels at emergency cost. Karpowership is utility-scale imported fuel dependence, not household diesel self-generation. Greater Tortue Ahmeyim (GTA) Phase 1 is producing and exporting LNG while SENELEC lacks the infrastructure to convert domestic gas to domestic power. Political uncertainty following the Sonko dismissal in May 2026 compounds the challenge.

Mozambique presents a third pattern. The country holds over 100 trillion cubic feet of gas in the Rovuma Basin. Generation resources exist. The binding constraint is transmission: gas and hydro do not connect to industrial demand at scale. The constraint here is Grid Finance, not Firm Power Finance at the generation level.

Utility restructuring is not a recommendation. It is the gate. Countries seeking firm power finance through the reformed architecture must demonstrate cost-reflective tariff pricing, payment chain discipline, and off-taker creditworthiness. Without these, concessional capital cannot close a firm power PPA regardless of label status. Debt relief, structural separation, tariff enforcement, and payment chain discipline must precede firm power investment, not follow it.

On institutional architecture: the named African institutions carry the deployment. AFC provides project development and equity for Firm Power Finance, including the capacity to structure guarantee pools backstopping firm power PPAs directly against industrial offtakers where utility creditworthiness is insufficient. Afreximbank provides trade finance and intra-African credit guarantees at trade-cycle tenors, and operates PAPSS for local currency settlement of cross-border energy trade. Multi-decade fuel supply guarantees require partial risk guarantees from sovereign-backed multilaterals such as the AfDB. The Trade and Development Bank (TDB) offers project finance at tenors longer than commercial banks but shorter than firm power asset lives, a gap that concessional co-financing must bridge. The AfDB provides concessional windows and sovereign guarantees. Africa50 provides project preparation for the bankability gap. The New Development Bank lends without the macro-policy conditionality associated with Bretton Woods institutions, though it maintains standard fiduciary and project-level requirements. These are the architecture through which a reformed label system would deploy. Their transaction-level capacity is demonstrated. Programmatic deployment at the scale the REIPPPP achieved requires capital replenishment and mandate expansion that ADF-17 and AFC’s capital raise have begun but not completed.

4. The Foundation Layer

This series diagnoses the energy architecture. It is one layer of an integrated Canary Compass programme.

The 2026 Inflection series builds the productive sector architecture. Part I (January 2026) established the structural forces: AI compressing labour returns, diaspora reconnection with the continent, and Africa’s absorption gap. Part II (April 2026) built the fiscal filter: a two-gate system applying a locked metric across all 55 AU members, with a tier structure determining which countries have earned the discipline for capital deployment. It also specified a four-level measurement engine addressing the audit lag that makes public reporting too uneven for live allocation. Part III, which builds the three capital pools for deployment into absorption industries, has not been published because the energy foundation must be established first. A Pool One credit allocation to a copper smelter without firm power behind it funds a factory that cannot run. The reverse also holds: firm power without the industrial demand to absorb it creates stranded generation assets. The two are co-dependent. The Chambishi production cut is Pool One failing before it begins. African pension assets exceed USD450 billion and insurance assets exceed USD320 billion. Regulation in South Africa, Nigeria, and Kenya already permits infrastructure allocation. The mechanism for channelling this capital is the Codex architecture that Part III specifies.

The Forced Choice (February 2026) established that the terms on which African minerals reach global markets are set by geopolitical competition between absorber and surplus nations. The Cathode Economy, publishing after this series completes, will show that every route through the extractive value chain ends in truncation. The energy constraint is structural across the entire extractive lane, not specific to any single mineral. Who captures the mineral processing value depends on who has the firm power to process. The Forced Choice identified a five to seven year window before battery chemistry substitution erodes Africa’s mineral bargaining power. Waiting for clean firm alternatives to reach bankability at African WACC risks arriving at the post-leverage world with nothing built. Without the energy corrective this essay specifies, the Codex pools deploy into industries that cannot run and the mineral value chain remains truncated at the intermediate stage.

Energy is the foundation layer. Capital deployment is the structure. Mineral value capture is the prize. The three series are the same architecture at different layers.

5. Close

Mariana Mazzucato’s mission-oriented framework argues that public finance should shape markets, not merely fix market failures. The architecture should define the mission first and design the instruments to serve it. The current architecture defines the instrument first and lets the mission follow. The Misaligned Transition corrective reverses the sequence. The mission is not “deploy renewable energy.” The mission is “build the firm power base that makes industrialisation and eventual transition structurally possible.” A mission-oriented critic might argue the mission should be clean firm power only: nuclear, geothermal, green hydrogen. The series’ preference ordering is consistent with that ambition. Geothermal and hydro where the geology and hydrology permit. Gas as time-bound bridge where they do not. Coal as last resort. The bridge exists because the clean alternatives are not yet deployable at the scale and speed African industrialisation requires across enough jurisdictions.

The pathway has precedent. Bangladesh’s garment sector, which generates over 80 per cent of the country’s export earnings and employs approximately 4 million workers, scaled on firm power from both the national grid and captive gas generators inside factories. Gas accounts for over half of Bangladesh’s electricity generation, and factory-level captive plants added 1,700 megawatts of gas-fired capacity. When gas supply fell in 2022, both channels collapsed: garment factories shut down production for half the working day. The pattern mirrors Nigeria’s 22 million generators. When grids cannot deliver, industry builds its own firm power. When the fuel behind that power becomes unavailable, the industrial base cracks. Africa’s absorption industries, from copper smelting to fertiliser to cement, require the same foundation.

Songwe, Stern, and Bhattacharya called for USD2.4 trillion in annual climate investment for emerging and developing economies by 2030. The series agrees on scale. It disagrees on structure. The corrective is not more money through the same labels. It is differently structured money through reformed labels. The governing principle from Part 1 holds: the category follows the function, not the fuel. Capital that funds dispatchable industrial power is Firm Power Finance whether the source is gas, geothermal, nuclear, or hydro.

Expanding the range of channels available for firm power increases African negotiating power. A reformed multilateral architecture competing alongside bilateral providers gives African governments more options, not fewer. Until that reform arrives, the Forced Choice operates.

Africa’s transition does not begin with the displacement of firm power. It begins with the financing of it.

Part 5 tests the taxonomy against three instruments that channel capital into Africa under green labels: carbon credits, hydrogen export corridors, and external land acquisitions. It asks whose industrial future the current architecture is designed to serve.

Sources

African Development Bank, ADF-17 Replenishment (Abidjan, December 2025).

African Union, Common Position on Energy Access and Just Transition (Addis Ababa, various 2022-2024).

Copperbelt Energy Corporation, Green Bond Programme and Itimpi II Commissioning (Kitwe, December 2024 and April 2026).

Energy Capital Power, “DFC Eyes African Oil & Gas Infrastructure Opportunities” (Houston, August 2025).

Energy for Growth Hub, “How South Africa Ended Load Shedding Without New Infrastructure” (April 2026).

Eskom Holdings, Generation Recovery Plan Update, FY2025 Financial Results, Parliamentary Briefings, and NERSA MYPD6 Tariff Determination (Johannesburg, 2025-2026). Author analysis of publicly reported Eskom operational and financial data.

Federal Republic of Nigeria, Series III Sovereign Green Bond Prospectus (Abuja, 2025).

Global Carbon Project, Global Carbon Budget 2025, ESSD (May 2026).

G20 Independent Expert Group, The Triple Agenda: A Roadmap for Better, Bolder, and Bigger MDBs (October 2023); and G20 Independent Review of MDBs’ Capital Adequacy Frameworks (July 2022).

IEA, Global Methane Tracker 2025 (Paris, 2025).

IEA, World Energy Investment 2025 (Paris, June 2025).

IFC and SIMA, USD150 Million Solar Green Bond for African Solar Developers (Washington, February 2024).

IRENA, Renewable Power Generation Costs in 2024 (Abu Dhabi, September 2025).

IRENA, Geothermal Energy Development in Eastern Africa: Recommendations for Power and Direct Use (Abu Dhabi, November 2020).

GlobalData, Africa Power Market Outlook to 2035 (London, March 2026).

Kenya National Treasury and Agriculture Ministry, National Agriculture Sector Investment Plan: Green Bond Programme (Nairobi, May 2026).

Loss and Damage Collaboration, Board Meeting B8 Update (Livingstone, April 2026).

Mordor Intelligence, Africa Diesel Generator Market (January 2026).

NERC, Commercial Performance of DisCos Fact Sheets and Quarterly Reports (Abuja, various 2024-2026). Author analysis of NERC quarterly reporting for DRO remittance, government subsidy obligations, and ATC&C loss data.

Onyambu, Dean N., “The Forced Choice,” Canary Compass (February 2026).

Onyambu, Dean N., “Africa Macro Note: The Acid Test,” Canary Compass (April 2026).

Onyambu, Dean N., “The 2026 Inflection: Part I, Push, Pull, Friction,” Canary Compass (January 2026).

Onyambu, Dean N., “The 2026 Inflection: Part II, Pricing, Measurement, Capital,” Canary Compass (April 2026).

Presidential Climate Commission (South Africa), JETP Implementation Reports and JETP Investment Plan (Pretoria, various 2023-2025).

Songwe, Stern, and Bhattacharya, Finance for Climate Action: Scaling Up Investment for Climate and Development (London, November 2022).

Transnational Institute, “Dependency by Design: How the JET-IP Structures South Africa’s Energy Future” (November 2025).

UK Government, “12-Month Just Energy Transition Partnership Leaders’ Update 2025” (London, December 2025).

World Bank, “Access to Energy” and Nigeria Generator Market Estimates (Washington, various 2022-2024).

Disclaimer

This article does not constitute legal, financial, or investment advice. The author shares views for perspective and discussion only. Do not rely on them as a substitute for professional advice tailored to your specific circumstances. Always consult a qualified legal, financial, investment, or other professional adviser before making decisions based on this content. The analysis reflects proprietary research undertaken by Canary Compass and the author.

Canary Compass and the author accept no liability for actions taken or not taken based on the information in this article.

The views expressed in this article represent the author’s independent professional analysis and do not constitute an endorsement of any individual, institution, or position. Canary Compass and the author accept no responsibility for how this content is interpreted, excerpted, or recontextualised by third parties not involved in its production and publication. Reproducing any portion of this work in isolation, or in combination with other material, in a manner that misrepresents the author’s original meaning constitutes a distortion of the published record.

The author may hold positions in financial instruments, currencies, or assets discussed or referenced in this publication. Such positions do not constitute a recommendation to buy or sell.

All views, projections, and forecasts reflect the author’s assessment at the time of writing. Data sourced from third parties is believed to be reliable but has not been independently verified. Past performance does not indicate future results.

All content published by Canary Compass is the intellectual property of the author. Reproduction, adaptation, or redistribution, in whole or in part, requires written permission.

About the Author

Dean N. Onyambu is the Founder and Chief Strategist of Canary Compass, a financial research publication focused on African monetary architecture and financial sovereignty. He brings 18 years of experience across trading, fund leadership, and economic policy, with senior roles at Standard Bank, First Capital Bank, and Opportunik Global Fund.

Read and subscribe at www.canarycompass.com.

The Canary Compass Channel is available on @CanaryCompassWhatsApp for economic and financial market updates on the go.

For more insights from Dean, you can follow him on LinkedIn @DeanNOnyambu or X @InfinitelyDean.