THE FORCED CHOICE

Absorber Economies, Surplus Economies, and the Closing Window: A Working Paper | 60–75-minute read

AI-generated image of the Forced Choice

Abstract

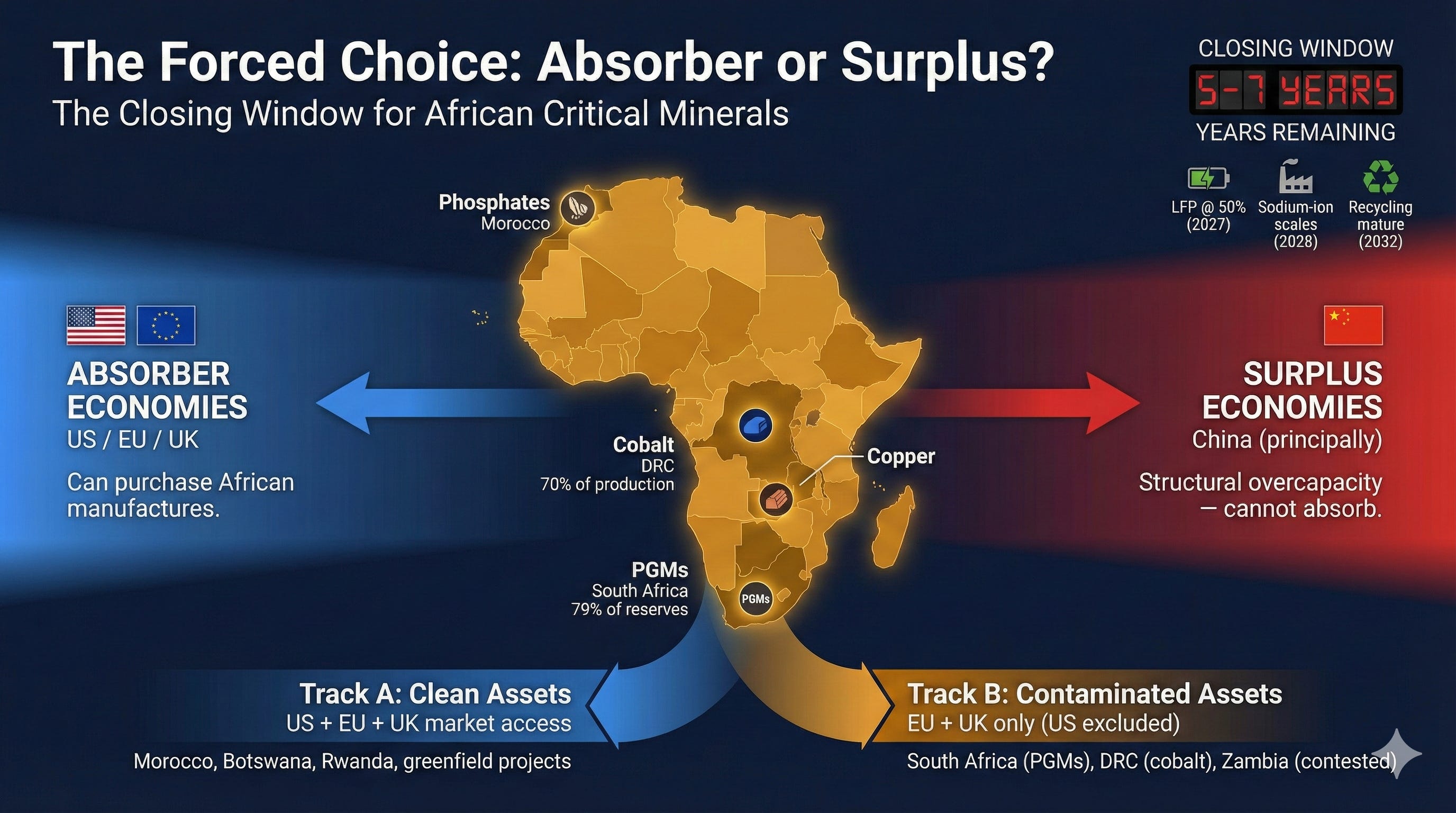

This working paper examines Africa’s strategic position in critical mineral supply chains amid intensifying US-China competition. Applying value chain analysis, Porter’s Five Forces, VRIO, and Ansoff Matrix frameworks, the analysis finds that African mineral leverage is narrower than commonly claimed but strategically significant where geological concentration exists; principally in platinum group metals (PGMs, Africa holds 79 per cent of global reserves, concentrated in South Africa) and cobalt (55 per cent of reserves, over 70 per cent of production). This leverage faces a closing window five to seven years before battery chemistry substitution erodes bargaining power.

The paper introduces a structural distinction between absorber economies (United States, European Union) that can purchase African manufactures and surplus economies (principally China) whose overcapacity prevents them from serving as markets for African industrial output. This distinction governs which partnerships can deliver industrial upgrading rather than permanent commodity extraction.

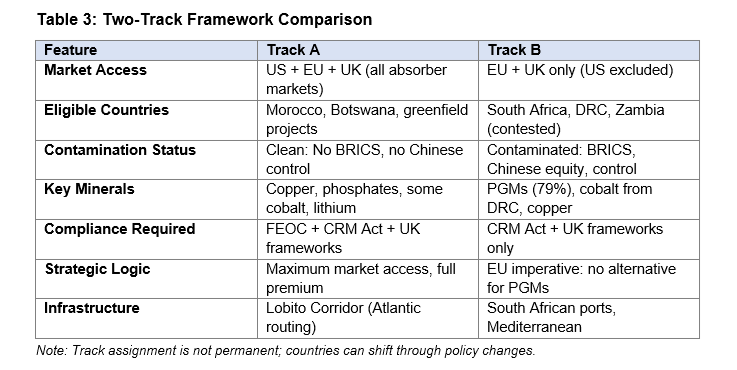

Five strategic pathways are assessed: strategic autonomy, full China alignment, full US alignment, the Carney middle-power model, and EU/UK diversification. Each faces fatal flaws. The paper proposes a ‘Coalition of the Eligible’ operating on two tracks: Track A for assets with clean access to all absorber markets, Track B for contaminated assets accessing EU/UK markets only, as the least bad pathway for converting geological leverage into industrial capacity before the window closes.

Keywords: critical minerals, Africa, industrial policy, supply chains, US-China competition, cobalt, platinum group metals

Executive Summary

This working paper addresses critical minerals as defined by the US Inflation Reduction Act and EU Critical Raw Materials Act: the minerals essential to battery manufacturing, renewable deployment, and grid expansion whose supply chains are subject to geopolitical contestation. These include cobalt, lithium, nickel, manganese, graphite, platinum group metals (PGMs), and increasingly copper. The analysis does not address bulk industrial minerals such as iron ore or bauxite except where they intersect with critical mineral supply chains.

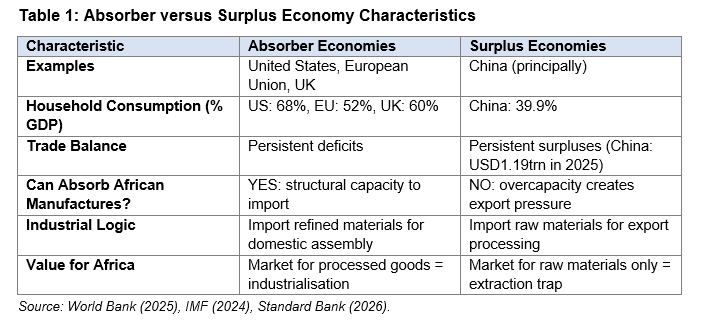

This paper distinguishes between two categories of major economy in the critical minerals supply chain. Absorber economies (the United States and European Union) consume processed minerals to manufacture finished goods. They import refined materials and components. Surplus economies (principally China) process raw materials into refined inputs and export the surplus. The absorber needs the mineral; the surplus economy controls the processing. Africa sits upstream of both, supplying raw material to whoever pays.

The commonly cited claim that Africa holds 30 per cent of global mineral reserves requires qualification. Bright Simons of IMANI and ODI has traced this figure to a 2002 African Development Bank paper with no subsequent verification. The actual data is more nuanced: Africa dominates in a handful of specific minerals but is a minor player in most others. Lithium reserves stand at 1.6 per cent of the global total. Rare earths at 2 to 3 per cent. These are marginal positions.

Yet Africa receives barely 10 per cent of global exploration spending, a share that has declined from 16 per cent in 2004. Sub-Saharan Africa is the most cost-effective region globally for mineral exploration. Australia and Canada, with combined landmass one-third Africa’s size, together receive three times the exploration investment. The gap between potential and capital flow is structural, not geological. The leverage that exists is narrower than commonly assumed but strategically significant where it does exist.

The Democratic Republic of Congo produces over 70 per cent of global cobalt. Africa holds 79 per cent of global platinum group metal reserves, concentrated in South Africa’s Bushveld Complex. These geological concentrations create genuine leverage. That leverage faces a closing window of five to seven years before substitutes mature and bargaining power erodes. Platinum group metals and cobalt represent genuine chokepoints. For these minerals, there is no alternative source at scale. The question is whether Africa can convert this narrow window of geological advantage into lasting industrial capacity before substitution renders it moot.

Four analytical frameworks converge on a single verdict. Value chain analysis shows Africa trapped at extraction while value accumulates elsewhere. Porter’s Five Forces confirms leverage exists but diminishes with time as substitutes advance. VRIO analysis identifies organisation as the missing criterion: Africa possesses valuable, rare, and difficult-to-imitate resources but lacks the continental coordination to capture value from them. The Ansoff Matrix directs strategy toward the only viable quadrant: diversification into new products (processed minerals) sold to new markets (absorber economies that can purchase them).

The structural distinction that governs outcomes is between absorber and surplus economies. Absorber economies run persistent trade deficits and consume more than they produce. They can purchase African manufactures. The United States is the paradigm, with household consumption at 68 per cent of GDP. Surplus economies produce more than they consume. China is the paradigm, with household consumption suppressed to 39.9 per cent of GDP and a goods trade surplus exceeding USD1.19 trillion in 2025.

China consumes domestically, including high-end goods. The issue is overcapacity. Chinese manufacturing capacity exceeds what domestic consumption absorbs, creating structural export pressure. Until China demonstrates sustained demand for external manufactures rather than commodities alone, it cannot serve as an absorber market for African industrialisation. Strategic autonomy has narrowed sharply. India faced tariffs of 50 per cent until 2 February 2026, when a trade deal reduced rates to 18 per cent in exchange for abandoning Russian crude imports and committing USD500 billion in American purchases, the price of alignment made explicit. South Africa faces 30 per cent tariffs as a BRICS member.

The United States reads balanced engagement as strategic ambiguity and responds with punishment. Every pathway available to African policymakers has fatal flaws. Strategic autonomy depletes leverage while Chinese lock-ins deepen. Full US alignment excludes contaminated countries where most leverage exists. The Carney Model of middle-power coalition-building requires coordination capacity Africa lacks within the leverage window.

The Coalition of the Eligible is the least bad pathway. It operates on two tracks: Track A for countries and assets with clean access to absorber markets, Track B for countries where US access is effectively closed due to BRICS membership or contamination but where EU and UK access remains available. Both tracks share a common purpose: building the capital, technology, and institutional capacity that eventually enables genuine autonomy.

The Coalition is transitional. Its purpose is to serve as a bridge to domestic depth, not permanent Western alignment. The goal is accumulating the foundation that makes future autonomy viable. Without this bridge, Africa arrives at the post-leverage world with nothing built. This analysis is conditional. It assumes mineral-led industrialisation remains Africa’s strategic objective. Whether that objective is correct (whether agriculture, services, technology, or other sectors offer more viable pathways) is a question this working paper does not attempt to answer.

What follows establishes the least bad path if the mineral route is pursued.

I. The Rupture

On 20 January 2026, Mark Carney addressed the World Economic Forum in Davos with a message that has defined the subsequent discourse: the global trading system is experiencing a rupture, not a transition. The distinction matters. Transitions imply managed adjustment, gradual reorientation, time to position. Ruptures create discontinuity. The rules that governed the previous era no longer apply. New rules have not yet stabilised. For decades, countries like Canada prospered under what Carney called the rules-based international order.

The story was partially false (the strongest would exempt themselves when convenient) but the fiction was useful. It provided a framework for trade, investment, and cooperation that benefited middle powers. That fiction has ended. Great powers can afford to go it alone. They have the market size, the military capacity, and the leverage to dictate terms. Middle powers do not. The Carney prescription follows: when we only negotiate bilaterally with a hegemon, we negotiate from weakness. We accept what is offered.

We compete with each other to be the most accommodating. This is not sovereignty. It is the performance of sovereignty while accepting subordination. The alternative is combination. In a world of great power rivalry, the countries in between have a choice: compete with each other for favour, or combine to create a third path with impact. If you are not at the table, you are on the menu. The evidence of rupture arrived simultaneously across multiple fronts. On 29 January 2026, British Prime Minister Keir Starmer landed in Beijing with sixty business executives, the highest-level UK delegation to China in years.

The UK trade deficit with China has widened sharply. Starmer’s message was pragmatic necessity: like it or not, China matters for the UK. In January 2026 alone, Xi Jinping hosted the leaders of Canada, Ireland, Finland, South Korea, and the United Kingdom. Beijing is weaponising access to its market while Western allies compete for favour. The same week, the European Union finalised terms on its trade agreement with India, eliminating 96.6 per cent of tariffs on EU exports to a market of 1.45 billion people.

The EU-Mercosur agreement, signed in Asunción on 17 January 2026 after twenty-five years of negotiation, now faces a turbulent ratification phase. Just four days after signing, the European Parliament voted to refer parts of the deal to the European Court of Justice for legal review, a process that could delay final ratification by months or years. Five EU member states voted against: Austria, France, Hungary, Ireland, and Poland, largely due to agricultural sector pressure. The European Commission is pushing for provisional application of trade provisions while the legal review proceeds.

Secretary of State Marco Rubio convenes a Critical Minerals Summit in Washington on 4 February 2026, pressing African delegations on supply chain commitments. Each of these developments reflects the same underlying dynamic. The major economies are scrambling to secure supply chains, lock in market access, and position themselves for a trading environment that no longer operates on multilateral consensus. Those who secure position survive. Those who hesitate find themselves on the menu rather than at the table.

The same day Starmer landed in Beijing, on 29 January 2026, Zambian President Hakainde Hichilema addressed the diplomatic corps in Lusaka. His message could not have differed more sharply from Carney’s prescription. We are too small, Hichilema said. Do not drag us into your geopolitics. The contrast is instructive. Carney leads a country of forty million people with 75 per cent export dependence on the United States. His response to American pressure has been to pursue twelve trade deals across four continents in six months, sign an agreement with China on electric vehicles, and tell the Trump administration directly: I meant what I said.

Hichilema leads a country rich in copper, positioned at the heart of the Lobito Corridor, holding leverage that Carney would trade significant resources to possess. His response has been to accept yuan-denominated royalties and mining tax payments, declare neutrality, and request that great powers leave Zambia out of their competition. Canada can afford to pursue strategic diversification because it has something to offer every partner. Zambia has chosen to wait for favourable terms rather than extract value from its position.

One approach builds leverage. The other watches leverage erode. Canada’s experience offers a cautionary template. Within days of Prime Minister Carney’s Davos speech declaring the rules-based order in rupture, the United States responded with tariff threats, rescinded diplomatic invitations, and reportedly engaged Alberta separatists seeking independence. Treasury Secretary Bessent publicly claimed Carney had “walked back” his remarks, a claim Carney denied from Ottawa: “To be absolutely clear, and I said this to the president, I meant what I said in Davos.” The episode illustrates the costs of even rhetorical defiance.

Canada is a G7 member, NATO ally, with integrated North American supply chains. African states lack comparable leverage. If Canada faces immediate retaliation for stating the obvious, the space for African diplomatic ambiguity is narrower still. As geopolitical analyst Velina Tchakarova observed in January 2026: “Middle powers incorporated into the plethora of American security and defence networks don’t have the choice of equidistance between America and China as they’ll be confronted with the reality of picking a side amid the New Cold War.

Or decouple from the US.” Her strategic foresight identifies Africa (particularly the Horn and Sahel) as a zone of growing volatility precisely because it sits outside established alliance structures, making it contested terrain where supply chain securitisation and raw materials access drive alignment pressure. The forced choice is now explicit. The question is not whether to choose. The question is whether to choose deliberately, extracting value for the choice, or by default, receiving nothing.

II. The Trade Reality

The Reversal

In 2000, total trade between China and Africa stood at USD11.67 billion. The relationship was relatively balanced. By 2025, China-Africa trade had reached USD295 billion, with African exports at approximately USD108 billion and imports from China at USD187 billion according to MOFCOM data. China has been Africa’s largest trading partner for sixteen consecutive years. US-Africa trade peaked at USD66 billion in 2008, then collapsed toward 2000 levels. UNCTAD data confirms the structural shift: Africa’s trade dependence on China has become systemic.

The Composition

The volume shift matters less than what moves through these corridors. 89 per cent of Africa’s exports to China come from extractives: crude oil, copper, iron ore, cobalt, and aluminium. 6 per cent is agriculture. 5 per cent is manufacturing. In the opposite direction, 94 per cent of China’s exports to Africa are manufactured goods. Africa exchanges rocks for finished goods. By 2025, Africa’s bilateral goods deficit with China was roughly USD80 billion.

The Surplus

In 2025, China’s goods trade surplus reached USD1.19 trillion. Exports rose 5.5 per cent year-on-year while imports remained flat. Exports to Africa surged 25.8 per cent. Since 2019, Chinese export volumes have risen 40 per cent while import volumes have risen 1 per cent. Standard Bank analysis shows 2025 retail sales growth of 2.7 per cent for the year, with growth slowing into outright decline by December. Household consumption remains stuck around 39.9 per cent of GDP. Real retail sales remain well below their pre-pandemic trend, with a gap of roughly ten trillion yuan of missing consumption.

This is export pressure being pushed outward. Africa is among the fastest-growing destinations for that push.

The Debt Composition

More than 42 per cent of African external debt is owed to private creditors. 23 per cent is owed to bilateral creditors. 34 per cent is owed to multilateral institutions. A 2022 study found that approximately 35 per cent of Africa’s external debt is held by Western banks, asset managers, and oil traders, compared to 15 per cent by Chinese lenders. The China debt trap narrative is overstated in volume terms. The issue with Chinese lending is structure, not volume: tied procurement, yuan denomination risk, opacity in contract terms, and technology hoarding remain problematic regardless of debt stock size.

III. The Surplus Economy Trap

The Absorber Distinction

The structural distinction that governs industrial outcomes is between absorber and surplus economies. Absorber economies run persistent current account deficits. They consume more than they produce. They can purchase African manufactures. The United States is the paradigm: household consumption at 68 per cent of GDP. The European Union stands at 52 per cent, the United Kingdom at roughly 60 per cent. Surplus economies run persistent current account surpluses. They produce more than they consume. They cannot absorb African manufactures because their domestic industries compete for the same export markets. China is the paradigm: household consumption at 39.9 per cent of GDP, record trade surpluses.

Why China Cannot Absorb

Michael Nicoletos’s analysis, published in January 2026, documents what he calls the elephant no one wants to see: China’s economic model is structurally broken. Private consumption at 39.9 per cent of GDP is low by international standards and below China’s own historical average of 49.4 per cent. The structural problems are severe. The property collapse between 2021 and 2024 destroyed between USD7 trillion and USD8 trillion in household wealth. Twenty-five to thirty-four million personal loan defaults occurred in 2024 alone, double the 2019 figure.

Household debt has reached USD11.4 trillion, 60 per cent of GDP. The birth rate hit a record low of 7.92 million in 2025, down 17 per cent year-on-year. Population is projected to fall by 280 million by 2050. The worker-to-retiree ratio is collapsing from four-to-one toward 1.2-to-one by mid-century. Rebalancing would require dismantling the mechanisms that powered China’s rise: ending cheap credit to state-owned enterprises, allowing currency strengthening, redirecting spending from infrastructure to households.

Japan attempted this from 1986 and has not achieved it thirty-eight years later. China’s demographics make the challenge categorically worse. EndGame Macro analysis reinforces this diagnosis. When the GDP deflator stays below zero, the economy can keep moving in real terms while getting poorer in nominal ones. Wages lag. Profits compress. Tax receipts disappoint. Debt quietly gets heavier. Beijing’s dilemma is that another property-led or credit-heavy stimulus would recreate the imbalances that caused the slowdown.

So instead of a reflationary jolt, it chooses the grind: targeted support, administrative guidance, selective bailouts, and a slow attempt to curb overcapacity without destroying employment. Michael Pettis articulates the deeper constraint: a country cannot restructure global capital flows without also restructuring global trade flows, nor can a country change its external imbalances without either changing its internal imbalances or changing the external imbalances of its trade partners. China cannot acquire fewer dollar assets unless either it reduces its trade surplus or it acquires more assets in other countries.

The former would be extremely painful for China, while the latter means either the EU, Japan, or the developing world must run huge trade deficits to accommodate China. The EU and Japan clearly do not want to, and the developing world has limited capacity to fund giant trade deficits. For Africa, the implication is structural. If an African country processes cobalt into battery precursors and seeks to sell the output, China is not a viable market. Chinese battery precursor manufacturers compete for the same customers.

Selling value-added goods to a competitor whose industrial policy is designed to dominate those markets is a structural dead end.

The Middleman Trap

China purchases African raw materials. China processes those materials into intermediate and finished goods. China sells those goods globally. The processing stage, where value compounds through employment, technology development, and industrial learning, happens in China. The framing that Africa and China are partners in development inverts the actual relationship. Africa is an input to the Chinese export machine. The demand for African cobalt, copper, and platinum group metals is derived demand: China wants these materials to feed its processing industries, not to support African industrialisation.

IV. The Lock-In Reality

Chinese Positions

Chinese entities have been systematically securing African mineral assets for two decades. Of 166 Chinese-owned critical mineral mining projects globally, sixty-six are in Africa. 41 per cent of DRC cobalt extraction is Chinese-controlled directly. Chinese policy banks issued USD24.9 billion in Belt and Road Initiative mining loans in the first half of 2025 alone. Recent acquisitions illustrate the pace: Botswana’s Khoemacau copper mine in 2023, Mali’s Goulamina lithium deposit in 2024, Tanzania’s Ngualla rare earth project in 2025.

BYD has secured feedstock from six African lithium mines through offtake agreements extending to 2032. Sicomines in the DRC operates under 68 per cent Chinese ownership with contracts extending through the 2040s, covering ten million tonnes of copper and 600,000 tonnes of cobalt over twenty-five years. These are ownership positions that persist.

Supply Chain Control

The dominance extends beyond extraction. China controls approximately 70 per cent of global critical mineral refining capacity, rising to 90 per cent for graphite and rare earth refining, and 60–70 per cent for lithium and cobalt refining. It produces approximately 70 per cent of rare earth minerals, 93 per cent of high-strength rare earth permanent magnets, and 95 per cent of heavy rare earth processing. It manufactures 90 per cent of the world’s solar panels and is projected to supply 60 per cent of renewable energy capacity by 2030.

Infrastructure Control

Beyond mine ownership, Chinese entities control the infrastructure through which minerals flow. More than one-third of African ports operate under Chinese control or ownership. The TAZARA railway, roads connecting mines to ports, and logistics networks are substantially Chinese-influenced.

The Substitution Timeline

China holds 98 per cent of sodium-ion and lithium iron phosphate battery production. These technologies reduce or eliminate dependence on cobalt, lithium, and nickel. Lithium iron phosphate batteries already hold 40 per cent market share and require zero cobalt. CATL’s sodium-ion facility uses no lithium, cobalt, nickel, or manganese. Beijing is constructing an escape hatch from the very commodities it is locking in across Africa. The leverage African states believe they possess may prove more temporary than assumed.

What Remains Contestable

The existing Chinese positions are largely permanent in the near term. What remains contestable is the pipeline of new projects. Africa is under-explored. Only 10 per cent of global exploration spending occurs on the continent. New discoveries can be structured without Chinese involvement from inception.

Update, February 2026: Glencore entered a non binding memorandum of understanding for Orion CMC to acquire a 40 per cent stake in Glencore’s interests in its Democratic Republic of Congo assets, Mutanda Mining and Kamoto Copper Company. The announcement implies a combined enterprise value of about USD9 billion for these assets including debt. Orion CMC gains rights to appoint non executive directors and to direct the sale of its share of production to nominated buyers, while Glencore continues to manage the assets within the existing US DRC Strategic Partnership Agreement framework. This matters because it demonstrates that contestability now includes established Tier One assets, not only greenfield pipelines, and it shows that Washington is translating supply chain policy into capital deployment and offtake control.

V. Structural Diagnosis

Four analytical frameworks illuminate Africa’s strategic position. Each approaches the question from a different angle. Together they converge on a single verdict: Africa possesses genuine leverage in specific minerals, that leverage is time-limited, and the binding constraint is organisational capacity to capture value before the window closes.

The Value Chain Position

The journey from ore in the ground to a finished product passes through six stages: extraction, primary processing, refining, component manufacturing, final assembly, and consumption. Each stage captures a different share of total value created. Stage 1 is extraction: ore out of ground. Stage 2 is concentration and beneficiation through crushing and flotation. Stage 3 is smelting, using heat to separate metal from ore. Stage 4 is refining to purify material to battery or industrial grade specifications.

Stage 5 is manufacturing of batteries, components, and finished goods. Most African mineral production remains concentrated at extraction and primary processing. Zambia operates copper smelters; South Africa has platinum group metal refineries. But the value chain stages that command premium margins (high-purity refining to battery-grade specifications, precursor chemical production, cell manufacturing) sit overwhelmingly outside the continent. China controls approximately 70 per cent of global critical mineral refining capacity, rising to 90 per cent for graphite and rare earths.

Africa’s value capture remains compressed at the lower end of the chain. China controls the middle stages. Chinese facilities refine cobalt, process lithium, manufacture battery components. The value captured at these stages ranges from ten to 35 per cent of the final product. The United States and Europe want Stage Five: final assembly into finished goods. They want electric vehicles assembled domestically, batteries installed in their factories, the jobs and industrial capacity that come with end-stage manufacturing.

Africa provides the raw input at the beginning and serves as a consumption market at the end. The production stage, where wealth compounds through employment, technology development, and industrial learning, happens elsewhere. The framing that China and Africa are development partners obscures the value chain reality. China purchases African raw materials to feed Chinese refineries. China sells finished goods back to African consumers. The processing stage, where value accumulates, remains external. Africa sells to the middleman, buys back from the middleman, and celebrates.

Skipping the middleman to access final markets directly would require processing capacity that Africa largely does not possess.

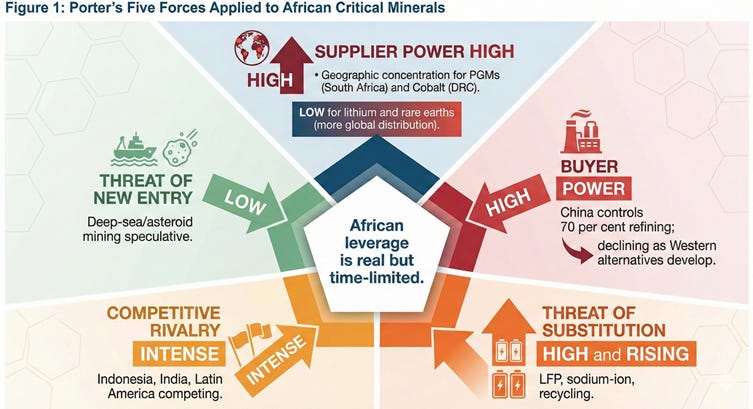

Bargaining Position: Porter’s Five Forces

Porter’s Five Forces framework assesses the competitive dynamics that shape industry profitability. Applied to Africa’s critical minerals position, it reveals where leverage exists and where it is constrained.

Supplier Power

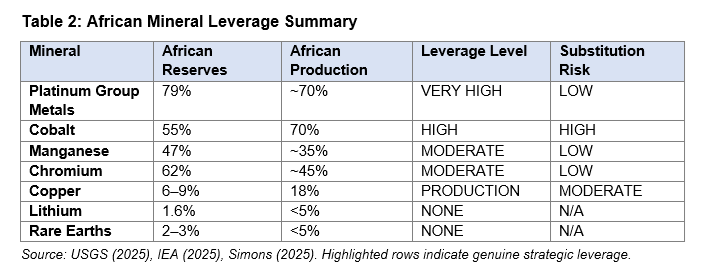

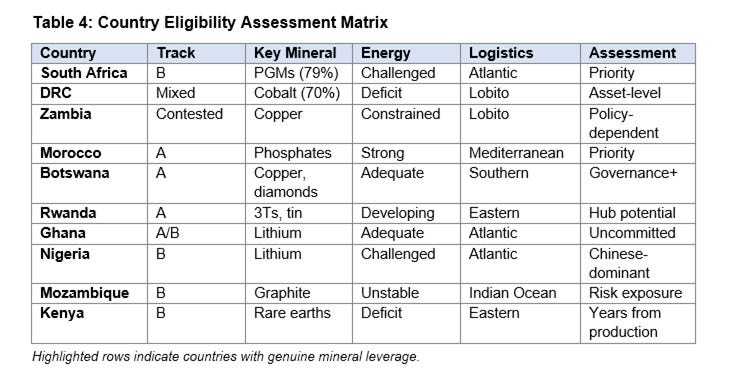

This is Africa’s source of leverage. The common claim that Africa holds 30 per cent of global mineral reserves is poorly sourced. Bright Simons of IMANI and ODI has traced this figure to a 2002 African Development Bank paper with no USGS verification. The actual data is more specific and more modest. Platinum group metals: Africa holds 79 per cent of global reserves, concentrated in South Africa’s Bushveld Complex. For PGMs, African supplier power is very high.

Cobalt: Africa holds 55 per cent of reserves and produces 70 per cent of global output, concentrated in the DRC. For cobalt, African supplier power is high but faces substitution risk. Manganese: Africa holds 47 per cent of reserves. Chromium: 62 per cent. These represent moderate supplier power with limited substitution risk. Copper: Africa holds 6 to 9 per cent of reserves but produces 18 per cent of output. DRC ore grades at 2–3 per cent copper (averaging 2.3 per cent) are exceptionally high compared to the 0.5 to 0.7 per cent global average. Production leverage exists, but copper reserves are constrained relative to African electrification and industrialisation needs.

Africa is a marginal player in lithium and rare earths, and these positions do not constitute leverage. The supplier power verdict is specific: Africa has genuine leverage in platinum group metals and cobalt, moderate leverage in manganese and chromium, production leverage in copper, and no meaningful leverage in lithium or rare earths.

Buyer Power

China’s control of 70 per cent of refining capacity (90 per cent for graphite and rare earths) gives it significant buyer power over African extractors. Chinese buyers can play suppliers against each other, demand lower prices, and dictate offtake terms. The United States and European Union are working to reduce this Chinese buyer power through supply chain diversification. American willingness to pay for secure, non-Chinese supply is high and rising. The Lobito Corridor project, backed by over USD550 million from the US International Development Finance Corporation, signals this desperation.

The European Union faces a particular constraint. Neither the US nor EU has an alternative source at scale for platinum group metals or cobalt. The difference: the US is willing to impose tariffs on South Africa anyway. The EU is not. EU-Mercosur secures niobium. EU-India provides manufacturing partnership. But neither Brazil nor India has 79 per cent of global PGMs. Neither has over 70 per cent of global cobalt production. The EU must engage with South Africa and the DRC regardless of BRICS membership or Chinese contamination. This constraint is African leverage.

Threat of Substitution

This is the clock ticking on African leverage. The timeline is more compressed than commonly assumed. Lithium iron phosphate batteries now hold 40 per cent market share and require zero cobalt. The shift from nickel-manganese-cobalt chemistries to LFP is already well advanced. Sodium-ion batteries entered commercial production at scale in 2024. CATL’s sodium-ion technology uses no lithium, cobalt, nickel, or manganese. China controls 98 per cent of sodium-ion production. Battery recycling creates urban mining alternatives to virgin extraction.

Recycling capacity is scaling rapidly in China, Europe, and the United States. The substitution verdict is sobering. The mineral leverage that exists today has an expiry date. The window is five to seven years before substitutes mature and African assets risk becoming stranded. Cobalt faces the highest substitution risk. PGMs face lower substitution risk due to their role in hydrogen fuel cells and industrial catalysis. Copper faces moderate risk as electrification proceeds regardless of battery chemistry.

Competitive Rivalry

The competition is already advanced. Indonesia introduced a raw nickel export ban in 2014 and enforced a full ban from 2020, then attracted large-scale downstream investment into processing and battery supply chains. Indonesia won the nickel race while Africa deliberated. The Indonesian nickel model offers a template the Coalition of the Eligible could adapt. By banning raw ore exports and requiring domestic processing as a condition of access, Indonesia forced capital to follow policy rather than policy following capital.

A coordinated export ban among Coalition members (covering raw critical mineral ore) would be easier to enforce among a smaller group of aligned states than across the fragmented continent. The question is whether Coalition members possess the political will to absorb short-term revenue loss for long-term value capture. The EU-Mercosur agreement secures European access to 82 per cent of global niobium reserves in Brazil. That market is now closed to African competition. Chile and Argentina’s lithium triangle offers alternatives to African lithium.

Latin American copper from Chile and Peru competes directly with Zambian and Congolese output. India may outcompete Africa for processing investment. Production-linked incentive schemes for batteries, electric vehicles, and solar manufacturing make India an attractive destination for Western companies seeking non-Chinese processing capacity. India has scale, infrastructure, English-speaking workforce, and established manufacturing ecosystems that most African countries lack.

India’s experience crystallised on 2 February 2026. After months of negotiation, Prime Minister Modi accepted President Trump’s terms: India would stop buying Russian crude (a strategic relationship dating to Cold War non-alignment), commit USD500 billion to American goods, and reduce Indian barriers ‘to ZERO’. In exchange, the combined 50 per cent tariff (25 per cent reciprocal plus 25 per cent Russia oil penalty) fell to 18 per cent. The episode demonstrates the forced choice in its starkest form. India, with 1.45 billion people and decades of defence partnership, could not preserve strategic flexibility. African states lack India’s leverage.

Threat of New Entry

Deep-sea mining remains speculative. Asteroid mining is decades away. New terrestrial discoveries in Greenland and the Arctic face environmental and infrastructure barriers. The near-term threat of new entry is low.

Porter Verdict

Africa has leverage in specific minerals where geographical concentration creates scarcity. That leverage is narrower than commonly claimed, faces substitution risk, and confronts competitor pressure. The leverage is real but time-limited. The strategic imperative is capturing value within the window, not assuming the window remains open indefinitely.

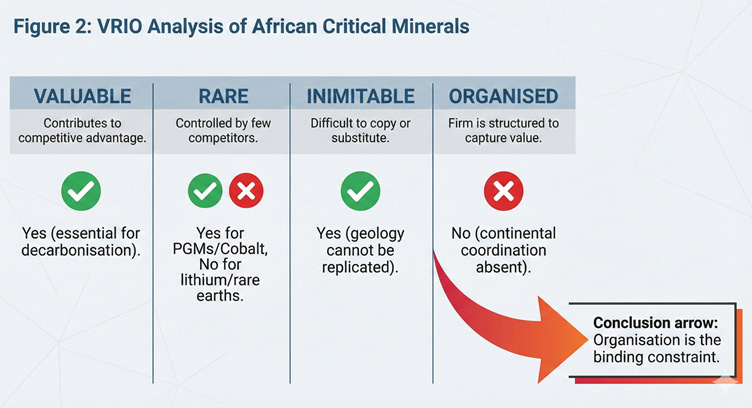

Competitive Assets: VRIO Analysis

The VRIO framework, developed by Jay Barney in 1991, assesses whether a resource can generate sustained competitive advantage. Four criteria must be met: the resource must be Valuable, Rare, difficult to Imitate, and the Organisation must be structured to capture value from it.

Value

African minerals are essential to the electrification and decarbonisation build-out. Cobalt stabilises lithium-ion battery cathodes. Platinum group metals catalyse hydrogen fuel cells. Copper enables electrification across every sector. Without these materials, decarbonisation mandates stall. The value criterion is unambiguously met.

Rarity

Cobalt deposits are geographically concentrated in the DRC to a degree unmatched by any other critical mineral. Platinum group metals are similarly concentrated in South Africa’s Bushveld Complex. The rarity criterion is met for key minerals. The rarity criterion is not met for lithium or rare earths. Africa’s 1.6 per cent of lithium reserves and 2 to 3 per cent of rare earth reserves do not constitute rarity. Multiple alternative sources exist at scale.

Imitability

Competitors cannot replicate African cobalt or PGM deposits. The geology is fixed. They can develop alternatives, substitutes, or recycling pathways, but they cannot create new Congolese cobalt reserves or new Bushveld PGM deposits. The imitability protection is partial but meaningful for the minerals where Africa has concentration.

Organisation

This is where Africa fails the VRIO test. Valuable, rare, and hard-to-imitate resources exist. The continental organisation to capture value from them does not. Fifty-four fragmented sovereigns negotiate individually against coordinated buyers. The African Continental Free Trade Area exists on paper but lacks enforcement capacity. Rules of origin remain disputed. African states have coordinated positions within multilateral frameworks: the African Group at the WTO, the ACP negotiations with the EU, Common African Positions on climate and debt.

These precedents demonstrate diplomatic capacity. Mineral coordination demands something harder: operational sacrifice with immediate costs and diffuse benefits, where individual countries face constant temptation to defect for short-term gain. The coordination problem is not diplomatic. It is structural. The organisation criterion cannot be met within the leverage window. This is the critical constraint. The strategic window is five to seven years. The Coalition of the Eligible is a partial solution to the organisation gap: asset-level eligibility architecture that builds institutional capacity over time, serving as bridge to eventual organisational capability.

VRIO Verdict

Africa holds resources that meet three of four criteria for sustained competitive advantage. The missing criterion, organisation, is the one that determines whether leverage translates into industrialisation or remains geological potential that others exploit.

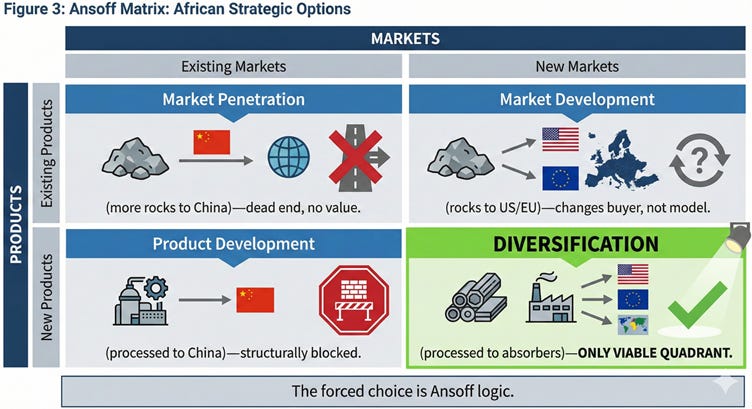

Strategic Options: The Ansoff Verdict

The Ansoff Matrix maps strategic options along two dimensions: products (existing or new) and markets (existing or new). Applied to African mineral strategy, it reveals which quadrants lead to industrialisation and which are dead ends.

Market Penetration: Existing Products, Existing Markets

This is the status quo. Shipping more raw copper and crude oil to China. The strategy generates immediate revenue but deepens exposure to a monopsony buyer while capturing zero additional value. The quadrant reinforces the extraction trap. It is a strategy of volume that changes nothing structural.

Market Development: Existing Products, New Markets

This strategy suggests redirecting raw minerals from China to the United States or Europe. While it diversifies political risk, it fails the industrial test. Selling raw cobalt to Texas instead of Jiangsu is still selling rocks. It changes the buyer but preserves the business model. Africa remains at Stage One of the value chain.

Product Development: New Products, Existing Markets

This involves processing minerals locally but attempting to sell the finished goods to China. The quadrant is structurally blocked. China imports ore to feed its own refineries. China does not import finished battery precursors that would idle its domestic capacity.

Diversification: New Products, New Markets

This is the only viable quadrant. Converting raw assets into intermediate goods (processing) and directing them toward markets that run deficits (absorbers). Selling battery precursors to US and EU supply chains is the only combination where the buyer needs the value-added product and has the structural capacity to pay for it.

Ansoff Verdict

Move to the diversification quadrant or remain trapped. The absorber markets are the new markets. Processing capacity is the new products. The forced choice is not ideological preference for Western partnerships. It is Ansoff logic: the only quadrant where African industrial upgrading can succeed is the one that combines value-added production with access to absorber markets.

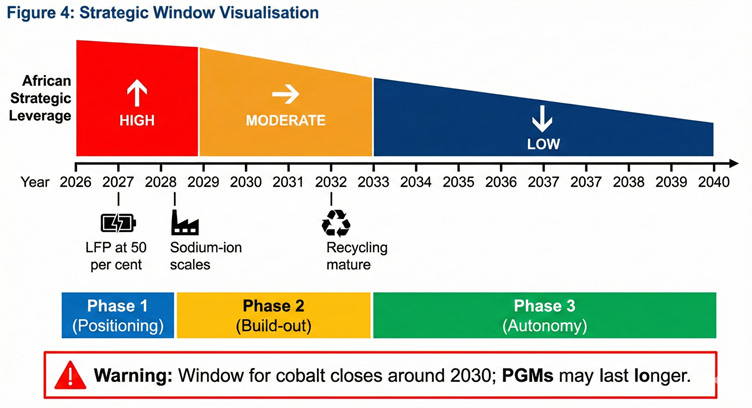

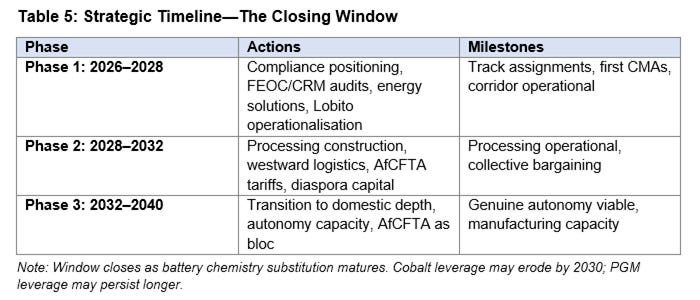

The Window

Five factors create a strategic window that will not remain open indefinitely. Substitution is accelerating. Recycling and urban mining reduce virgin extraction demand. The minerals that create African leverage today will be less critical within this window. Investment is locking in. The FEOC compliance architecture gates market access. Section 232 tariff frameworks create negotiation windows.

Investment decisions are being made now. Countries and assets not positioned for this wave will miss it entirely. Competitors are moving. Indonesia secured Chinese processing investment through export bans while Africa debated. Morocco is positioning as a battery hub. India is developing refining capacity. The first-mover advantage accrues to those who act. Coordination takes time. Building the organisational capacity that the VRIO analysis identifies as missing will take years. The window for individual countries and assets to position themselves may close before continental coordination materialises.

Political windows close. Elections in Zambia, Kenya, Nigeria, and South Africa (local government), in 2026 and 2027, create domestic uncertainty. Governments capable of making structural commitments may be replaced by governments that cannot. The alignment decisions that shape the next decade must be made by the current generation of leaders. The window is real but finite. The strategic imperative is immediate positioning, not eventual adjustment.

VI. The Leverage That Actually Exists

The discourse around African mineral leverage requires correction. The commonly repeated claim that Africa holds 30 per cent of global mineral reserves has shaped policy assumptions, investor narratives, and negotiating postures. The claim is poorly sourced and misleading.

The Thirty Per Cent Myth

Bright Simons, honorary vice president at IMANI and visiting senior fellow at ODI Global, has traced the earliest record of this claim to a 2002 African Development Bank paper. The figure has been repeated by the World Bank, UNEP, the Mo Ibrahim Foundation, and countless policy documents since then. Simons has been warning against it for more than a decade. The methodology behind the claim is unclear. It appears to conflate different mineral categories, aggregate reserves that are not strategically equivalent, and lack verification against USGS or geological survey data.

Respectable international organisations still push this narrative despite its analytical weakness. When the actual data is examined, Africa’s position is more specific and more modest than the 30 per cent framing suggests.

Where Leverage Exists

Platinum group metals: Africa holds 79 per cent of global reserves, with South Africa’s Bushveld Complex containing the vast majority. This is genuine concentration. There is no alternative source at scale. The leverage is real. Platinum group metals serve applications beyond hydrogen fuel cells. Palladium remains critical for catalytic converters in internal combustion vehicles, a market that will decline but not disappear within the leverage window. Rhodium is essential for automotive emissions control with no viable substitute.

Cobalt: Africa holds 55 per cent of reserves and produces 70 per cent of global output. The DRC dominates both reserves and production. The leverage is real but faces substitution risk from LFP and sodium-ion battery chemistries. Manganese: Africa holds 47 per cent of reserves, concentrated in South Africa and Gabon. The leverage is moderate with limited substitution risk. Chromium: Africa holds 62 per cent of reserves, concentrated in South Africa. The leverage is moderate for industrial applications.

Copper: Africa holds 6 to 9 per cent of reserves but produces 18 per cent of global output. The discrepancy reflects exceptionally high ore grades in the DRC, averaging 2–3 per cent copper compared to 0.5 to 0.7 per cent global average. Production leverage exists, but reserves are constrained. If African industrial output doubled, the continent might become a net importer of copper for its own development needs. The nuclear dimension warrants attention. The United States is accelerating small modular reactor deployment domestically and positioning nuclear as dispatchable clean baseload.

Africa’s energy deficit and uranium reserves in Niger, Namibia, and South Africa create potential alignment between American nuclear ambitions and African energy needs, a negotiation dimension not yet explored in current frameworks.

Where Leverage Does Not Exist

Lithium: Africa holds 1.6 per cent of global reserves. Chile, Argentina, and Australia dominate. Africa is a marginal player entering an established market. This is not leverage. Rare earths: Africa holds 2 to 3 per cent of global reserves. Only Madagascar and Nigeria produce significant quantities, together accounting for under 5 per cent of global output. The claim that Africa is rich in rare earth minerals is factually incorrect. The entire rare earth market is projected at approximately USD8 billion by 2032, less than half what Ghana alone earns from gold.

Nickel: Africa holds 5.6 per cent of reserves. Indonesia dominates global production. Africa has no meaningful position.

Strategic Implications

The narrow but real leverage has strategic implications that differ from the broad leverage narrative. Focus matters. African mineral strategy should concentrate on the minerals where genuine leverage exists: platinum group metals, cobalt while the window lasts, manganese, chromium, and copper production. Dispersing effort across minerals where Africa has no meaningful position wastes resources and credibility. Time matters more than previously assumed. Cobalt leverage faces substitution within five to seven years.

PGM leverage may last longer if hydrogen fuel cells scale. Building strategy around a fifteen-year window when the actual window may be half that risks stranded positioning. Competition is real. Africa competes against Latin America, Australia, Indonesia, and India. EU-Mercosur has already secured 82 per cent of European niobium supply. The minerals where Africa lacks concentration are markets where Africa is a price-taker, not a price-maker. Conservation deserves consideration. Simons’ STRIVE framework prioritises minerals for African industrialisation: copper, phosphates, aluminium, manganese, iron ore.

These are bulk-industrial minerals needed for Africa’s own development. The minerals Western supply chains want for electric vehicles may not be the minerals Africa should export. A strategy that ships everything westward may leave Africa importing the very minerals it needs to develop.

VII. The Contamination Problem

The countries where Africa’s mineral leverage is concentrated are the same countries where access to US markets is most compromised. This is the contamination problem, and it fundamentally shapes the viability of any alignment strategy.

Country-Level Contamination

South Africa is a BRICS member and has faced 30 per cent US tariffs since August 2025. The country-level contamination affects all South African assets regardless of their individual ownership structure. 41 per cent of DRC cobalt extraction is directly Chinese-controlled. The Sicomines consortium operates under 68 per cent Chinese ownership with contracts extending through the 2040s.

Chinese entities hold substantial positions across the DRC mining sector. Zambia is a major copper producer with exceptionally high ore grades. In October 2025, Zambia accepted yuan-denominated royalties and mining tax payments. President Hichilema’s public positioning has emphasised non-alignment and neutrality. The posture signals strategic ambiguity that US policy reads as insufficient commitment. Zambia’s positioning has been more complex than simple neutrality. In 2025, Zambia declined to sign a US health cooperation agreement that appeared tied to critical minerals access commitments.

Simultaneously, Zambia moved toward yuan-denominated royalty and tax payments without securing corresponding beneficiation requirements. The pattern suggests tactical manoeuvring rather than strategic clarity: accepting Chinese payment terms while resisting American conditionality, without extracting processing commitments from either side.

The Governance Capture

Chinese commercial influence often extends into governance structures. Board seats, offtake agreements, infrastructure dependencies, and local political relationships create leverage beyond direct ownership percentage figures. A mine may show 30 per cent Chinese ownership on paper while operating under Chinese operational control through management contracts or exclusive purchasing arrangements. The contamination propagates through supply chains.

The red line is effective control.

Asset-Level vs Country-Level Analysis

Contamination analysis must operate at both country and asset levels. South Africa is contaminated at country level through BRICS membership and tariff status. But specific South African assets with clean ownership chains might qualify for Track B positioning through EU markets that face no alternative. The DRC presents mixed contamination. Some assets are directly Chinese-controlled. Others, like the Kamoa-Kakula complex under Canadian and South African ownership through Ivanhoe Mines, may qualify for Track A positioning at asset level despite country-level complications.

Zambia’s contamination is positioning-based rather than ownership-based. Western-owned assets exist. The complication is governmental posture, not mine ownership.

The Eligibility Architecture

The two-track framework responds to contamination realities. Track A serves clean countries and assets. Track B serves contaminated countries and assets where US access is effectively closed but EU access remains available due to European structural constraints. The distinction is not permanent assignment. Countries can shift tracks through policy changes. Assets can shift tracks through ownership restructuring. The framework acknowledges current contamination while creating pathways for repositioning.

February 2026 provides a live example of how asset level eligibility can be engineered inside a contaminated country. Glencore agreed a non binding memorandum of understanding for Orion CMC to acquire a 40 per cent stake in Mutanda Mining and Kamoto Copper Company. Orion CMC obtains non executive board representation and the right to direct the sale of its share of production to nominated buyers. The structure targets effective control and traceable offtake without transferring operatorship. It is Track A design logic inside Track B geography.

VIII. The European Imperative

The European Union faces structural constraints that create African leverage regardless of American punishment. This section examines why the EU must engage with Africa on critical minerals, even where the United States has imposed barriers.

The Concentration Problem

For platinum group metals, there is no alternative to South Africa. Russia has some production but is sanctioned. Secondary sources exist but cannot approach the scale the EU requires for automotive catalysts and hydrogen economy development. For cobalt, there is no alternative to the DRC. The Congo produces 70 per cent of global output. Australia has some cobalt production.

Indonesia is developing nickel laterite sources with cobalt by-products. None approaches Congolese scale. The EU-Mercosur agreement illustrates European methodology. Twenty-five years of patient negotiation to secure access to Brazilian niobium, Argentine lithium, and Latin American agricultural markets. The EU negotiates slowly but eventually secures what it needs. The same patience will be applied to African critical minerals.

The EU Critical Raw Materials Act

The Critical Raw Materials Act establishes benchmarks for European supply chain security. By 2030, the EU must extract 10 per cent of its critical mineral needs domestically, process 40 per cent domestically, and recycle 15 per cent. The remainder must be sourced from secure partners with diversified supply chains. These targets cannot be met without African supply. The EU lacks domestic PGM deposits. European cobalt sources are negligible. The arithmetic forces engagement with South Africa and the DRC regardless of their geopolitical positioning.

The Act creates compliance architecture analogous to American FEOC provisions. Supply chain traceability, sustainability requirements, and governance standards gate market access. But the standards are structured differently, creating space for countries that cannot access American markets.

The European Flexibility

Europe’s approach to contamination differs from America’s. BRICS membership triggers American tariffs but does not automatically exclude countries from European supply chains. The EU maintains engagement with South Africa despite BRICS membership. European pragmatism allows what American punishment forbids. This flexibility is not unlimited. The EU will currently “not purchase” from “sanctioned” Russian sources. Chinese-controlled assets face scrutiny under supply chain security provisions. But the space for African engagement is wider than American markets offer.

UK Positioning

The United Kingdom occupies a middle position. Britain faces tariff exposure from Washington despite the special relationship. The UK trade deficit with China has widened to GBP42 billion. Prime Minister Starmer’s Beijing visit with sixty business executives signals pragmatic hedging rather than full alignment with American punishment approaches. The UK is a smaller absorber market than either the US or EU. But UK critical minerals frameworks exist, and UK flexibility on contamination questions may exceed American rigidity.

For contaminated African assets, UK market access may remain available alongside EU access.

IX. The Monetary Weapon

The forced choice operates in currency as well as trade. Yuan exposure creates vulnerabilities that compound the alignment question.

The Chokehold Mandate

Analysis from Tindale and others has identified a mechanism by which supply chain dominance captures monetary policy. Central banks require confidence in disinflation to cut interest rates. If input costs are subject to external disruption, that confidence is harder to achieve. China’s supply chain tools include administrative latency through licensing queues and inspections, specification control that makes high-purity materials scarce while low-grade materials fill volume, benchmark governance through thin liquidity manipulation, trade finance pressure through shorter terms and higher collateral requirements, and destination-based differentiation that favours preferred partners, defined not only by political alignment but by payment currency, creating incentives for yuan adoption.

The implication is that central banks operate mechanisms designed for closed loops, yet inputs are now externally governed. Chinese supply chain position affects Western monetary conditions through channels that do not require explicit weaponisation.

The Yuan Trap

Yuan exposure creates a different vulnerability than dollar exposure. The renminbi is not organically offshore. It does not circulate globally independent of Beijing’s control. Offshore yuan liquidity is deliberately managed. If an African country holding significant yuan-denominated debt experiences a shift in its relationship with China, yuan liquidity can be tightened precisely when refinancing is needed. This does not require formal sanctions or international coalition. It requires only the administrative controls China already maintains as part of capital account management.

The risk is asymmetric and additive. Adopting the yuan does not allow an African state to exit the dollar system. Global energy, food, and 88 per cent of foreign exchange transactions remain dollar-denominated. Yuan adoption forces countries to serve two masters. A liquidity squeeze from either Washington or Beijing threatens solvency. Zambia’s acceptance of yuan-denominated royalties and mining tax payments in October 2025 illustrates the trap. The decision does not liberate Zambia from dollar exposure.

It adds yuan exposure on top. The country now has two potential choke points rather than one. The strategic intent is now explicit. On 1 February 2026, China’s Communist Party journal Qiushi published remarks from President Xi Jinping calling for the renminbi to become “widely used in international trade, investment and foreign exchange markets, and attain reserve currency status.” Xi outlined three institutional pillars: a “powerful central bank,” globally competitive financial institutions, and international financial centres capable of attracting global capital.

The timing (amid dollar weakness, Federal Reserve leadership transition, and escalating trade tensions) signals Beijing’s assessment that the global monetary order is entering a contested phase. Yet structural constraints remain binding. The renminbi accounts for barely 1.93 per cent of global reserves versus the dollar’s 57 per cent. Capital controls prevent full convertibility. And China’s persistent trade surpluses mean it does not export renminbi liquidity through deficit-financed trade absorption. Instead, renminbi liquidity is distributed primarily through administrative and policy channels, including central bank swap lines and Belt and Road financing, rather than through the deep, deficit-driven capital markets that underpin true reserve currency status.

Ambition and capability remain misaligned.

Note: A managed offshore RMB loop can still function as a trade currency within a bloc without China running a current account deficit. If commodity exporters accumulate RMB through oil and metals sales, they can recycle those balances by lending RMB to deficit importers purchasing Chinese goods. Trade can therefore clear in RMB even when China is not a direct party to every transaction.

The constraint is scale and permanence. A circulating trade credit stock is not the same as a reserve asset stack. The moment surplus holders seek a deep, hedgeable store of value and a credible exit that is not contingent on political rollover, the system encounters the same bottleneck: the availability of credible RMB assets, reliable convertibility, and a lender-of-last-resort function that extends offshore under predictable rules.

Dollar Dominance

The dollar’s position remains structurally entrenched despite diversification rhetoric. In energy markets (oil and gas), approximately 90 per cent of global trade remains dollar-denominated, challenged by BRICS initiatives but still the standard. In food markets (grains), dollar dominance is estimated at around 90–95 per cent, near-total. In global reserves, the dollar’s share stands at approximately 57 per cent, slowly declining from about 70 per cent in 2000 but still dominant.

The structural point is that dollar dominance constrains African bargaining. Critical mineral exports priced in dollars flow through dollar-clearing systems subject to US jurisdiction. Diversification into yuan-denominated trade does not escape this constraint; it merely shifts Africa from one great power’s currency hegemony to another’s.

The Miran Treasury Strategy

Analysis from Miran and others suggests the United States is actively building capacity to weaponise financial channels more aggressively. The strategy involves using tariffs to force adjustment and disrupt surplus recycling, dollar weakening to restore US competitiveness, Treasury restructuring to remove the reserve veto by which foreign holders could punish US policy through bond sales, and stablecoins and AI to stabilise the transition. If this strategy proceeds, financial weaponisation follows after insulation is achieved.

The US would have greater freedom of action against partners deemed insufficiently aligned. On 30 January 2026, the US Treasury declared the yuan “substantially undervalued” and called on China to allow it to strengthen “in a timely manner.” This is the opening of a new front. Analysts including Brad Setser estimate the renminbi remains 10–15 per cent undervalued on a trade-weighted basis, though the precise figure depends on methodology. Goldman Sachs analysis in December 2025 estimated undervaluation as high as 25 per cent using their GSDEER and GSFEER models.

Any yuan appreciation is likely to be gradual. China’s export-dependent growth model and weak domestic consumption create structural resistance to sustained currency strengthening. The U.S. Treasury’s designation signals intent but does not compel action, and African policymakers should not assume yuan appreciation will materialise quickly enough to alter current trade dynamics. At present, renminbi financing does offer a relative cost advantage, particularly where policy banks, swap lines, or concessional terms are involved.

At the same time, policymakers should recognise the risk asymmetry. If yuan appreciation were to accelerate unexpectedly, governments that borrowed in yuan to escape dollar dependency would face higher debt service costs as the yuan strengthens against their currencies.

The Federal Reserve leadership transition introduces an additional variable. With Kevin Warsh reported as a leading candidate to succeed Jerome Powell, market expectations have shifted toward potentially lower U.S. interest rates. If dollar funding costs decline while China’s internationalisation efforts push renminbi funding costs higher, today’s cost advantage could narrow or reverse. In that scenario, the marginal cost advantage of dollar financing could widen rather than narrow, reinforcing dollar centrality in African trade finance precisely when some policymakers assume diversification will become easier.

For African countries holding yuan-denominated debt, this creates an additional vulnerability. If the United States forces yuan appreciation as part of trade negotiations with China, African borrowers would face rising debt service costs. What is currently framed as relief from dollar exposure risks becoming a new form of currency trap.

X. The US Policy Architecture

Understanding the forced choice requires understanding the specific policy mechanisms through which the United States gates market access. These are legislative requirements with binding legal force, not diplomatic preferences subject to negotiation.

The Inflation Reduction Act and FEOC

The Inflation Reduction Act of 2022 created a compliance architecture that determines which critical minerals can enter US supply chains. Section 30D Clean Vehicle Credits terminated on 30 September 2025, but the broader Foreign Entity of Concern provisions remain operative and continue to gate market access through the expanded framework. FEOC contamination propagates through the entire value chain. A single Chinese equity stake at any stage contaminates all downstream output. Under the latest FEOC interpretations, ownership is no longer the sole determinant of eligibility.

The red line is effective control. A mine may be wholly owned by an African pension fund, but it will be disqualified from IRA-eligible supply chains if a Chinese firm holds board seats, marketing rights, or significant operational influence. The asymmetry is structural. Chinese capital has a disincentive to build African processing capacity because every African refinery cannibalises existing Chinese facilities. Western capital faces no such constraint. When African governments mandate local beneficiation, Western firms must either build local capacity or lose market share to compliant competitors.

This asymmetry is the structural opportunity. The contrast between Chinese and American approaches is instructive. China’s primary goal is to feed domestic industry; when facing export bans, it negotiates for special exemptions; it prefers raw or semi-processed inputs that feed Chinese refineries. The United States’ primary goal is to secure compliant supply; when facing export bans, it seeks to build local or regional processing hubs to maintain access; and it is open to full precursor chemical production on African soil. This asymmetry creates African leverage that Chinese capital cannot match.

The One Big Beautiful Bill Act

The One Big Beautiful Bill Act, passed as Public Law 119-21 in 2025, expanded the FEOC framework from the original seven tax credits to a comprehensive structure governing critical mineral supply chain eligibility. The legislation formalises what was previously Treasury guidance into binding statutory requirements. The expansion means FEOC compliance now gates access to a broader range of incentives and market access provisions.

Pax Silica: The Mineral Iron Curtain

The Pax Silica initiative, launched by the US State Department on 12 December 2025, formalises what amounts to a mineral iron curtain. The United States, Japan, South Korea, Singapore, Australia, the United Kingdom, and Israel signed the Pax Silica Declaration, establishing a framework for critical minerals cooperation that explicitly excludes China. The Netherlands, UAE, and Qatar joined shortly after. Sectoral engagement remains possible within hard boundaries. Those boundaries are set by supply chain rules, ownership thresholds, and security definitions that absorber economies enforce through legislation.

The IRA, FEOC provisions, Section 232 tariff frameworks, and Pax Silica architecture create selection mechanisms that determine which African assets receive processing investment and which are excluded regardless of diplomatic rhetoric.

Critical Minerals Agreements

FEOC-clean African assets may not qualify for full IRA benefits unless processed in a country with a Critical Minerals Agreement with the United States. The US has signed CMAs with Japan in March 2023 and a Critical Minerals Framework Agreement with Australia in October 2025. No African country has a CMA. This gap represents the coalition’s first collective action opportunity. Bloc-level negotiation for CMAs covering eligible African countries would unlock IRA-qualifying status for compliant assets. Individual countries negotiating separately face weaker bargaining positions and longer timelines.

The coalition’s first test is whether it can achieve what bilateral negotiation cannot.

Trade Not Aid: The SIWG

The Trump administration’s Africa policy is explicitly framed as trade not aid. USAID assistance to Africa has fallen 25 per cent since 2025. Critical minerals were exempted from sweeping new tariffs, one of the few sectors so protected. The exemption signals where American priorities lie. On 28 January 2026, Deputy Secretary of State Christopher Landau and African Union Commission Chairperson Mahmoud Ali Youssouf signed an agreement in Addis Ababa establishing the US-AUC Strategic Infrastructure and Investment Working Group.

The joint statement is explicit: the SIWG will provide a foundation for durable, profitable investments to drive economic goals in place of foreign assistance. The priorities are equally explicit: critical minerals and commodities supply chains, transportation corridors, energy networks, and regulatory harmonisation aligned with PIDA and AfCFTA. The African Growth and Opportunity Act lapsed on 30 September 2025, placing approximately 1.3 million African jobs at risk. The House of Representatives passed a three-year extension on 12 January 2026 by a vote of 340 to 54.

The Senate approved only a one-year extension to 31 December 2026 in its appropriations bill on 30 January 2026. South Africa’s continued participation remains pending White House decision given the 30 per cent tariff already imposed. The uncertainty itself is a negotiating tool. Secretary of State Marco Rubio convenes the Critical Minerals Summit in Washington on 4 February 2026, pressing African delegations on supply chain commitments. The US-DRC Strategic Partnership, signed in December 2025, offers American firms preferential access to Congolese mineral reserves.

The Lobito Corridor, backed by over USD550 million from the US International Development Finance Corporation and USD200 million from the Development Bank of Southern Africa (total USD753 million), represents the physical infrastructure of the alignment strategy.

The Technology Dimension

The strategic logic extends beyond market access and infrastructure. If African states are offering alignment in a generational reordering, the negotiation should encompass technology access (including positioning in the AI supply chain that both powers are racing to control) and debt relief from Western-held obligations. The technology dimension is not peripheral. AI is diffusing as strategic infrastructure, with compute and advanced chips treated as controlled inputs. The United States has formalised tiered approaches to chip access that follow alignment, not price.

Washington actively uses compute access as tech diplomacy, approving advanced chip exports to close partners in the Gulf while constraining adversaries. China plays its own version through platforms, infrastructure, and partnerships that embed its standards and dependencies. Countries attempting strategic ambiguity risk delayed diffusion and second-tier capability access because neither side wants frontier technology to flow, even indirectly, to the other side. Kenya’s experience with Semiconductor Technologies Limited illustrates the volatility of American partnership.

STL received USD1.3 million from the US Trade and Development Agency in 2022 under Biden’s “friend-shoring” strategy, positioning Kenya as a potential node in diversified chip supply chains. With Trump’s return and “America First” imperatives, that partnership quietly evaporated. STL now seeks alternative funding, having secured only GBP300,000 from the UK against a USD350 million vision. The Vietnam contrast is instructive: when US support wavered, Hanoi committed USD500 million in public investment.

Today Vietnam is an emerging semiconductor hub. Kenya’s government has made no comparable commitment. The episode demonstrates that American strategic interest and American strategic commitment are not the same thing. The debt dimension creates leverage that current negotiations have not exploited. The majority of African sovereign debt is held by Western creditors, not China. This creates bargaining power for countries willing to link alignment choices to restructuring conversations. The question is whether African negotiators recognise the hand they hold.

The Conditionality Argument

The debate over Western conditionality is often framed as a clash of values: American moralising versus Chinese respect. This framing is an expensive category error. In financial terms, conditions are risk mitigation mechanisms. The interference that African elites resent, the requirements for contract enforcement, transparency, and independent courts, are precisely the structural features that lower the cost of capital in global markets. The data is unambiguous. African Eurobonds carry average yields of 9.1 per cent on dollar-denominated sovereign bonds, compared to 6.5 per cent in Latin America and 5.3 per cent in Asia for comparably rated issuers.

The Africa premium runs 200 to 400 basis points above similarly rated emerging market peers. 80 per cent of rated African sovereigns are classified as high-risk. Only Botswana and Mauritius maintain investment-grade status. Researchers have quantified that subjective elements in credit ratings, including governance assessments, cost African governments an additional USD24 billion in interest payments and USD46 billion in foregone lending over the life of various bonds. These sums could fund infrastructure, education, and healthcare.

The premium is not imposed by Western conditionality. The premium reflects investor perception of governance risk. When Western lenders demand rule of law, they are effectively requiring the borrower to lower their own risk premium. An economy with enforceable contracts and transparent data attracts capital at 6 per cent. An economy without attracts capital at 12 per cent, or not at all. Chinese financing avoids conditionality lectures but does not lower the cost of capital in global markets. The vendor financing model delivers infrastructure at inflated costs through tied procurement, not improved sovereign creditworthiness.

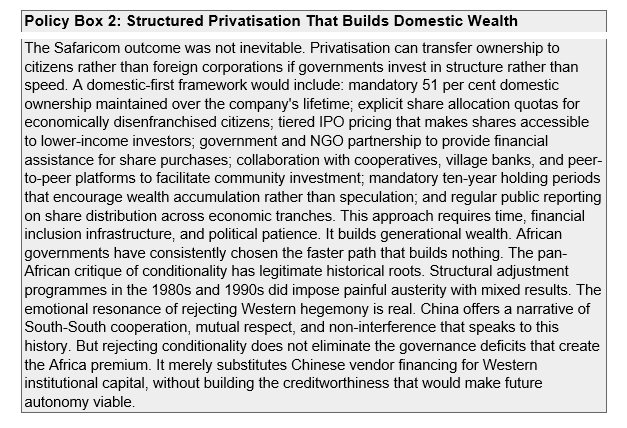

Kenya’s recent experience illustrates the stakes. In 2025, the World Bank and IMF froze loan disbursements after Kenya failed to meet eleven of sixteen agreed conditions. The IMF denied Kenya USD851 million. The conditions included restructuring Kenya Airways, boosting tax revenue, and paying suppliers. These requirements are not colonial interference. They are the prerequisites for fiscal sustainability that determines whether Kenya can access capital markets at all. The Safaricom case illustrates the pattern.

Rather than structuring a sale that would transfer ownership to Kenyan citizens through a more complex citizen-anchored process (which would require more time, financial inclusion mechanisms, and political patience), the government sold to Vodacom because it was faster. Safaricom shifted from local to foreign ownership not because no alternative existed, but because the alternative required effort that African governments have consistently declined to make at scale.

The Strategic Logic

The Trump administration’s approach is transactional and explicit. American investment flows to countries that provide supply chain security. Countries that maintain strategic ambiguity face tariff exposure and reduced access. The administration is not persuading. It is selecting. Washington’s shift from statements to capital deployment accelerated in late 2025. The DFC’s USD553 million Lobito loan in December 2025, the US-DRC Strategic Partnership signed that same month, and the Critical Minerals Summit in February 2026 signal a more active posture.

But the amounts remain modest relative to Chinese accumulated investment, and the conditionality frameworks remain incomplete. When a government that pivots toward the US faces Chinese economic retaliation, the question is whether Washington provides protection or only preference. The Kenya semiconductor case reinforces this point: Biden-era friend-shoring delivered a USD1.3 million grant and promises of partnership. Trump-era America First withdrew the commitment without replacement. Strategic interest evaporated overnight.

This is what statements without protection looks like in practice. As one Atlantic Council observer noted: if the US wants dedicated supply, that has to come with something, whether security support, infrastructure, or both. That is where the real negotiations are. The policy architecture creates the selection mechanism. The question for African policymakers is whether to be selected or excluded.

XI. The Competition Landscape

African mineral strategy operates in a competitive environment. Africa competes against other suppliers for access to absorber markets. Understanding this competition is essential to realistic positioning.

Latin America

Chile and Peru dominate global copper production and reserves. Chile and Argentina’s lithium triangle holds reserves that dwarf African lithium positions. Brazil holds 82 per cent of global niobium reserves, now secured for European supply through the EU-Mercosur agreement signed in January 2026 after twenty-five years of negotiation. Latin American suppliers have advantages Africa lacks: geographic proximity to the US market, established infrastructure, decades of reliable supply history, and political relationships that predate the current supply chain competition.

The Lobito Corridor aims to provide Atlantic routing for African copper, but Chilean copper already flows west without new infrastructure investment.

Australia

Australia exports lithium and rare earths at scale. Australian mining operates under stable rule of law, contract enforcement, and regulatory predictability that many African jurisdictions cannot match. Australia has allied status with the United States through AUKUS, removing any contamination concerns. For Western buyers seeking secure supply, Australia is a safer bet than Africa on governance risk. Australian lithium competes directly with African lithium. Australian rare earths compete with emerging African rare earth production.

Indonesia

Indonesia demonstrates what decisive policy can achieve. The 2014 raw nickel export ban, fully enforced from 2020, forced downstream investment into Indonesian processing capacity. Chinese and Korean battery manufacturers built facilities in Indonesia to access nickel supply. Indonesia now dominates global nickel processing. Indonesia won the nickel race while Africa debated. The Indonesian example is instructive for what Africa might have done. It also closes the nickel market to African competition.

India

India may prove to be Africa’s most significant competitor for processing investment. Production-linked incentive schemes for batteries, electric vehicles, and solar manufacturing create attractive conditions for Western companies seeking non-Chinese processing capacity. India has scale, infrastructure, an English-speaking workforce, established manufacturing ecosystems, and a single sovereign that can make unified policy commitments. The EU-India trade agreement integrates India into Western supply chain architecture.

Western companies choosing where to locate processing facilities face a choice between India and Africa. India offers lower political risk, better infrastructure, established supply chains, and a unified regulatory environment. Africa offers proximity to extraction but fragmented policy environments and infrastructure deficits. India’s positioning as a processing destination may outcompete African processing aspirations even if African extraction leverage exists. The minerals leave Africa regardless.

The question is whether processing happens in Africa, India, or elsewhere.

Morocco

Morocco is playing a masterful hand by leveraging its Free Trade Agreement with the United States and its proximity to Europe. In 2024, Chinese battery giant Gotion High-Tech signed a USD1.3 billion deal to build Africa’s first EV battery gigafactory in Morocco. By manufacturing in Morocco, Chinese firms can potentially mitigate exposure to US FEOC restrictions under the Inflation Reduction Act while feeding Europe’s massive EV demand. Morocco demonstrates what strategic positioning can achieve.

The Competition Verdict

Africa competes in a crowded field. For minerals where Africa lacks concentration, competition is fierce and African positions are weak. Even for minerals where Africa has concentration, competition for processing investment exists. The leverage from extraction does not automatically translate into processing capacity when alternative locations offer superior business environments.

XII. The Pathways Assessed

Five strategic pathways are available to African policymakers. Each has been proposed by credible voices. Each has structural weaknesses. The task is identifying the least bad option, not the good one.

Path One: Strategic Autonomy