Watch Your Six: The Bank of Zambia (BOZ) is Set to Tighten Further

With the Monetary Policy Committee (MPC) decision on May 15, 2024, looming large, the dynamics between the onshore and offshore USD/ZMW rates take center stage. The onshore interbank spot rate, currently at 27.325 mid, is slightly lower than the offshore rate at 27.650 mid. The significant reduction of this spread to just 0.325 kwacha, from a gap of two kwacha just a week ago, signals a noteworthy shift in market sentiment that demands our full attention, particularly in light of the upcoming MPC decision.

Several factors contribute to the tightening spread between the onshore and offshore rates. The offshore space grapples with increased funding constraints, while onshore dollar demand has noticeably decreased. However, the most influential factor is the market's anticipation of the MPC's decision, which could raise the Statutory Reserve Ratio (SRR) by a significant 850 basis points to 34.5%. With its potential to profoundly affect market sentiment and liquidity, this decision is a pivotal event that we must monitor closely.

The convergence of the onshore and offshore rates could be a precursor to a market pullback, a scenario that we need to be prepared for. If the Bank of Zambia (BOZ) continues to bolster the market with FX sales over the next few days, this pullback could be hastened. A pullback before the MPC announcement could prompt the BOZ to reassess the need for an SRR hike. Instead of an SRR hike, monetary authorities might consider a 100 basis points rise in the policy rate sufficient for this tightening round. However, given the current market liquidity, upcoming security maturities, and coupon payments, this could potentially be a misstep.

We cannot overstate the significance of June 2024, a month we have continually pointed to as pivotal to money market dynamics. The liquidity situation, currently at ZMW 0.54 billion, is on the brink of significant expansion due to the maturity of securities. Over the next seven weeks, ZMW 16.17 billion in T-bill maturities, bond maturities, and coupon payments will flood the Kwacha money market. Of such magnitude is this amount that it represents over half (51.6%) of the total security maturities and coupon payments scheduled from July to December 2024, which total ZMW 31.31 billion. Remember that this influx does not include increased liquidity stemming from fiscal expenditures.

The implications of this liquidity surge are significant and require our careful consideration. A significant chunk of the ZMW 7.99 billion bond maturities comprise non-resident holdings (NRH). Recent trends suggest these investors may choose not to reinvest, which could lead to divestment pressures from the offshore market. Furthermore, the government's upcoming auctions, intended to raise approximately ZMW 10.4 billion, could still leave a notable amount of liquidity in the kwacha money market. Assuming the auctions successfully attract the targeted amount, an excess liquidity of over ZMW 5.77 billion would remain. This surplus supports an environment where purchasing USD becomes more feasible due to the ample availability of kwacha.

While we advocate for fiscal authorities to surpass their advertised funding targets and allow yields to near 30%, especially for longer-term securities, we acknowledge a marked reluctance to increase funding costs. Although non-residents currently participate only in the secondary market, it is crucial to recognize that primary market yields often anchor with secondary market yields.

Yields approaching 30% would provide more attractive entry points for foreign investors seeking significant returns to compensate for ongoing concerns about currency weakness. Such high yields would be especially compelling without robust measures to stabilize the foreign exchange structure. Measures such as reinstating de-dollarization regulations like SI-33, redirecting mining sector tax receipts back to the foreign exchange market, or mandating economic justification for USD deposits held above a 45-day to 60-day period could alleviate some of these concerns. However, without such initiatives, higher yields become vital to draw substantial foreign portfolio investment into bonds.

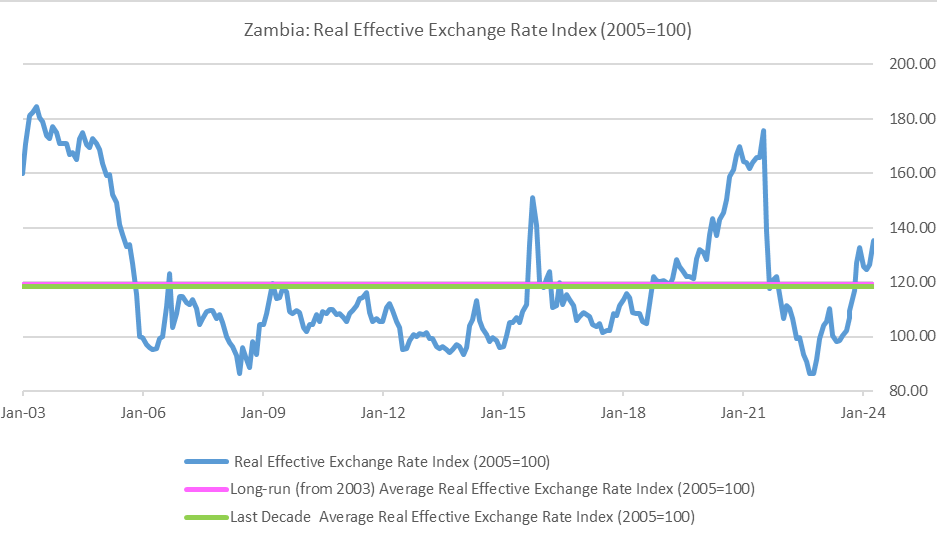

Considering these dynamics and fiscal authorities' bizarre reluctance to enforce the transfer of government deposits from commercial banks to the BOZ, the central bank should implement the proposed Statutory Reserve Ratio (SRR) increase of 850 basis points. This measure would effectively withdraw approximately ZMW 6.64 billion from circulation. Complemented by strategic dollar sales, such a decisive move could stabilize or bolster the ZMW. In the best-case scenario, this could lower the exchange rate to between 20.855 and 20.960. For baseline expectations, we project a low of around 23.390 to 23.440, while for the worst-case scenario, we could see a narrow dip to between 24.895 and 25.345. It is also important to note that, in Real Effective Exchange Rate (REER) terms, our calculations suggest that the kwacha is currently around 14% undervalued.

Dean N Onyambu is the Executive Head of Trading at Opportunik Global Fund (OGF), a CIMA-licensed fund for Africans and diasporans (Opportunik), and is a co-author of Unlocking African Prosperity. Passion and mentorship have fueled his 15-year journey in financial markets. He is a proud former VP of ACI Zambia FMA (@ACIZambiaFMA) and founder of mentorship programs that have shaped and continue to shape 63 financial pros and counting! When he is not knee-deep in charts, he is all about rugby. His motto is exceeding limits, abounding in opportunities, and achieving greatness. #ExceedAboundAchieve

For more insights from Dean, you can follow him on LinkedIn @DeanNOnyambu, X @InfinitelyDean, or Facebook @DeanNathanielOnyambu.

The Canary Compass Channel is available on @CanaryCompassWhatsApp for economic and financial market updates on the go.

Canary Compass is also available on Facebook: @CanaryCompassFacebook.