ZAMBIA MACRO NOTE: A Little Here, a Little There

The fiscal cost of Zambia’s fuel tax suspension is small. The pressures it compounds are not.

AI-generated image. Each pressure is small. The direction is not.

Yesterday we published a back-of-the-napkin estimate that the three-month tax suspension would cost the Treasury roughly ZMW3 billion to ZMW4 billion. Overnight, we refined the model. The revised range is ZMW3.3 billion to ZMW4.6 billion, depending on the conflict path, duration, and consumption growth. But the fiscal cost is not the story. The story is where that cost lands. The IMF had already identified early signs of fiscal slippage before the oil price surge. VAT collection was already under pressure. Mineral royalties are compressed by currency strength. The bond market has tightened. A ZMW14.6 billion maturity wall arrives in June. No IMF programme exists to anchor the response. The cost is manageable. Whether the quarter absorbs it depends on what else is moving.

The Intervention

On 31 March 2026, the Energy Regulation Board published the April fuel price review. On the same day, Cabinet declared the fuel supply situation an emergency. It approved the zero-rating of Value Added Tax and suspension of Excise Duty on petrol and diesel for three months, effective 1 April 2026.

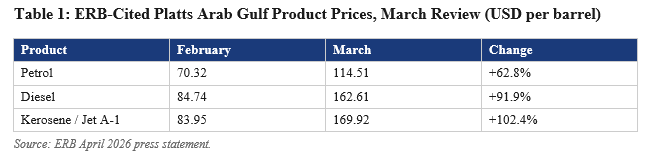

The ERB’s Import Parity Pricing model uses Platts Arab Gulf product assessments, the international benchmark that determines the wholesale cost of fuel imports into Zambia, as its top cost line.

The Kwacha depreciated 0.63 per cent over the same period, from K19.18 to K19.30.

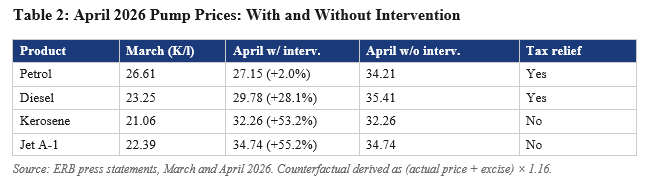

The April pump prices already reflect the removal of excise and the zero-rating of VAT. The ERB’s formula, applied without intervention, would have produced pump prices of approximately K34.21 for petrol and K35.41 for diesel. Cabinet chose to intervene.

Kerosene carries no excise duty, is exempt from VAT, and attracts zero customs duty. The tax intervention mechanism available for petrol and diesel did not exist for kerosene. It rose 53 per cent to K32.26 per litre. With national stock cover at fewer than 15 days and supply constrained to road tanker capacity from Dar es Salaam, subsidising kerosene would have risked a physical shortage. The price pass-through is the mechanism that keeps the residual market clearing. The households that cook with kerosene absorb the full shock. Not because the government chose to exclude them, but because the tax architecture offered no lever and the supply constraints ruled out a subsidy. Charcoal, the primary cooking fuel for lower-income urban households, has more than tripled since April 2019. These are the households with no domestic savings to cushion seven years of above-target inflation through investment participation. The tax suspension on petrol and diesel limits the pass-through to public transport fares, which protects the ability to get to work. It does not reach the kitchen.

The Fiscal Cost

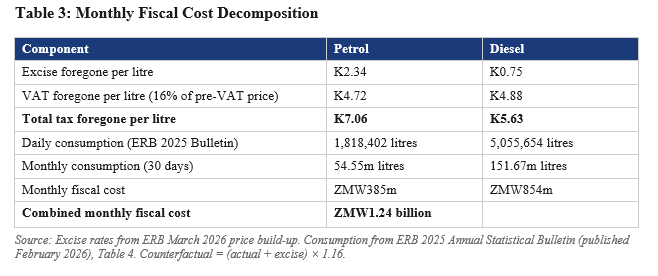

Taxes have been suspended, not spending authorised. The budget loses the revenue it would otherwise have collected.

The fiscal cost per litre equals the excise foregone plus the VAT that would have been charged on the pre-VAT counterfactual price. The counterfactual pump price equals the actual April price plus the suspended excise, multiplied by 1.16 for VAT.

The 2025 consumption figures are 11 per cent higher for petrol and 12 per cent higher for diesel than 2024. The assumption of flat consumption is conservative: demand may contract at higher prices, which would lower the fiscal cost but also signals weaker economic activity. The fiscal cost is driven by the Platts Arab Gulf benchmark, which reflects global conditions regardless of where Zambia sources its product. The supply risk is separate. If the Strait of Hormuz remains closed, physical product from the Gulf does not arrive. Indian refineries, which sit on a shorter shipping route to Dar es Salaam than the Arab Gulf and already supply East Africa, are the most likely alternative source. Nigeria’s Dangote refinery, which reached full capacity in February 2026, offers a medium-term continental option. But the immediate vulnerability is domestic: the Energy Minister disclosed petrol stock cover at 19 days on 6 March; by 19 March the Permanent Secretary reported 23 days. Both figures sit at the margin where disruption to road tanker logistics from Dar es Salaam compresses supply within weeks.

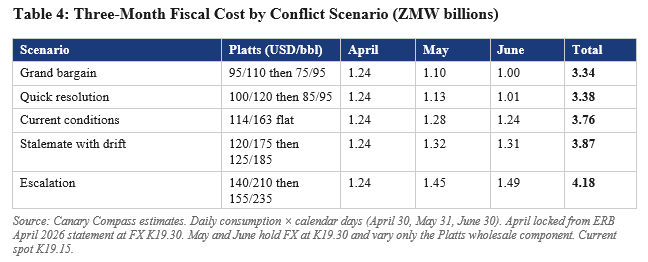

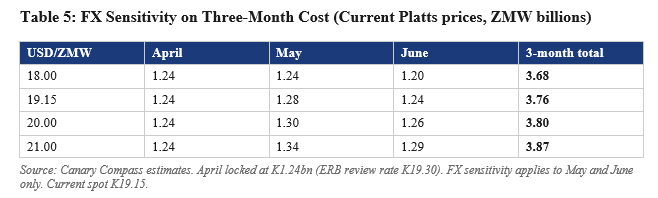

April’s cost is locked. It does not depend on where oil goes next. The question is what May and June cost under different conflict trajectories.

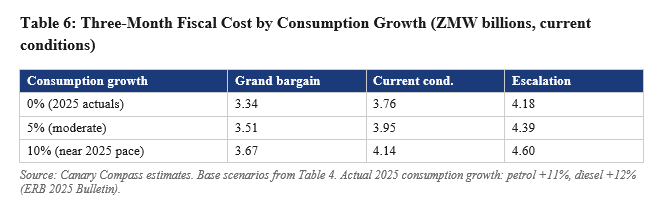

If nothing changes from where we are today, the three-month suspension costs approximately ZMW3.8 billion.

The estimates in Tables 4 and 5 use 2025 consumption volumes held flat. Consumption grew 11 to 12 per cent in 2025 and will almost certainly be higher in 2026.

The range across oil price scenarios and consumption assumptions is ZMW3.3 billion to ZMW4.6 billion for the three-month window. The three-month window is itself an assumption. If the suspension extends beyond June, every additional month adds between ZMW1.0 billion and ZMW1.5 billion depending on where oil prices settle. The pre-war baseline was approximately USD70 per barrel. Any price above that level pressures the government to maintain the suspension, and the market consensus as at end-March does not see a return to that baseline within the three-month window.

The Pressure Points

The suspension removes revenue from the top of the fiscal envelope. The economy was already underdelivering revenue from the bottom.

On 5 March 2026, the IMF staff team concluded its visit to Zambia. The statement identified “early signs of slippage” driven by spending pressures on the wage bill, agricultural support, and election-related expenditures. Absent corrective measures, the primary surplus was projected to fall by about 1 percentage point of GDP relative to the 3.8 per cent envisaged at the last ECF review. The fuel cost arrives on top of a budget that was already slipping.

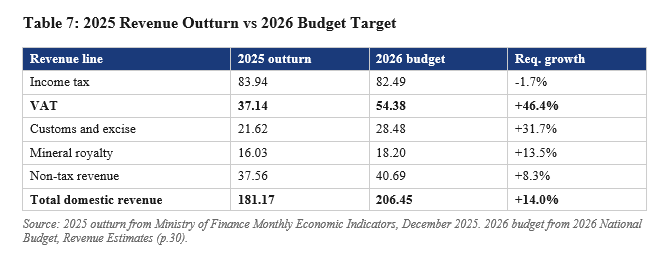

Fourth quarter 2025 GDP printed 1.6 per cent, dragging the full year to 3.8 per cent against a 2026 budget assumption of 6.4 per cent real growth. The collapse was concentrated in wholesale and retail trade, which subtracted 1.5 percentage points from Q4 value added. The revenue base entering 2026 was already under strain. The table below compares actual 2025 collections with the 2026 budget targets.

The weight falls on VAT. The collapse in wholesale and retail was most visible in domestic VAT, which reached only 34 per cent of its 2025 target. Import VAT, which accounted for 88 per cent of total collections, performed at 91 per cent. The assessment formula converts CIF values to Kwacha at the prevailing exchange rate: when the currency strengthens, every dollar of imports generates less Kwacha in tax at the border. The same mechanism compressed mineral royalties. The 2026 VAT target requires 46 per cent growth from that combined base. The Kwacha has strengthened a further 14 per cent since December. The deficit target of 2.1 per cent of GDP rests on that growth assumption.

Mineral royalties, budgeted at ZMW18.2 billion, face a separate compression. Copper averaged USD12,943 per tonne in Q1 2026, some 30 per cent above the 2025 average. But the Kwacha averaged K19.43 in Q1, roughly 23 per cent stronger than the 2025 average of K25.2. The copper price gain is almost entirely offset by currency strength. At Q1 prices and exchange rates, the budget requires approximately 17 per cent production growth to deliver the royalty target. At 10 per cent production growth, royalties annualise at roughly ZMW17.1 billion, a shortfall of ZMW1.1 billion.

The interest-to-revenue ratio stood at approximately 25 per cent before the suspension, calculated as budgeted domestic interest expense of ZMW52.0 billion against budgeted domestic revenue of ZMW206.5 billion. On the broader base of domestic revenue plus grants, the ratio is 24 per cent. The IMF’s fiscal sustainability framework flags ratios above 20 per cent.

The government’s 2026 domestic borrowing programme targets ZMW106.07 billion in market issuance. At the start of the year, the required monthly average was ZMW8.84 billion. Strong January and February auctions brought the remaining requirement to ZMW80.81 billion and the monthly average down to ZMW8.08 billion. March reversed the trajectory. The remaining requirement is ZMW75.80 billion across nine months, or ZMW8.42 billion per month. The required allocation rate against remaining offered amounts at Q1 auction sizes has climbed from 89.4 per cent to 95.2 per cent. One poor financing month was enough. The refinancing targets were difficult from the start. The government cannot afford poor financing months to continue at the same time that revenues are underperforming.

The fiscal cost must be funded. The net domestic financing authorised in the budget is ZMW21.62 billion. If revenue underperforms, the deficit widens. Funding the wider deficit domestically requires a supplementary appropriation to authorise additional borrowing, which raises the ZMW106.07 billion issuance baseline into a market that now needs to operate at 95 per cent allocation. Without a supplementary appropriation, the shortfall either compresses expenditure or adds to the domestic arrears stock, which stood at ZMW77.6 billion (USD3.25 billion) as at end-September 2025. All three options carry cost.

April and May are light on bond maturities, as March was. June is not. Per Reuters and Bank of Zambia Q1 auction results, June has ZMW14.62 billion in total maturities, of which ZMW8.29 billion is in bonds. The March auction result reflects several pressures moving at once. Exchange rate risk from the Iran situation compounds the IMF’s early revenue concerns and a GDP outturn of 3.8 per cent against expectations of 4.5 to 5.2 per cent. The global risk environment discourages frontier market exposure. The offshore bid that masked the transmission failure in February did not return. If that persists into June, new offshore investors may stay away and existing holders facing maturities may divest rather than reinvest. One undersubscribed auction is a signal, not a verdict. But the domestic market has not historically absorbed bonds at this scale without offshore participation.

The Ministry of Finance’s 2026 Monthly Economic Indicators have not been published. It is 1 April. The government just committed ZMW3.3 to 4.6 billion in tax revenue foregone over three months against a budget of ZMW253.1 billion. The IMF Extended Credit Facility concluded following its sixth review in January 2026. The Ministry of Finance stated that the government chose not to pursue an extension, directing instead that engagement on a successor programme begin immediately. The IMF’s March visit indicated otherwise: initial technical discussions could begin as early as late April, but substantive engagement would resume only after the general elections and once a new government is in place. With the ECF concluded, there are no quantitative performance criteria binding the fiscal authorities. Domestic budget ceilings can be amended via supplementary appropriation.

The government undertook to maintain fiscal discipline when the ECF was not rolled over. Timely fiscal reporting is the minimum condition for that commitment to be credible. The January indicators remain unpublished.

The Structural Point

This note does not argue that the intervention was wrong. The alternative was pump prices of K34.21 for petrol and K35.41 for diesel. That would have imposed severe hardship on households whose purchasing power eroded over nearly seven years of above-target inflation between April 2019 and early 2026. Inflation returned to the target band in March 2026, but the cumulative damage is already embedded in prices. The CPI index sits between 44 and 64 per cent above where the Bank of Zambia’s own target band would have placed it, depending on which point in the band you measure from. Individual staple commodities tell a harsher story over the same period. Charcoal sits 98 per cent above the 8 per cent ceiling path in March 2026. Maize grain sits 81 per cent above. Breakfast mealie meal 69 per cent. The government faced no viable alternative. It absorbed the cost fiscally rather than pass it to the consumer.

The structural point is different. The government exited sovereign default, completed six consecutive IMF reviews, and reached agreement in principle on 94 per cent of USD13.3 billion in external debt under restructuring. Those achievements are real. They also make the current fiscal tightness more consequential, not less. The stabilisation effort earned the space to build larger buffers. The 2026 budget assumed aggressive revenue growth and set an expenditure envelope that requires a large domestic borrowing programme to fund. The refinancing wall from the 2020-2021 issuance cycle, when the prior administration borrowed at yields between 30 and 35 per cent, concentrates maturities in this year. That wall is inherited. The revenue assumptions and expenditure commitments are not. The room had not kept pace with the stabilisation effort.

Kenya, facing the same Platts Arab Gulf price surge through its own import parity model, drew on its Petroleum Development Levy stabilisation fund. Zambia's ERB price build-up includes a Strategic Reserves Fund levy of K0.15 per litre, collected since 2005 with a price stabilisation mandate. Its balance has never been publicly disclosed. Interestingly, it was not deployed.

What this episode reveals is the fragility of Zambia's fiscal shock absorption architecture. The Strategic Reserves Fund was established for exactly this scenario and was not deployed. A commodity-dependent, import-exposed economy with no strategic fuel reserve, a stabilisation fund of undisclosed balance, and no automatic trigger for fiscal adjustment will face this choice again. The architecture that needs building is not a better subsidy. It is a fiscal buffer that is funded, transparent, and operational, making the next shock a technical adjustment rather than a Cabinet emergency.

The excise and VAT suspension reduces collections at precisely the moment the budget needs them most. The interest-to-revenue ratio worsens as the denominator shrinks. Mineral royalties are compressed by Kwacha strength. The domestic borrowing programme meets a bond market that just undersubscribed and a T-bill market trading below the policy rate. A ZMW14.6 billion maturity wall arrives in June. And we cannot assess how the budget is performing because the fiscal data has not been published.

The three-month window expires on 30 June 2026. If oil remains above the pre-crisis baseline of approximately USD70, the government faces a binary. It can extend the suspension and continue absorbing ZMW1.0 to 1.5 billion per month from a tightening revenue envelope. Or it can allow full pass-through into pump prices, with a general election scheduled for August. The political incentive to extend is obvious. The fiscal capacity to extend is not. Both options carry cost. Neither is free.

The fuel tax suspension costs 1.3 to 1.8 per cent of the budget. By itself, it is manageable. It does not arrive by itself. It arrives in a quarter where the IMF has already flagged a 1 percentage point primary surplus slippage. Revenue is under pressure from three directions simultaneously. The bond market has tightened. A June maturity cliff concentrates rollover risk in the same month the suspension expires. None of these is a crisis. All of them are moving in the same direction. A little here, a little there.

Sourcing note: Full primary source citations are available in the online publication at www.canarycompass.com. Key sources include ERB April 2026 press statement, ERB March 2026 price build-up, ERB 2025 Annual Statistical Bulletin, Cabinet resolution (31 March 2026), Bank of Zambia auction results and exchange rate data, Reuters maturity profile, ZamStats GDP and CPI data, 2026 National Budget Revenue Estimates, Ministry of Finance Monthly Economic Indicators (December 2025), Bank of Zambia Debt Statistical Bulletin Q3 2025, IMF Press Releases Nos. 26/024 and 26/073, and prior Canary Compass publications.

Disclaimer

This article does not constitute legal, financial, or investment advice. The author shares views for perspective and discussion only. Do not rely on them as a substitute for professional advice tailored to your specific circumstances. Always consult a qualified legal, financial, investment, or other professional adviser before making decisions based on this content. The analysis reflects proprietary research undertaken by Canary Compass and the author.

Canary Compass and the author accept no liability for actions taken or not taken based on the information in this article.

The views expressed in this article represent the author’s independent professional analysis and do not constitute an endorsement of any individual, institution, or position. Canary Compass and the author accept no responsibility for how this content is interpreted, excerpted, or recontextualised by third parties not involved in its production and publication. Reproducing any portion of this work in isolation, or in combination with other material, in a manner that misrepresents the author’s original meaning constitutes a distortion of the published record.

The author may hold positions in financial instruments, currencies, or assets discussed or referenced in this publication. Such positions do not constitute a recommendation to buy or sell.

All views, projections, and forecasts reflect the author’s assessment at the time of writing. Data sourced from third parties is believed to be reliable but has not been independently verified. Past performance does not indicate future results.

All content published by Canary Compass is the intellectual property of the author. Reproduction, adaptation, or redistribution, in whole or in part, requires written permission.

About the Author

Dean N. Onyambu is the Founder and Chief Editor of Canary Compass, a financial research publication focused on African monetary architecture and financial sovereignty. He brings 18 years of experience across trading, fund leadership, and economic policy, with senior roles at Standard Bank, First Capital Bank, and Opportunik Global Fund.

Read and subscribe at www.canarycompass.com.

The Canary Compass Channel is available on @CanaryCompassWhatsApp for economic and financial market updates on the go.

For more insights from Dean, you can follow him on LinkedIn @DeanNOnyambu or X @InfinitelyDean.