ZAMBIA MACRO NOTE: Seven Stars That Refuse to Align

The MPC Cuts Again. The Fiscal and Financing Convergence, May 2026.

AI-generated Image: Failed Convergence

The Bank of Zambia cut the policy rate by 25 basis points to 13.25 per cent on 13 May. In February, it cut 75 basis points. The deceleration from 75 to 25 is the concession the data extracted.

Between those two decisions, the April bond auction undersubscribed. The fiscal deficit exceeded two months’ budgeted allowance. The Finance Minister tabled a supplementary budget adding domestic borrowing from the securities market that had just rejected the government’s offering. The MPC eased. The environment into which it eased did not. This note maps the fiscal and financing evidence first, then assesses the monetary policy decision against it.

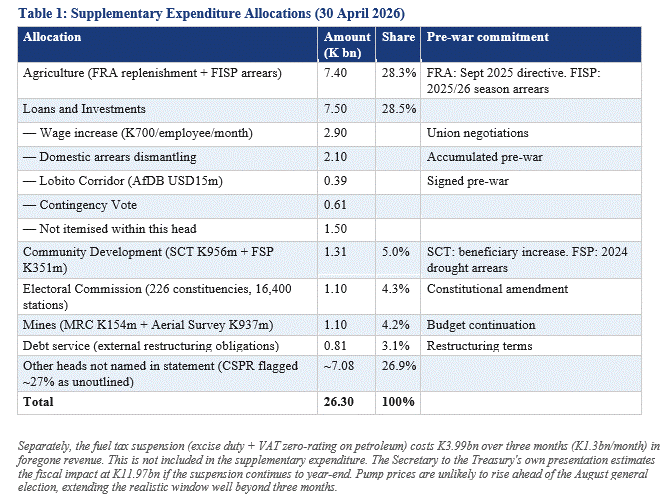

The Supplementary Budget

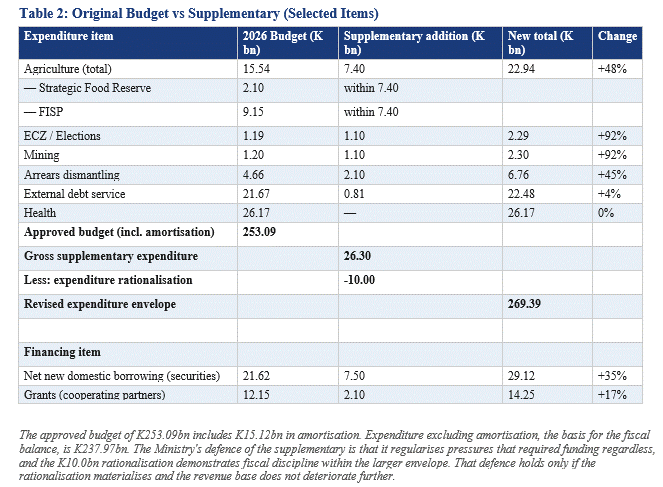

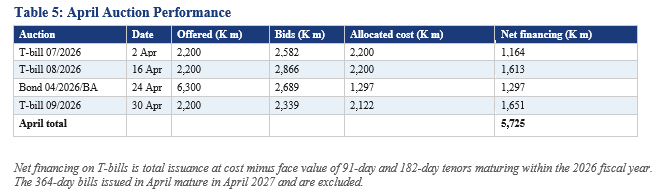

On 24 April 2026, the Government of the Republic of Zambia offered K6.3bn in bonds to the domestic market. The market bid K2.7bn, a subscription rate of 43 per cent. The government allocated K1.3bn, rejecting higher-yielding bids. Six days later, on 30 April, the Finance Minister tabled Supplementary Estimates No. 1 of 2026 in the amount of K26.3bn. The financing plan includes K7.5bn in additional net domestic borrowing from the same securities market. This K7.5bn financing figure is separate from the K7.5bn expenditure allocation under Head 21 (Loans and Investments); the first is a source of funds, the second a use.

The supplementary invites attribution to the Iran war. The composition does not support it as a direct cause. The war is cited as context in the ministerial statement: “the war in the middle east which has led to Government foregoing about US$200.0 million in 3 months, thereby affecting several macro and fiscal parameters.” That USD200m in foregone fuel tax revenue is real and sits on the revenue side. It is not an expenditure item within the K26.3bn. The supplementary expenditure allocations are domestic in origin. The war may have accelerated the tabling by compressing fiscal space through the revenue loss, but the spending items themselves were committed before the Middle East conflict began. The war determined when the supplementary arrived, not what it contained.

The 2026 budget, presented on 26 September 2025 under the IMF’s Extended Credit Facility and approved by parliament in December, targeted a fiscal deficit of 2.1 per cent of GDP and capped net new domestic borrowing at K21.6bn (2.3 per cent of GDP). The sixth and final ECF review was completed on 27 January 2026. The IMF praised reform progress at programme close. The post-programme question was whether fiscal discipline would survive once the external anchor no longer bound the calendar. The supplementary, tabled three months later, provides the answer.

The budget was made under the anchor. The supplementary was made without it. The timeline is three months.

Parliament referred the estimates to the Expanded Planning and Budgeting Committee, which expressed support but cautioned against “continued heavy reliance on borrowing and expenditure realignments.” The House approved the estimates on 11 May. The committee report has not been published. The primary estimates document has not been released for independent verification.

The FRA Drag on Primary Balance

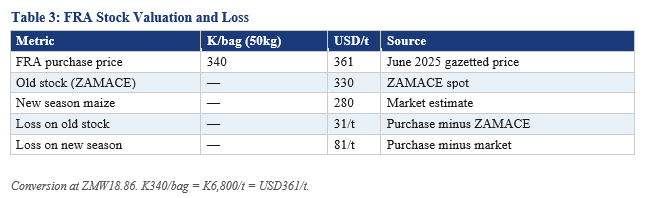

In September 2025, the President directed FRA to purchase all available maize. The planned purchase was 543,000 MT. FRA purchased 1,667,921 MT, valued at K11.3bn against an approved budget of K2.4bn. Treasury funded K3bn directly. A K5bn commercial loan covered the next tranche. The residual unfunded arrear stood at approximately K3.3bn. FRA’s secure storage capacity is approximately 1.5m MT. It purchased 1.7m MT. The excess sits in open-air storage.

The supplementary confirms the consequence. K7.4bn to Agriculture is the largest single allocation, covering FRA replenishment and FISP arrears. The Expanded Planning and Budgeting Committee expressed concern over “continued accumulation of arrears owed to agro-dealers and financing challenges facing the FRA despite increased allocations.”

The K5bn loan converted a social commitment into interest-bearing sovereign debt. New purchases from a record 2025/26 harvest (exceeding 3.87m tonnes) will compound the position. FRA has announced it will purchase a minimum of 500,000 MT for the 2026/27 season from May to October 2026. The 2026/27 purchase price has not been gazetted. Even at the 2025/26 price of K340/bag, the cost of buying only the gap to the 2.5m MT strategic reserve target is K5.4bn against a K2.1bn allocation. In an election year, the political incentive to buy more is identical to the pressure that produced the September 2025 directive.

FRA cannot offload current stock without loss.

The government has never run a fiscal exposure of this magnitude through FRA. The combined pressure of K5bn loan servicing, the K3.3bn unfunded arrear, and new purchases above the K2.1bn allocation represents a drag on the primary balance measured in the low billions annually.

The conditional escape depends on climate. If El Nino materialises alongside sustained disruption to global fertiliser and agrochemical supply, FRA’s stock shifts from liability to strategic asset (Tindale, 2026). China’s restriction on sulphuric acid exports from May 2026 appears politically durable (Duesterberg and Aibel, Hudson Institute). Without these conditions, the stock deteriorates or is sold below cost.

FRA does not publish audited financial statements. These numbers are reconstructed from ministerial statements, parliamentary records, and budget documents.

What These Numbers Measure

Fiscal Balance = Revenue and Grants − Expenditure (excluding amortisation)

When the answer is negative, the government must finance the gap.

Primary Balance = Revenue and Grants − Expenditure (excluding amortisation and interest payments)

The primary balance reveals whether the government can cover current operations from current revenue before the cost of past debt. The IMF tracked this number as its core measure of fiscal sustainability throughout the programme. A primary deficit means the government cannot fund even its operational spending from revenue.

The Secretary to the Treasury presented Q1 fiscal data to stakeholders in April. Revenue, expenditure, and financing appeared as three resource categories. He did not subtract one from the other. Neither the fiscal balance nor the primary balance appeared. The single most important number in the presentation was absent.

Fiscal Performance Through Q1

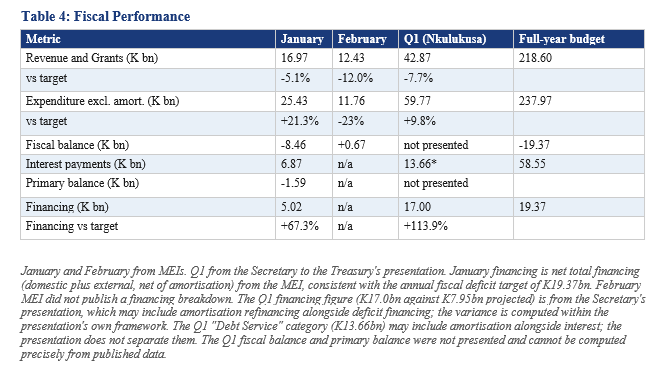

The fiscal deficit consumed 40 per cent of the annual target in two months. Q1 financing of K17bn implies approximately 88 per cent was consumed in one quarter. Both figures predate the war or were materially determined before it could explain them.

January ran a fiscal deficit of K8.5bn, consuming more than a quarter of the full-year allowance in a single month. Expenditure reached 21 per cent above target. FRA funding overshot its monthly target by 404 per cent. FISP disbursements ran 39 per cent above plan. The primary balance swung from a targeted surplus of approximately K3.9bn to a deficit of K1.6bn, a K5.5bn miss.

February reversed the expenditure pattern. Spending pulled back 23 per cent below target. Revenue deteriorated. VAT collected 42 per cent below plan. Domestic VAT reached K198m against a target of K897m, 78 per cent below. Grants came in at K30m against a full-year budget of K12.1bn. The full expenditure breakdown for February was not published.

Through two months, the cumulative fiscal deficit stood at K7.8bn against a full-year budget of K19.4bn. That is 40 per cent of the annual target consumed in 17 per cent of the year. January fully precedes the war. February’s fiscal outturn was materially determined before the 28 February shock could explain it.

The Q1 aggregates confirmed the trajectory. Tax revenue ran 4.8 per cent below target. Grants fell 67 per cent short (Secretary to the Treasury’s Q1 presentation). Transfers, where FRA and FISP sit, reached K15.0bn against K7.3bn projected, 104 per cent above. Total financing reached K17.0bn against K7.9bn planned. The government borrowed more than double what it had projected. The ZRA Commissioner separately confirmed that Q1 revenues fell short by K1.7bn. The Secretary to the Treasury’s own presentation identifies two Hormuz transmission channels for Zambia: fuel import dependency and imported fertiliser inputs.

The Q1 financing figure independently confirms the scale of the deficit. In standard fiscal accounting, the deficit approximately equals the financing requirement. Q1 financing of K17.0bn against a full-year target of K19.4bn implies that approximately 88 per cent of the annual deficit was consumed in one quarter. The Secretary to the Treasury’s expenditure figure (K59.77bn) may differ from the MEI definition, and the presentation did not separate interest from amortisation, so the fiscal balance cannot be computed precisely from Q1 data alone. But the financing line is unambiguous. The government financed K17bn in one quarter against a plan of K7.9bn.

Moody’s Ratings projected in April that the deficit could reach 4 per cent of GDP, nearly double the 2.1 per cent target. The Finance Minister said “that may be slightly on the high side.” The supplementary budget, tabled the same week, suggests otherwise.

The revenue base itself may be weaker than the budget assumed. Preliminary estimates show the economy grew 3.8 per cent in 2025, unchanged from 2024 and below the trajectory the 2026 budget was built on. Copper production fell 12.5 per cent from January to 63,253 tonnes in February (Ministry of Mines). The ZamStats trade data measures a separate metric, exports rather than mine output, and shows a parallel decline: refined copper export volumes fell 11.2 per cent from 77,200 tonnes in February to 68,600 tonnes in March, with export earnings down 10.5 per cent from K19.4bn to K17.3bn as LME copper prices dropped 3.6 per cent to USD12,499 per tonne. Export volumes exceed production because Zambian smelters process DRC copper concentrate alongside domestic ore. Cumulative Q1 2026 export volumes remain 6 per cent above Q1 2025, but the monthly direction is downward. Mineral royalties, which are levied on Zambian mine output, held above their February target on price strength, but declining production at any price level compresses the royalty base.

The Grants Hole

The grants line is close to zero. Through Q1, grants reached K789m against K2.4bn projected (Secretary to the Treasury’s Q1 presentation). Against the full-year budget of K12.1bn, the run-rate is concerning.

Part of this connects to the stalling of Zambia’s health aid arrangement with the United States. PEPFAR provided approximately USD367m annually, roughly 60 per cent of total US development support and funding over 60 per cent of the national HIV programme. The US shifted to bilateral memoranda of understanding requiring data-sharing provisions and, in some cases, minerals access. By December 2025, fourteen African countries had signed: Kenya, Rwanda, Uganda, Nigeria, Mozambique, Ethiopia, Botswana, and seven others. Several agreements have been challenged in court. Zambia has not signed. Zimbabwe rejected the terms on data sovereignty grounds. Ghana rejected similar terms. South Africa’s bilateral relationship collapsed over separate tensions. Tanzania and the DRC have not signed. The Foreign Minister called the proposed terms “unconscionable.” The deadline passed without resolution.

The 2026 health budget is K26.2bn. The budget speech acknowledged the risk of losing external health support: the K6.4bn allocation for drugs and medical supplies "represents an increase of 30.0 percent from 2025" and was explicitly intended "to cover the gap following the withdraw of some external support" (paragraph 168). Whether other health budget lines were also adjusted in anticipation is not disclosed. The budget projected K12.1bn in total grants from cooperating partners. Whether that figure assumed continuity of PEPFAR funding is also not disclosed. PEPFAR at approximately K6.9bn annually (USD367m at the current rate of ZMW18.86) represents more than half the grants target. A joint ZIPAR and United Nations analysis of the 2026 budget identified a K21bn financing gap to meet international health commitments (2 October 2025). Through Q1, grants reached K789m against K2.4bn projected. The gap between the budget's assumptions and the grants outturn is widening regardless of which assumptions the budget made.

This is one side of the structural constraint we mapped in “The Forced Choice” (February 2026). The United States conditions health aid on minerals access. China, Zambia’s largest bilateral creditor at over USD4bn, conditions engagement on political alignment. The RightsCon cancellation in May illustrated the other side. The IMF programme, which imposed conditions but also provided resources and diplomatic cover, is no longer in place. The grants line collapsing is the fiscal expression of a closing external support architecture. We covered the political economy of this constraint in “The Forced Choice” at canarycompass.com.

With the fiscal hole widening and external grants stalling, the burden of funding the state falls entirely on the domestic securities market.

Financing Performance Through April

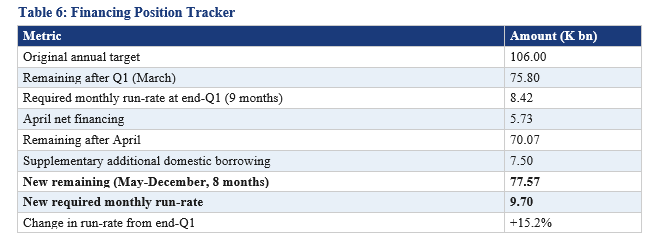

The domestic borrowing programme originally targeted K106bn in gross securities issuance for 2026, including the refinancing of maturing debt. Of that total, K21.6bn represented net new domestic financing. The supplementary adds K7.5bn in additional net domestic financing, raising the net domestic borrowing requirement to K29.1bn and the effective gross issuance target to approximately K113.5bn.

The bond auction tells the story. In January, bids reached K10.1bn against K4.2bn offered. In February, K21.3bn. Offshore capital took 49 and 69 per cent of allocations. By April, bids fell to K2.7bn against K6.3bn. The 7-year drew K281m against K1.6bn. Rejected bids at the long end carried yields up to 100 per cent. Bond demand fell 87 per cent from the February peak.

T-bills are operating inside a corridor trap. Three of four tenors offer insufficient compensation relative to the overnight interbank deposit floor. The 30 April auction showed the pressure: the 182-day was rejected at 15.3 per cent (accepted at 11.5), and the 364-day at 14.0 (accepted up to 12.7). Investors demanded higher yields. The government, through its agent, the Bank of Zambia, rejected them.

April did not reduce the burden. The supplementary added more than April delivered. The required monthly run-rate has risen from K8.42bn to K9.70bn despite a month of issuance having passed. May has no bond auction. Even if the T-bill auctions in May and June each deliver K2.2bn in net financing (requiring subscription above 100 per cent because T-bills maturing within the year offset gross issuance), the remaining balance entering the June bond auction rises further. The monthly run-rate climbs above K10.7bn. The June bond auction, offered at K6.3bn, would need to deliver approximately K10.6bn in net issuance to break even on a single month's requirement.

Unless June produces a significant financing month, issuance sizes in the second half will need to increase. The current structure of K6.3bn per bond auction and K2.2bn fortnightly in T-bills cannot reasonably be expected to sustain the required monthly run-rate. Unless there is a significant change in the global environment, Zambia may have to let yields rise to attract the participation the programme requires.

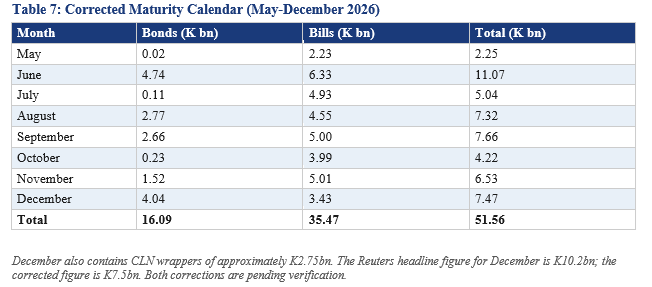

June: The Corrected Maturity Wall

Our earlier estimate of K8.3bn in June bond maturities, sourced from Reuters, included credit-linked note wrappers. A credit-linked note gives offshore investors exposure to the same domestic bond through an international clearing structure; it is not additional debt. These CLNs carry XS ISINs and are classified as Eurobonds in the Reuters database, but they are derivative representations of domestic ZM-ISIN bonds structured for international clearing through Euroclear. The Reuters data flags them with a “DR” (duplicated) marker. The outstanding amounts on the domestic and international ISINs are identical. Stripping these wrappers corrects the maturity profile.

June carries the largest maturity concentration in the remaining calendar. Bond maturities of K4.7bn and bill maturities of K6.3bn will provide recycled liquidity, but the amount is smaller than the K14.6bn headline we cited. Whether investors roll at maturity or exit depends on global risk appetite, yield compensation, and confidence in the fiscal trajectory.

A weak June auction would not only widen the immediate financing gap but compromise Q3 and Q4 even if conditions subsequently improve, because the catch-up burden compounds forward. If neither robust bidding interest nor rollovers materialise through June, the required yield concession to clear the market widens.

Some regional data suggests the April deterioration was systemic. South Africa saw record bond outflows in March. Kenya’s switch auction collapsed at 87 per cent in April, with the CBK Governor attributing it directly to geopolitical uncertainty. The CBK ran three switch auctions in 2026. The January and March switches oversubscribed. By the third, on 13 April, six weeks into the war, demand collapsed to KSh2.56bn against a KSh20bn target.

But the systemic explanation has an expiry date. Even if the global environment normalises, concerns are shifting onto domestic fiscal performance. Moody’s projection of a 4 per cent deficit did not require the war. It required only the domestic fiscal performance that the MEIs have confirmed. The war amplified what the structure was already producing. Offshore demand may have been front-loaded into January and February. The maturity calendar between March and April offered limited recycled cash (no bond auction is scheduled for May, which also carries limited maturities). Those factors would have thinned demand regardless. If the global environment stabilises and offshore still does not return at scale, the fiscal trajectory becomes the larger explanation.

BoZ committed to introducing Liability Management Operations in Q2. No modalities have been published as of mid-May. May, which carries no bond auction, could be the window. Kenya’s experience suggests the current environment is not favourable for switch operations.

The Offshore Dependency

That positioning was earned. The copper story, the reform trajectory, and the debt restructuring completion attracted capital into a carry trade at yields of 16-17 per cent with a strengthening kwacha. Offshore liked the administration. Investors who had met the President were encouraged by his ambitions for the country. The macro direction was credible.

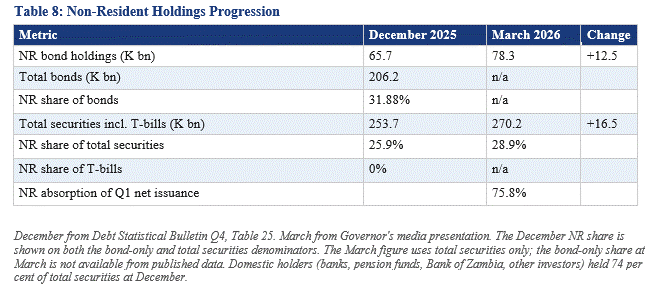

In three months, non-residents absorbed K12.5bn of the K16.5bn in net new securities issued. The domestic market contributed K4.0bn. The Bank of Zambia had raised the non-resident participation cap from 5 per cent to 23 per cent in January. Q1 2026 was the most offshore-dependent quarter of domestic financing in Zambia’s post-restructuring history.

The total 2026 cash flow obligation to non-residents on the existing portfolio at end-December stood at K24.6bn (Debt Statistical Bulletin Q4, Table 27): face value maturities of K10.5bn, discount payments of K4.5bn, and coupon payments of K9.6bn. Net additions in Q1 (K12.5bn in face value) do not retire the annual obligation. Total cash owed to non-residents on the portfolio exceeds what any single quarter's inflow contributed. When the April bond auction collapsed, servicing this obligation became a financing question yet again.

The kwacha’s Q1 appreciation rested on mining sector FX supply of USD915.7m, up from USD759.4m in Q4 2025. Net sales by mining companies reached USD626.0m. Gross international reserves reached a historic high of USD6.5bn in February before closing Q1 at USD6.2bn. The March decline included USD114.7m in government payments for fuel procurement. Outstanding foreign exchange demand orders built to USD33.1m at end-March from zero at end-December. At USD6.2bn, reserves provide a substantial buffer against near-term currency pressure. The kwacha risk is not immediate. It is conditional: if copper volumes continue to decline and fuel imports continue to draw on reserves, the FX supply arithmetic shifts over quarters, not weeks.

The January and February bond auctions proved the confidence was real. Bids of K10.1bn and K21.3bn, with offshore taking 49 and 69 per cent of allocations, showed that investors priced the reform trajectory, the debt restructuring completion, and the IMF-anchored fiscal path. That confidence carried Zambia through the immediate post-programme period. The question still remains whether it survives without the programme. An IMF anchor does not prevent fiscal shocks. It provides the institutional framework through which shocks are absorbed without breaking market confidence. When a country with an active programme faces an oil shock, investors expect the programme conditions to constrain the fiscal response. When the programme has ended and the supplementary arrives three months later, investors must assess fiscal discipline on the government's own record. The April auction was the first assessment. June will be the second.

Even in the best case where the global environment normalises and offshore sentiment recovers, the Zambia they return to is not the Zambia they bought into in February. They priced a 2.1 per cent deficit under an IMF anchor with domestic borrowing capped at K21.6bn. They now face a widening deficit, domestic borrowing at K29.1bn, a grants architecture that has not recovered, an FRA exposure measured in billions, and no programme. The same yield that was attractive in February may not compensate for the deteriorated fiscal position. Offshore may return, but at a higher yield threshold. The government may get the participation it needs, but only by conceding on price. A stable currency makes this possible. It removes FX risk and preserves the carry on exit. But it requires the yield leg to adjust upward. If the election resolves without disruption and yields adjust into a stable currency, offshore participation could recover in Q3. If the conflict de-escalates, oil falls, and June clears strongly, Zambia gets a window. The structural items (FRA, wages, arrears) would persist, but the systemic alibi would expire faster, shifting the test from shock management to domestic fiscal credibility.

At K113.5bn in effective annual issuance, the market depends structurally on offshore participation. Non-residents held 28.9 per cent of total securities and absorbed 75.8 per cent of Q1 net issuance. That participation is not marginal. It is the financing. Each incremental percentage point is harder to attract. If offshore saturates, two paths remain: fiscal consolidation reduces the borrowing requirement, or the domestic market steps up. Several 2025 bills aimed at improving credit access would redirect bank balance sheets toward private-sector lending. That is good policy in normal times. In a year when the government needs domestic banks to strongly absorb a portion of K113.5bn in securities issuance, those bills create tension. The domestic bid for government paper could thin at the same time the borrowing requirement has not shrunk.

The Finance Minister told Bloomberg in April that the local bond market “has been very useful” and that there is “scope for more” yield reduction, “not based on force, but based on what investors can see and judge.” The April auction subscribed at 43 per cent.

Election-year fiscal loosening is standard frontier-market behaviour. The issue is whether this loosening was priced in. The budget signalled discipline. The supplementary reversed it. Offshore will extend latitude in an election year. A deficit consuming nearly half the annual allowance in two months, before the war, is not latitude. If the systemic environment normalises and the fiscal data does not improve, the country-specific explanation takes over.

It is against this backdrop of fiscal expansion and evaporating market demand that the central bank’s rate decision must be measured.

The Monetary Policy Decision

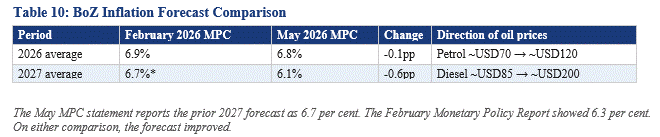

The Committee cited a favourable inflation outlook, the expected maize harvest, exchange rate stability, and upside risks from the Middle East conflict. Inflation declined from 11.2 per cent in December 2025 to 6.8 per cent in April, inside the 6-8 per cent target band. The forecast projects it remains within the band through 2028, averaging 6.8 per cent in 2026 and moderating to 6.1 per cent in 2027. The drivers cited are exchange rate appreciation and anticipated lower maize prices.

Zambia’s inflation outturn is unusually benign relative to the scale of the fuel shock. The reason is not monetary policy. It is a fiscal subsidy. The MPC statement itself acknowledges this: fuel prices “could, actually, have been higher than they currently are had it not been for the tax relief that the Government has provided, notably the suspension of excise duty and zero-rating of value added tax on petroleum products for three months.” The Committee identified the mechanism, noted that it suppresses measured inflation, and cut anyway. Inflation protected by revenue foregone is not inflation conquered by structural adjustment. The maize harvest mechanically suppresses food prices, the largest weight in the basket, but the FRA is buying the surplus at K340/bag, converting the CPI benefit into a fiscal liability measured in billions.

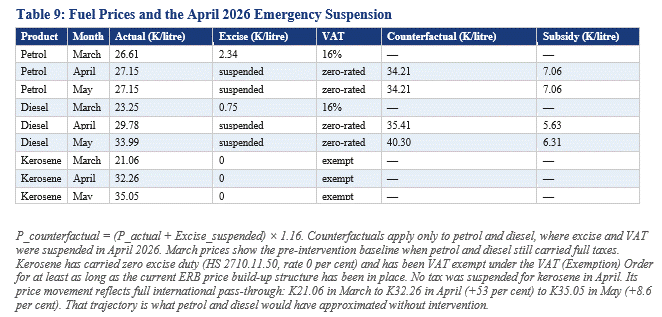

The ERB price build-up makes the subsidy measurable. The counterfactual pump price follows a simple formula:

P_counterfactual = (P_actual + Excise_suspended) × (1 + VAT_rate)

The table shows three stories. Petrol carried excise of K2.34 per litre and VAT at 16 per cent through March. In April, both were suspended. Without the suspension, petrol would cost K34.21. It costs K27.15. The government is absorbing K7.06 per litre. Diesel carried excise of K0.75 and VAT at 16 per cent. Without the suspension, May diesel would cost K40.30. It costs K33.99. The subsidy is K6.31 per litre, up from K5.63 in April as international diesel prices rose 23 per cent in a single ERB review cycle. Kerosene, which has never carried excise or VAT within the current pricing structure, shows what full pass-through looks like: K21.06 in March, K32.26 in April, K35.05 in May. The government is purchasing the 6.8 per cent inflation reading at K6.31 per litre of diesel and K7.06 per litre of petrol.

The April CPI, published by ZamStats the week before the MPC meeting, already showed the strain. Monthly non-food inflation (month-on-month) jumped from 0.4 per cent in March to 1.3 per cent in April. The driver was fuel: diesel at the pump had risen 28 per cent between the March and April ERB reviews (K23.25 to K29.78), even with the suspension in place. Transport inflation (year-on-year) swung from minus 0.3 per cent in March to plus 1.3 per cent in April. The May ERB review adds another 14 per cent to diesel. The pipeline feeding into the May and June CPI readings is rising, not stable.

What the statement did not address is more revealing than what it did. The word “fiscal” does not appear. There is no mention of the supplementary budget tabled twelve days before the meeting. No mention of domestic borrowing rising 35 per cent. No mention of the April bond auction subscribing at 43 per cent. No mention of grants at 67 per cent below target. The entire fiscal and financing convergence documented in this note is absent from the central bank’s assessment.

The forecast improved while international fuel prices roughly doubled. The BoZ cites exchange rate appreciation and lower maize prices as the drivers. Both are real. The forecast improvement depends heavily on the assumption that food and exchange rate disinflation outweigh fuel price pass-through. If the tax suspension expires and oil prices remain elevated, that assumption faces its hardest test in the final quarter. The statement does not disclose how much of the improved path depends on the temporary fiscal tax relief it acknowledges elsewhere.

The three-month suspension window expires on 30 June. It is unlikely to. No government removes a fuel subsidy two months before a general election, although a partial restoration remains possible if oil prices fall. The suspension will run through August at minimum, and likely through September or beyond. The September MPC will therefore assess inflation produced entirely under fiscal suppression. The Committee will have no unsuppressed data to evaluate. If the suspension expires at end September, full pass-through hits the October pump price. October is the last month of the lower seasonal inflation cycle (May to October: harvest effects, lower food prices month-on-month). November begins the planting season, when food inflation rises structurally. The fuel shock and the seasonal turn would compound in the same quarter. The Committee meets 28-29 September with subsidised data, holds or adjusts the rate, and then faces the compounding shock without a scheduled decision point. The 25 basis point cut was not cautious. It was a forecast built on the assumption that someone else keeps writing the cheque.

The BoZ’s mandate is price stability, not fiscal financing. The Committee would argue inflation is within target and real rates remain positive. But the inflation reading the mandate is being measured against depends on a fiscal subsidy the central bank does not control. The statement identifies the subsidy but does not model what happens when it expires.

The May decision collided with the fiscal and financing pressures documented above. The stable exchange rate, at ZMW18.86, should be the foundation for attracting offshore participation back into the bond market. A stable currency removes FX risk and preserves the carry on exit. But the return requires both legs: currency and yield. The MPC moved the yield leg in the wrong direction.

The 30 April T-bill auction showed bidders demanding 15.3 per cent on the 182-day and 14.0 per cent on the 364-day. The Bank of Zambia rejected those bids. At 13.25 per cent, the policy rate pushes the overnight floor lower, attempting to close the corridor trap from above. The auction data suggests the market wants to move in the other direction. Bonds are a different market where yields are set by auction clearing rates, fiscal trajectory, and global risk appetite. But the signal matters. A central bank that eases while the fiscal position is deteriorating tells the bond market that it trusts its own inflation forecast more than the fiscal data warrants. If that forecast depends on a temporary subsidy, the market prices accordingly. In an environment where the government needs K9.70bn per month from the domestic market, the disconnect between the policy rate and the market's required yield carries a cost.

The next MPC meeting is 28-29 September. The Committee has locked itself into 13.25 per cent through the June bond auction, the fiscal data for March through June, the supplementary implementation, and the August general election. The most consequential fiscal and financing period of the year will unfold without a scheduled rate decision.

Close

Seven stars needed to align. That was the assessment in January, when the refinancing wall was mapped and the buffers were thin. The arithmetic left no margin for shocks on either the fiscal or the financing side simultaneously.

The fiscal deficit reached 40 per cent of the annual target in two months. Q1 financing of K17bn implies approximately 88 per cent was consumed in one quarter. The FRA liability of K11.3bn followed a September 2025 directive. The wage increment was negotiated before the war. The constituencies were created by constitutional amendment. All of this preceded the Middle East conflict. Of K16.3bn in net new supplementary expenditure, no major allocation is directly identifiable as war expenditure. The war’s direct fiscal cost appears on the revenue side through foregone fuel taxes. Its indirect cost appears through financing pressure and reserve drawdowns. When the suspension is extended through the August election, as it almost certainly will be, that revenue loss roughly doubles.

The government now plans to raise the supplementary addition from a securities market that subscribed at 43 per cent six days before the supplementary was tabled. The required monthly run-rate has risen to K9.70bn, 15.2 per cent higher than at end-Q1, despite a month of issuance having passed. The Secretary to the Treasury presented Q1 data without computing the fiscal balance. The grants line sits well below plan while the PEPFAR arrangement remains unresolved. The budget speech acknowledged the withdrawal of external health support nine months ago. The FRA carries billions in exposure outside headline fiscal reporting.

The Secretary to the Treasury’s own conclusion in April was that “Zambia has reached a decisive moment where recent stabilisation gains must be carefully preserved and strengthened.” The Q1 data he presented in the same briefing, and the supplementary budget tabled the same week, suggest those gains are not being preserved. They are being spent.

The data in this note was available to every analyst covering Zambia. The MEIs are published. The auction results are published. The budget speech is published. The supplementary statement is published. The local analytical ecosystem did not produce the stress-test before the supplementary arrived.

Zambia’s fiscal challenges are compounded by an analytical environment where commentary calibrated to access rather than accuracy disables the early warning function that independent analysis is supposed to perform. Each of these spending decisions looked costless in isolation. The maize purchase was a political win for farmers. The wage increment was a win for civil servants. The constituencies were democratic expansion. But they accumulate. They compound. They sit on the balance sheet as arrears and commercial loans until a supplementary arrives to regularise them. When the accumulated cost crystallises, it transmits to the taxpayer through debt monetisation that puts a floor under inflation. Or it transmits through fiscal adjustment that cuts the services the spending was supposed to fund. This is not a new cycle. It is the cycle that required IMF intervention in the first place.

The fiscal position is slipping while financing is tightening. Yields may have to move higher to compensate. That big February statement may yet turn into a concession.

For the full analytical framework, see The 2026 Refinancing Wall, Domestic Market Absorption, Copper Output and the 2026 Royalty Arithmetic, Growth Without Diffusion, A Little Here a Little There (fuel subsidy counterfactual methodology), The Acid Test, The Forecast Is Not the Evidence, and The Forced Choice at canarycompass.com.

Sources: Bank of Zambia MPC Statement (13 May 2026, meeting 11-12 May), Governor’s Media Presentation (13 May 2026), Monetary Policy Report (February 2026), and auction results (January, February, April 2026). Ministry of Finance Monthly Economic Indicators (January, February 2026). Ministry of Finance Quarterly Debt Statistical Bulletin (Q3 2025, Q4 2025). Secretary to the Treasury Q1 presentation (April 2026). Musokotwane ministerial statement to Parliament (20 February 2026). Supplementary Estimates No. 1 of 2026 (ministerial statement, 30 April 2026; approved 11 May 2026). 2026 Budget Speech (26 September 2025). ZRA Q1 revenue confirmation. ZamStats, The Monthly, Volume 277 (April 2026). Energy Regulation Board, Review of Petroleum Pump Prices (April and May 2026). Reuters maturity profile (corrected for CLN wrappers). Finance Minister Situmbeko Musokotwane (Bloomberg, April 2026; Parliament, 30 April 2026). Foreign Minister Mulambo Haimbe (May 2026). Moody’s Ratings (April 2026). Civil Society for Poverty Reduction. Expanded Planning and Budgeting Committee. Agriculture Minister Reuben Mtolo (January 2026). Tindale (2026). Duesterberg and Aibel, Hudson Institute (2026). CBK Governor Kamau Thugge (Business Daily, April 2026). UNDP/ZIPAR health financing analysis. Canary Compass, “A Little Here, a Little There” (1 April 2026).

Disclaimer

This article does not constitute legal, financial, or investment advice. The author shares views for perspective and discussion only. Do not rely on them as a substitute for professional advice tailored to your specific circumstances. Always consult a qualified legal, financial, investment, or other professional adviser before making decisions based on this content. The analysis reflects proprietary research undertaken by Canary Compass and the author.

Canary Compass and the author accept no liability for actions taken or not taken based on the information in this article.

The views expressed in this article represent the author’s independent professional analysis and do not constitute an endorsement of any individual, institution, or position. Canary Compass and the author accept no responsibility for how this content is interpreted, excerpted, or recontextualised by third parties not involved in its production and publication. Reproducing any portion of this work in isolation, or in combination with other material, in a manner that misrepresents the author’s original meaning constitutes a distortion of the published record.

The author may hold positions in financial instruments, currencies, or assets discussed or referenced in this publication. Such positions do not constitute a recommendation to buy or sell.

All views, projections, and forecasts reflect the author’s assessment at the time of writing. Data sourced from third parties is believed to be reliable but has not been independently verified. Past performance does not indicate future results.

All content published by Canary Compass is the intellectual property of the author. Reproduction, adaptation, or redistribution, in whole or in part, requires written permission.

About the Author

Dean N. Onyambu is the Founder and Chief Editor of Canary Compass, a financial research publication focused on African monetary architecture and financial sovereignty. He brings 18 years of experience across trading, fund leadership, and economic policy, with senior roles at Standard Bank, First Capital Bank, and Opportunik Global Fund.

Read and subscribe at www.canarycompass.com.

The Canary Compass Channel is available on @CanaryCompassWhatsApp for economic and financial market updates on the go.

For more insights from Dean, you can follow him on LinkedIn @DeanNOnyambu or X @InfinitelyDean.