Zambia Monetary Policy: Structure Before Sentiment. Part 1: Decision Week

Why the Bank of Zambia must hold at 14.5% on Wednesday

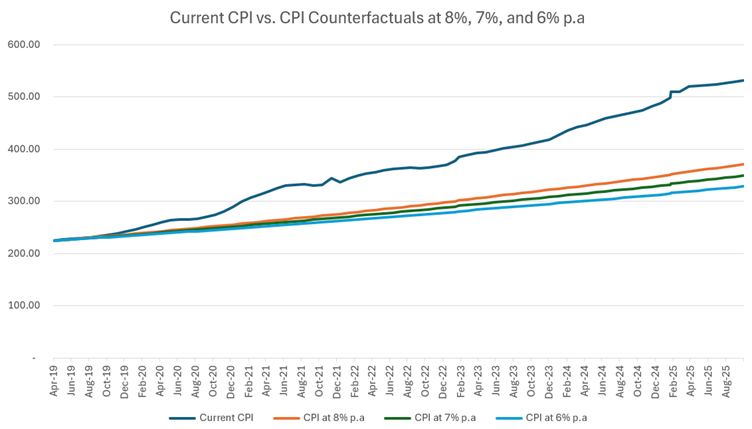

Source: Bank of Zambia, Own estimates

Editor’s Note: November 12, 2025

This correction follows a detailed technical engagement with the Bank of Zambia regarding the classification of financial account flows. The purpose of this note is to ensure that all published work reflects the most accurate interpretation of the data and maintains the highest standards of analytical integrity. The underlying aggregates of the balance of payments remain unchanged. The revisions relate solely to the internal composition of the financial account.

Scope of the Correction

The headline balances for the current account, capital account, overall financial account, net errors and omissions, overall balance, and reserve movements remain unchanged from their previously published values. The corrected figures affect only the internal distribution within the financial account between direct investment, portfolio investment, other investments, and financial derivatives.

Corrected Figures Referenced

Direct Investment (FDI):

+$685.3 million in the first half of 2025 and a cumulative +$3.51 billion across sixteen quarters (Q3 2021 to Q2 2025).

These flows include new equity, expansions of existing projects, retained earnings, and intracompany loans. The data confirm that some headline investment announcements translated into real inflows, placing Zambia’s direct investment climate in positive territory across the sample period. However, much of this capital entered through capital goods imports, contractor payments, and reinvested earnings, which do not create immediate foreign exchange liquidity in the interbank market.

Portfolio Investment:

−$17.1 million in the first half of 2025 and a cumulative −$436.0 million over the sixteen quarters.

Portfolio flows have therefore remained net negative throughout the review period, reflecting weak foreign participation in domestic securities and the ongoing impact of the 5 per cent cap on non-resident holdings of government securities.

Other Investment:

−$788.4 million in the first half of 2025 and a cumulative −$6.41 billion over the sixteen quarters.

Of this, −$3.75 billion reflects offshore asset accumulation by non-financial corporations, households, and non-profit institutions serving households—essentially, profit retention, offshore savings, and working capital balances held abroad.

A further −$1.87 billion reflects private-sector external debt servicing under other investment liabilities, consisting of principal and interest repayments by corporates. These transactions constitute cash outflows that directly reduce foreign exchange availability within the domestic system.

Financial Derivatives:

−$7.8 million in the first half of 2025 and −$36.1 million cumulatively. These remain negligible and carry no material effect on the overall interpretation.

Impact of the Correction

The correction does not alter the substantive conclusions from earlier analyses. The kwacha’s appreciation remains unsupported by broad-based, market-supplied foreign exchange inflows. The balance of payments continues to reflect structural external pressure. The inflation interpretation and the monetary policy recommendation remain unchanged. If anything, the corrected data strengthen these interpretations by providing a clearer understanding of the sources of foreign exchange leakage and the scale of persistent outflows.

Commitment to Transparency

Revisions of this nature are standard in macroeconomic analysis, particularly when working with complex balance of payments data. Publishing this correction reflects a deliberate commitment to transparency, professionalism, and accuracy. The note builds upon the engagement with the Bank of Zambia and confirms that analytical conclusions remain valid while improving the precision of flow classifications.

While the original article remains unchanged below, readers can access the corrected article through the link below. The corrected note supersedes the earlier interpretation of the financial account composition while preserving all substantive conclusions.

Link to Correction Article:

Zambia’s Financial Account: Corrected Composition, Unchanged Conclusions

0. Executive Intent

The November Monetary Policy Committee meets at a moment when surface relief masks deeper structural pressure. Inflation remains far above the 6% to 8% target range, and the Consumer Price Index level shows a decisive break from every credible disinflation path. The IMF’s August 2025 review reaches the same conclusion, projecting that inflation will only return to the target band in 2026 and that real incomes remain severely compressed.

The exchange rate confirms the imbalance. The recent appreciation of the kwacha did not reflect stronger fundamentals. Mining receipts were stable rather than significantly rising, portfolio flows remained thin, and the balance of payments stayed in deficit. Central bank intervention exceeded programmed levels early in the year, a signal that market supply never strengthened sufficiently to anchor the currency. Reserves improved on paper, but mainly through mechanical channels, such as statutory reserve accumulation and episodic disbursements, rather than through sustained net market purchases.

The October inflation report reinforces this fragility. Food and non-food inflation remain elevated on an annual basis, and monthly pressure from fuel and imports persists. Pass-through remains high because Zambia’s pricing structure is closely tied to foreign exchange movements, and structural bottlenecks prevent temporary currency strength from delivering lasting relief.

Under these conditions, a policy rate cut would increase the likelihood of renewed depreciation, widen the CPI level gap, and erode the credibility necessary to restore real purchasing power. The transmission mechanism also remains constrained. Liquidity asymmetries, sovereign exposure, and balance sheet structures limit the policy rate’s influence on lending conditions, meaning that an early cut would not necessarily translate into broader credit access.

The correct stance for November is to hold. Stability requires discipline until inflation shows real convergence, external balances strengthen through earned flows, and reserve buffers reflect genuine improvements in foreign exchange supply. This article sets out the evidence. Part One establishes the macro foundation. Part Two will assess the credit system and explain why the transmission mechanism cannot carry an easing signal at this stage.

1. Inflation Reality

1.1 CPI Level Divergence

Inflation may have eased on a monthly basis in October, but the overall price level remains far beyond the target range and continues to define the fundamental constraint on monetary policy. The Consumer Price Index stands at 530.91. If inflation had followed an 8% path since April 2019, the index would read 370.92. A 7% path would place it at 349.16. A 6% path would anchor it near 328.49. This gap represents a 30% to 38% loss in purchasing power over six years. No meaningful disinflation can occur without addressing this level of divergence.

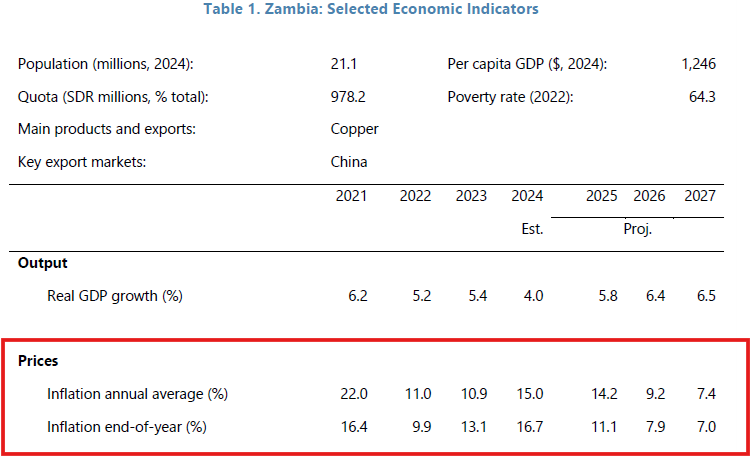

The IMF reaches a similar conclusion. Its August 2025 review projects year-end inflation at 11.1%, averaging 9.2% in 2026, and only returning to the 6% to 8% band at the end of 2026. The IMF also notes that real incomes have not recovered in line with prices, and that cost-of-living pressures remain severe, particularly for the most vulnerable households. These projections confirm that the current moderation in headline readings does not signal convergence.

Source: IMF

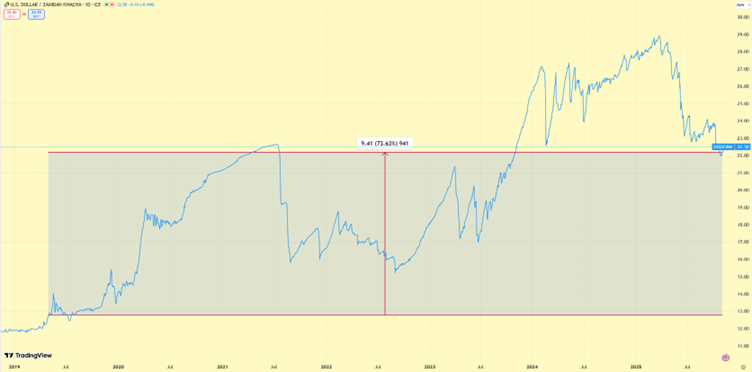

The exchange rate reinforces this assessment. The kwacha’s depreciation from 12.77 per dollar in April 2019 to approximately 22.18 in October 2025 implies a reduction in purchasing power of more than 40%. Zambia’s high pass through ensures that these movements affect food, fuel, transport, and essential inputs almost immediately. Households experience this directly. Even small shifts in the currency transmit into prices across their daily basket. Under these conditions, a temporary currency appreciation does not correct the accumulated price level. It only slows the rate of increase.

Source: TradingView

The CPI gap, therefore, remains the central macro anchor. Price stability requires a sustained period of discipline, supported by credible policy and an exchange rate aligned with genuine improvements in foreign exchange supply. Any easing before this adjustment takes place risks widening the price level gap further and delaying the return to target.

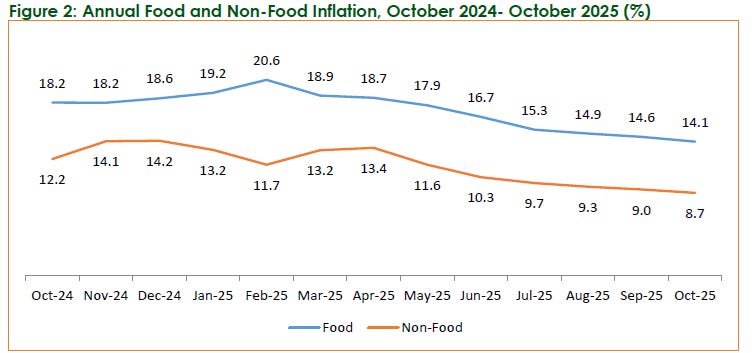

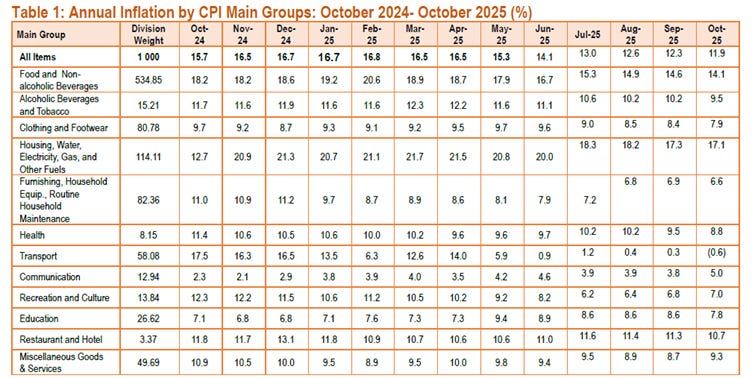

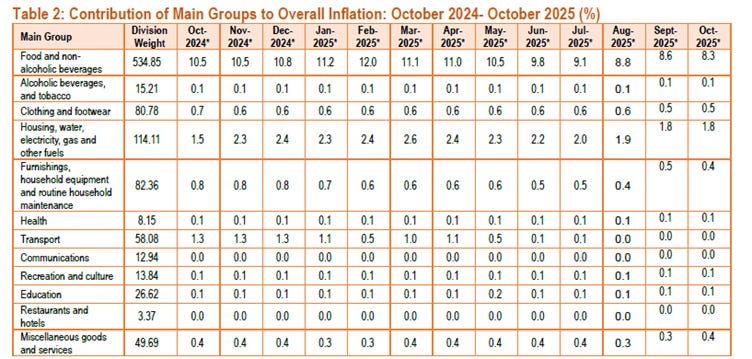

1.2 Inflation Composition

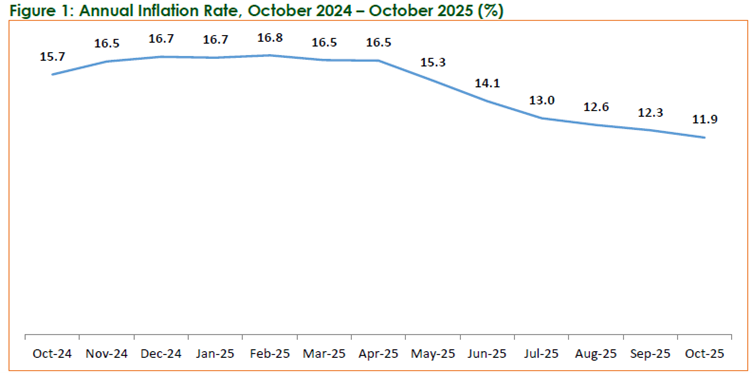

Source: ZamStats

Headline inflation slowed to 11.9% in October from 12.3% in September. Food inflation eased to 14.1%, and non-food inflation eased to 8.7%. These readings show softer momentum, yet they do not indicate relief in the underlying structure of prices.

Source: ZamStats

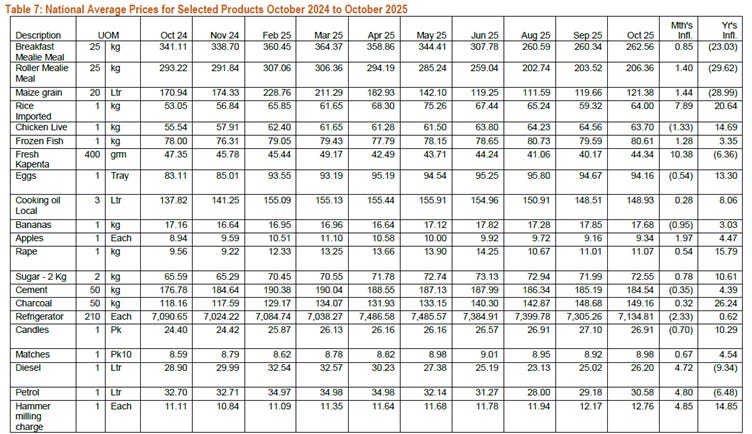

The annual data remains elevated. Both food and non-food categories reflect the cost shocks accumulated over recent years, driven by foreign exchange volatility, energy costs, logistics, and imported inputs. The October Monthly report confirms that essential food items, such as rice, vegetables (rape), live chicken, eggs, and processed products (sugar), remain significantly above last year’s levels. The sharp decline in maize-based products reflects the seasonal supply from the bumper harvest, rather than broad-based disinflation. Maize grain, breakfast meal, and roller meal prices are correcting from an earlier spike driven by drought. They are not signalling sustained easing across the wider food basket.

Source: ZamStats

Source: ZamStats

Non-food inflation shows similar persistence. Housing, water, electricity, gas, and other fuels rose by more than 17% year on year. Clothing and footwear, furnishings, household equipment and household maintenance, as well as miscellaneous goods and services, all recorded substantial annual increases, contributing significantly to non-food yearly inflation. These categories shape real household budgets and adjust quickly to changes in fuel and import-related costs. They adjust slowly to temporary currency strength. This slow adjustment reflects structural conditions rather than short-term sentiment.

Monthly movements confirm the lag between currency conditions and domestic prices. Food prices rose by 0.4% in October, and non-food prices rose by 0.5%. Imported rice increased by 7.89% and fuel prices rose sharply, with petrol up 4.8% and diesel up 4.72%. These items price off foreign exchange conditions with a delay, so their October levels still reflect the weaker exchange rate that prevailed through September and early October. Fresh Kapenta rose by 10.38%, driven by supply and cost dynamics rather than any direct foreign exchange exposure. November may record slower monthly momentum, but the risk backdrop has shifted. The kwacha has begun to weaken again, and the global environment suggests a firmer dollar in the short term following a technical intermediate bullish cross, as markets reassess U.S. interest rates and global risk. This combination limits the disinflation that a short October rally could have delivered.

Source: ZamStats

Source: ZamStats

The IMF, writing earlier in the year, highlighted sticky non-food inflation and high, immediate pass-through from foreign exchange movements into domestic prices. The latest data now shows food inflation as the dominant annual pressure point. In October, food inflation remained elevated on a year-on-year basis, while the monthly readings showed food prices rising by 0.4% and non-food prices by 0.5%. The economy is also entering the November to April planting season, a period when monthly food inflation typically exceeds the post-harvest pattern recorded from May to October. This seasonal tilt, combined with persistent import-linked costs and fuel adjustments, explains why temporary easing cannot deliver meaningful progress on the annual rate and why the return to the target band remains gradual.

For monetary policy, the implication is clear. The composition of inflation keeps pressure embedded in the price structure. A temporary easing in selected categories does not alter the underlying level. Durable convergence requires real supply improvements, stable foreign exchange conditions, and reduced exposure to imported costs. A premature rate cut would misread this balance and raise the probability of an inflation rebound in early 2026.

1.3 Household Balance Sheets

Household balance sheets continue to reflect severe real income compression. Nominal wages have increased in selected sectors, but these adjustments remain far below the cumulative rise in the price level since 2019. The CPI gap, the exchange rate path, and the structure of consumption all indicate a decline in real spending power.

The IMF notes that a significant portion of Zambia’s workforce remains concentrated in informal, low-productivity activities and that structural transformation has slowed in recent years. The informal sector carries the most significant exposure. Incomes in this segment adjust daily and track the prices of food, fuel, and public transport. Increases in these categories prompt immediate cuts in consumption and shifts toward more affordable substitutes. The October Monthly shows that households are spending more to secure fewer goods in many essential categories. This pattern indicates cash flow stress rather than improved welfare.

Source: IMF

Household budgets amplify this pressure. Food, transport, rent, school fees, and utilities dominate monthly spending. Households cannot compress these categories without compromising basic welfare. These items react quickly to foreign exchange movements and fuel costs, so households remain exposed even when headline inflation slows.

The private sector does not provide an offset. The purchasing managers index has hovered around the fifty threshold for years, reflecting an economy that alternates between marginal expansion and contraction. These conditions limit wage growth, employment gains, and the ability of firms to pass productivity improvements into household incomes.

Source: IMF

This environment shapes expectations. Households do not anchor their expectations to the headline rate. They anchor them to the daily prices of fuel, mealie meal, rent, transport, and school fees. Under these conditions, the credibility of monetary policy depends on visible progress in these categories. That progress has not yet materialised.

A rate cut would not ease household pressure. It would validate a price level that remains far above incomes, weaken the nominal anchor, and increase the risk of renewed pressure through the foreign exchange channel. The structural conditions that compress household balance sheets would remain unchanged.

2. Exchange Rate Reality and FX Market Structure

2.1 Kwacha Strength Is Not Flow-Driven

The recent appreciation of the kwacha created the impression of stronger external fundamentals. The flow data does not support that view. Mining receipts, the core source of foreign exchange supply, remained broadly stable rather than expanding significantly. Export earnings held steady but did not rise decisively enough to shift the balance of payments into surplus. The structure of supply, therefore, remained unchanged.

Portfolio investment confirms the same reality. Investors withdrew $46.6 million in the first quarter and returned $56.8 million in the second. The system therefore gained only $10.2 million in net portfolio investment during the first half of the year. These flows are too small and too volatile to drive sustained appreciation in a market where quarterly foreign exchange turnover reaches several billion dollars once mining taxes, corporate transactions, and bank balance sheet flows enter the system.

Market microstructure strengthens this conclusion. Every dollar sold by the central bank into the interbank market was absorbed immediately by real sector demand. Commercial banks did not accumulate foreign currency balances even as turnover increased. This recycling pattern indicates that the market did not experience a surplus at any point during the appreciation. It experienced temporary relief driven by positioning and sentiment, not by a structural increase in supply.

Positioning behaviour also changed. The average short dollar exposure in the interbank market increased from $11.9 million per day in the first quarter to $13.5 million in the second quarter and to $15.7 million in July. Participants increased short positioning even though actual inflows had not strengthened. This behaviour reflects confidence in the trend rather than confidence in fundamentals. It also increases the probability of reversal when conditions tighten.

The IMF’s August 2025 review supports this interpretation. It notes that fundamentals did not underpin recent currency strength and that Zambia’s foreign exchange market remains shallow. It highlights that the appreciation occurred despite limited improvements in export supply, weak capital flows, and intervention levels above programmed amounts in early 2025.

When price moves ahead of flow, the risk profile of the currency shifts. A policy rate cut at this stage would signal reduced defence at a moment when the system does not yet have the supply capacity to absorb renewed pressure. Stability, therefore, requires a firm stance until genuine improvements in external balances are visible.

2.2 Reserve Fragility

Headline reserves improved in the first half of the year, but the composition of that increase reveals significant fragility. The IMF makes this explicit. It notes that a significant portion of the reserve build was mechanical, driven by the rise in foreign currency deposits and the application of the statutory reserve ratio rather than by sustained net market purchases. These additions improve the headline but do not strengthen foreign exchange earning capacity.

Episodic disbursements also contributed. Multilateral support, project financing, and exceptional inflows temporarily raised the reserve level. These channels provide valuable buffers, but they bypass the core balance of payments mechanisms and create future repayment obligations. When export supply remains weak, such buffers delay pressure rather than reduce it.

Source: IMF

Intervention data reinforces this vulnerability. In the first quarter, as per the IMF, the central bank sold $233.5 million against a program allowance of $79 million. This deviation reflects the scale of pressure needed to stabilise the currency during a period with limited inflow strength. Intervention moderated in the second quarter as sentiment improved, but mining-related inflows also declined, partly due to the Zambia Revenue Authority’s expanded offsetting of foreign exchange-related tax liabilities. The IMF cautions that such offsetting reduces the amount of foreign exchange entering the market and undermines reserve accumulation.

Reserve adequacy assessments remain mixed. Headline reserves rose above $4.8 billion in July 2025, representing around 4.3 months of import cover, but usable reserves — those available for market support — remain well below the program’s net official international reserves (NIR) target for the end of 2025. The IMF stresses that Zambia’s external buffers remain thin relative to import needs, particularly given the significant negative net international investment position, sustained energy import requirements, and heightened financing risks over 2025 and 2026.

Under these conditions, an early rate cut would weaken the currency’s defensive posture and raise the probability of renewed pressure on reserves. Defending the exchange rate from a weaker reserve position is more costly and less effective. Intervention becomes larger, more prolonged, and more destabilising for liquidity conditions. A disciplined stance is therefore essential until reserve buffers reflect genuine, earned improvements.

2.3 High Pass Through

Pass-through remains one of the dominant channels of inflation pressure in Zambia. The October Monthly report shows that both food and non-food categories remain highly sensitive to foreign exchange movements, fuel costs, and import-related pricing. The IMF describes this pass-through as high and immediate, and identifies it as a core structural constraint.

Food inflation eased on a monthly basis in October due to seasonal supply effects, particularly in maize-based products. However, the annual data remains elevated across several categories that depend on imported inputs and logistics. Cereal grain products, cooking oil, processed foods, and selected proteins all reflect the accumulated effect of exchange rate movements and energy costs from earlier in the year. Seasonal relief cannot quickly unwind these cost bases.

Non-food inflation shows even greater rigidity. Housing, water, electricity, gas, and other fuels remain significantly above last year’s levels. Education, health, household equipment, and routine maintenance all reflect persistent pressure. Fuel price adjustments in October moved directly into transport costs, and transport costs then increased logistics and distribution expenses. These channels operate continuously and remain unchanged when the currency strengthens temporarily.

Structural features amplify this behaviour. Fuel importers price fuel in dollars, and the monthly fuel pricing mechanism transmits foreign exchange movements immediately into pump prices. Logistics costs then move through the distribution of food, construction materials, consumer goods, and manufacturing inputs. Despite improvements, fertiliser and agricultural chemicals still depend heavily on imported content, tying agricultural costs to the exchange rate. Limited competition in distribution and food processing slows downward adjustment, even when costs ease.

Corporate balance sheets increase sensitivity further. Firms carry working capital facilities, supplier contracts, and lease obligations denominated in dollars. When the currency weakens, operating costs rise immediately. Retail prices adjust quickly to protect margins, thereby embedding pass-through effects across both consumer and producer prices.

This asymmetry explains why temporary currency strength does not produce broad relief and why the return to the target band requires consistent policy discipline. A premature rate cut would increase the likelihood of renewed depreciation and accelerate pass-through, particularly in the fuel and transport sectors. The result would be a broader inflation rebound in early 2026.

Concluding Remarks

The evidence across inflation dynamics, the exchange rate, reserves, and household balance sheets points in a single direction. The price level remains significantly above the target range of 6% to 8%. Annual inflation is easing gradually, but the underlying cost structure remains unchanged. Zambia’s foreign exchange market continues to exhibit shallow supply conditions, and stronger fundamentals did not underpin the recent appreciation. Reserve buffers look higher on paper, but they remain vulnerable because mechanical factors and episodic inflows drive them rather than sustained net market purchases.

Pass-through remains high. Fuel, transport, food distribution, and essential services respond quickly to foreign exchange movements and adjust slowly when the currency strengthens. These channels define the inflation profile and explain why temporary relief cannot produce durable disinflation. Real incomes remain compressed, and households continue to face persistent pressure across the items that shape daily life.

Under these conditions, a rate cut would increase the likelihood of renewed depreciation, widen the CPI level gap, and erode the credibility necessary to restore real purchasing power. It would also place further strain on reserve buffers and narrow the policy space available for stabilisation in early 2026. The risks are asymmetric. Easing into structural fragility raises the likelihood of a sharper correction later.

A firm stance, therefore, remains essential. Holding the policy rate protects the nominal anchor, reduces the probability of a second inflation round, and supports the gradual return to the target band. Stability requires policy discipline until external balances are strengthened through earned flows and until the domestic price structure exhibits genuine convergence.

Part Two will examine the credit system. It will assess liquidity conditions, foreign currency deposits, sovereign exposure, and the structural features that weaken transmission. These mechanisms explain why an early policy cut would not translate into improved access to credit and why the banking system absorbs rather than amplifies easing during periods of structural imbalance.

Source: IMF

The decision for November remains clear.

Hold the rate.

Preserve the anchor.

Protect the system.

Disclaimer

This article does not constitute legal, financial, or investment advice. The author shares views for perspective and discussion only. Do not rely on them as a substitute for professional advice tailored to your specific circumstances. Always consult a qualified legal, financial, investment, or other professional adviser before making decisions based on this content.

Canary Compass and the author accept no liability for actions taken or not taken based on the information in this article.

About the author

Dean N. Onyambu is the Founder and Chief Editor of Canary Compass. His insights draw on experience across trading, fund leadership, governance, and economic policy.

The Canary Compass Channel is available on @CanaryCompassWhatsApp for economic and financial market updates on the go.

Canary Compass is also available on Facebook: @CanaryCompassFacebook.

For more insights from Dean, you can follow him on LinkedIn @DeanNOnyambu, X @InfinitelyDean, or Facebook @DeanNathanielOnyambu.