Zambia Monetary Policy. Structure Before Sentiment. Part 3: Foundations for Transmission

From a stance that communicates to a system that responds

0. Executive Summary

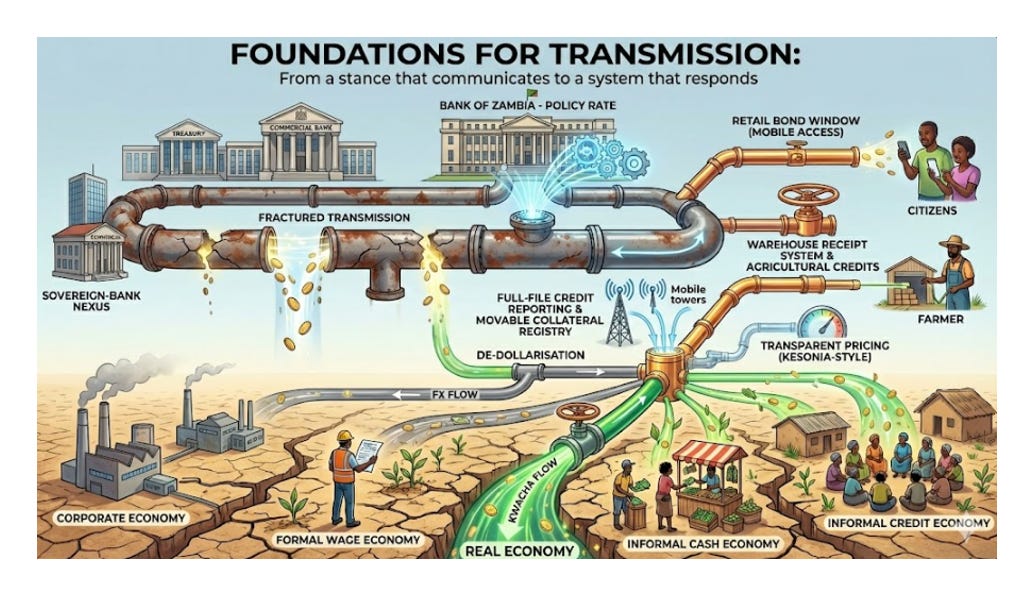

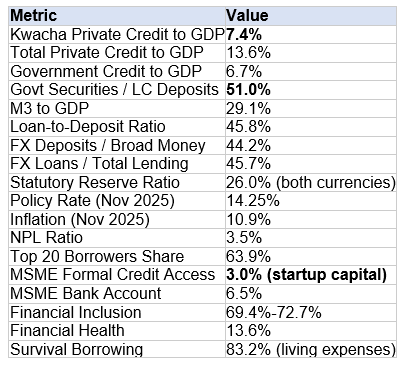

Zambia’s monetary policy rate operates in a structurally constrained environment. Genuine Kwacha-originated private credit stands at 7.4% of GDP. Commercial banks hold government securities equivalent to 51.0% of their local currency deposits. Foreign currency deposits account for 44.2% of broad money. Under these conditions, adjusting the policy rate does not meaningfully alter credit availability or borrowing costs for households and firms. The rate signals intent. The system does not carry it.

This paper identifies eight structural chokepoints that prevent transmission from reaching the real economy: the sovereign-bank nexus, dollarisation hysteresis, interbank segmentation, credit exclusion, information asymmetry, agricultural disconnection, pricing opacity, and legal and market infrastructure gaps. For each chokepoint, it presents specific interventions grounded in existing regulatory authority, pending legislation, and proven regional experience.

The core proposals are:

Break the sovereign-bank nexus by activating concentration-based risk weights under SI 62 of 2025, diversifying the investor base through a mobile-accessible retail bond window, and consolidating the government bond curve through benchmark issuance and switch auctions.

Reverse dollarisation structurally through asymmetric statutory reserve requirements (20.0% Kwacha, 35.0%+ foreign currency, fulfilled in Kwacha) that create ongoing local currency demand, combined with finalisation of currency directives and development of a liquid hedging market.

Unlock interbank liquidity by scaling Tradeclear’s umbrella guarantee facility, extending the term repo framework to 180-day tenors, and activating an interim Bank of Zambia co-guarantee if segmentation persists.

Expand the credit frontier through aggressive operationalisation of the movable collateral registry, linking Deposit Insurance Fund liquidity release to private sector loan-to-deposit targets, and establishing the SME Guarantee Fund with 90-day claims settlement.

Bridge the information gap by mandating full-file credit reporting from mobile network operators, utilities, and digital lenders, and integrating village bank credit histories into the formal credit bureau through an aggregator model.

Connect the farm gate to the policy rate through the Agriculture Credits and Warehouse Receipts Bill (N.A.B. 34 of 2025), Bank of Zambia eligibility for warehouse receipts at the discount window, and bundling credit with weather-index insurance.

Make pricing visible by requiring banks to publish weighted cost of funds and marginal cost of term funds, and adopting a KESONIA-style reference rate framework where loan pricing is expressed as reference rate plus margin.

Complete the legal architecture by securing passage of the Banking and Financial Services Bill (N.A.B. 36 of 2025), which contains netting and close-out provisions essential for repo and derivatives market depth.

Several of these tools gain power when combined. Linking loan-to-deposit ratio floors with tiered statutory reserve relief connects prudential policy to credit behaviour. Conditioning Deposit Insurance Fund liquidity release on private credit targets prevents released capital from recycling into government bonds. Aligning capital adequacy incentives with 8th National Development Plan priority sectors directs lending toward productive investment.

The sequencing runs in three phases. Phase One (Q1-Q2 2026) consolidates stability while laying the plumbing: asymmetric reserve requirements, SI 62 activation, MNO data integration, currency directive finalisation, and passage of the Banking and Financial Services Bill. Phase Two (2026-2027) rebuilds transmission inside the current stance: retail bond platform launch, Deposit Insurance Fund operationalisation with private credit conditionality, warehouse receipt scaling, village bank integration, and term repo extension. Phase Three (2027+) completes the architecture: full village bank aggregator model, liquid hedging market, complete agricultural transmission infrastructure, and countercyclical capital buffer inversion.

The test throughout is economic dignity: does each intervention give households, firms, and communities a fair chance to save in the unit of account, to borrow for productive needs on terms that reflect actual risk, and to withstand shocks without being wiped out?

This paper does not attempt to replace the medium-term fiscal and economic framework. It focuses on the monetary transmission channel inside that framework and on the specific plumbing that allows the policy rate to reach households and firms. The solutions exist. The sequence is clear. What remains is execution.

1. Executive Intent

Part 1 established why easing into an inflation overshoot and fragile external position carries real risk. Policy restraint is not ideological conservatism. Premature easing in a structurally constrained system amplifies volatility instead of stability.

Part 2 showed that shallow liquidity, valuation-driven money, and sovereign-anchored pricing prevent the policy stance from changing behaviour. Part 2.75 refined this with a crucial quantitative correction: genuine Kwacha-originated private credit stands at 7.4% of GDP, while commercial banks hold government securities equivalent to about 51.0% of their local currency deposits.

Part 3 moves from diagnosis to design. It addresses the central operational question facing the Bank of Zambia: what specific structural foundations must be laid for the Monetary Policy Rate to evolve from a signalling device for the interbank market into a credible pricing lever for the real economy?

This is not merely a technical challenge of transmission. It is a structural engineering problem involving the reconfiguration of incentives, the integration of excluded markets, and the dismantling of the sovereign-bank nexus that currently defines the financial architecture. The objective is not to criticise previous choices, but to upgrade the architecture until every actor responds rationally to a clear set of signals.

2. The Baseline: A Fractured Transmission Mechanism

To design effective solutions, we must first accept the severity of the transmission deficit. The numbers from Part 2.75 provide the definitive anchor. Part 2.75 showed how this narrow base reflects a banking system that prices and allocates around the sovereign rather than the productive economy.

2.1 The Depth Problem

Zambia’s broad money stands at 29.1% of GDP as of September 2025. Most emerging markets operate between 50.0% and 100.0%. Frontier markets sit between 30.0% and 50.0%. The global median approaches 60.0%. Zambia remains one of the shallowest monetary systems in the world. Transmission cannot strengthen when the base is this narrow.

Total commercial bank credit reaches approximately 20.3% of GDP. Of this, private sector credit is 13.6% and government credit is 6.7%. But the headline private credit figure overstates what reaches the real economy. Of that 13.6%, approximately 45.7% is denominated in foreign currency, credit that responds to Federal Reserve policy, not Bank of Zambia policy. Strip out the dollars, and genuine Kwacha private credit falls to 7.4% of GDP. This is the transmission base. Everything else is either government borrowing or currency-hedged lending that the policy rate cannot reach.

2.2 The Journey of K100

Part 2.75 traced the fate of a notional K100 entering the banking system. Approximately K26 is immediately sterilised by the Statutory Reserve Ratio. Of the remaining K74, banks must pledge government securities to access deposits from correspondent interbank or corporate institutions. This is not an investment choice. It is a structural requirement. In that world, the policy rate mainly prices sovereign rollover rather than new borrowing by households and firms. The result: more than half of remaining liquidity is absorbed by government securities, either directly or through collateralised interbank lending.

Under these conditions, a reduction in the policy rate does not translate into increased credit availability or lower borrowing costs for the real economy. It merely alters the yield dynamics of the sovereign debt portfolio. The residual liquidity available for private credit is negligible and rationed to a narrow segment of corporate and salary-backed borrowers.

2.3 The Four Economies

Zambia does not operate as a single economy. It functions across four distinct tracks that respond differently to every policy signal.

The corporate balance sheet economy is where large firms, mines, and strong names borrow. They raise working capital and term funding at negotiated spreads, often utilising foreign currency balance sheets. They “hear” the policy rate, but respond primarily to Treasury pricing and global liquidity conditions.

The formal wage economy is where employees interact with banks through salary accounts and personal loans. Existing borrowers feel the policy stance. When the rate falls, floating products reprice and monthly instalments come down, although relief is often partial. New borrowers face a different reality: high lending rates, tight credit screening, with margins, fees, and risk premiums keeping quoted borrowing costs elevated.

The informal cash economy is where many Zambians treat banks as places for money transfers rather than stores of value. Financial decisions centre on cash flow management, not interest rates. The policy rate is inaudible.

The informal credit economy runs through savings groups, village banks, suppliers, and landlords. Trust and reputation are the main assets. Record keeping is social rather than digital. The policy rate does not exist here. These systems are resilient and trusted in ways formal products are not, but they remain invisible to the central bank’s signal. Transmission will not improve if policy only speaks to formal contracts and ignores these informal balance sheets.

A single policy rate therefore delivers four different outcomes. The transmission architecture must reach all four economies, or it remains a message without a receiver.

2.4 Definitive Metrics (Part 2.75 Baseline)

Table 1: Transmission Baseline Metrics

These numbers define the starting position for any easing cycle. They are the constraints within which policy must operate.

3. Chokepoint One: The Sovereign-Bank Nexus

The primary obstruction to monetary transmission is the concentration of government securities on commercial bank balance sheets. With approximately 51.0% of local currency deposits absorbed by sovereign paper, banks have constructed a comfortable equilibrium. Returns on equity approach 30.0% without meaningful private sector credit risk. The zero risk weight on domestic government securities creates a regulatory subsidy that taxes private lending by comparison. No rational management team will walk away from that mix while regulation rewards it.

This is not a criticism of bank management. It recognises that the current architecture makes sovereign concentration the rational choice. Dismantling this nexus requires changing the incentive structure, not moral suasion.

3.1 Activating Capital Adequacy: SI 62 of 2025

The Banking and Financial Services (Capital Adequacy) Rules, 2025 (Statutory Instrument No. 62, issued 19 September 2025, effective 01 January 2026) provides the regulator with a potent toolkit. While traditionally viewed as prudential safeguards, these rules can be deployed as active instruments of monetary transmission.

Tiered Risk Weights on Sovereign Exposure

Under Rule 12 of SI 62, banks must classify assets and compute risk weighted assets in the manner that the Bank of Zambia determines, which in practice means the Bank sets the risk weights for different asset classes. The reform proposal: establish a concentration threshold for sovereign holdings. Holdings below the threshold necessary for liquidity management retain zero risk weight. Incremental holdings above this threshold attract progressive capital charges.

For illustration, the mechanism could operate as follows: 0.0% risk weight for sovereign holdings below 15.0% of total assets; 20.0% risk weight for holdings between 15.0%-25.0% of assets; 50.0% risk weight for holdings above 25.0%. This degrades the return on equity for excessive sovereign accumulation without destabilising the system. Banks retain their current positions but face increasing capital costs on marginal additions. These numbers are illustrative. The principle is to tax concentration, not to penalise liquidity management.

Risk mitigation: The specific bands require calibration after impact analysis, especially for smaller institutions, so that capital requirements do not trigger abrupt adjustments. Phased implementation with reasonable transition periods protects financial stability while reshaping incentives.

The Countercyclical Capital Buffer Inversion

Rule 9 of SI 62 introduces the Countercyclical Capital Buffer (CCyB), designed to protect the banking sector from periods of excess aggregate credit growth. Specifically, the rule requires each bank to build and maintain a countercyclical capital buffer between zero and 2.5% of risk weighted assets in common equity tier one, and to hold it in addition to the capital conservation buffer. In Zambia, where credit growth is anaemic rather than excessive, this tool can be repurposed within the Basel framework. This keeps Basel language intact while repurposing the tool to push credit toward the real economy. The regulator can explicitly link the release of capital buffers to targets for private sector credit extension.

The mechanism: if aggregate private sector credit growth remains below a defined Transmission Target, the CCyB requirement is set to zero or relaxed for compliant banks. Conversely, banks that fail to expand private sector books while continuing to accumulate government securities face higher Capital Conservation Buffer requirements. This transforms capital adequacy from a static safety metric into a dynamic incentive for lending.

Alignment with the 8th National Development Plan

The risk weight adjustments should align with national development priorities. Lower marginal risk weights for lending to agriculture, manufacturing, tourism, and mining, the priority sectors identified in the 8NDP, would direct released capital toward productive investment rather than allowing it to recycle into shorter-dated sovereign paper.

3.2 Diversifying the Investor Base: The Retail Bond Window

The 2026 Annual Borrowing Plan projects gross domestic borrowing of K106.0 billion: K21.6 billion financing part of the 2026 budget deficit, with the remaining K84.4 billion utilised to refinance domestic debt maturities. This volume threatens to perpetuate crowding out unless the investor base is radically diversified. The banking sector currently absorbs the lion’s share of short-term Treasury bills, treating them as high-yield substitutes for cash. This locks liquidity into a closed loop between Treasury and banks.

The solution is a digitised, friction-free retail bond window accessible via mobile money and integrated directly with the Central Securities Depository. Kenya’s M-Akiba shows that a mobile retail bond can open the door to first-time investors, but it also highlights the risks of poor user design and timing. The Zambian version should keep the rails simple, focus on primary purchases and redemptions, and build reminders, customer care, and clear exit rules from day one. The investor portal already allows households to buy government bonds and bills directly. This is positive for access. If we want retail bonds to reach beyond a narrow group of affluent investors, two design choices matter. First, the minimum ticket should move below one thousand Kwacha so that teachers, nurses, and marketeers can participate. Second, the portal must be fully integrated into mobile channels and agent networks. Without that, the retail window will remain shallow and the impact on savings and transmission will be limited.

Allowing households to purchase Treasury bills with amounts as low as K500 directly from their phones would tap savings currently sitting in mobile wallets while reducing bank deposit-to-bond arbitrage. The underlying infrastructure for dematerialised government securities and mobile payments already exists. This is a design-and-integration reform rather than a greenfield build.

The transmission impact operates through three channels. First, disintermediation lowers the cost of funds for the state by removing the bank spread. Second, competition forces banks to increase deposit rates to retain funds, strengthening interest rate pass-through to depositors. Third, liquidity pressure from migrating deposits forces banks toward higher-yielding private sector loans to maintain margins. The aim is not to push the whole rate structure higher, but to reallocate the existing margin away from cheap deposits and sovereign arbitrage and toward fairer returns for savers and productive credit.

A retail bond window can anchor digital savings products for informal and semi-formal workers by allowing fintechs and banks to wrap simple interfaces around direct holdings of government securities. This links the informal sector to the formal system without forcing households through complex brokerage channels.

3.3 Strengthening Primary Dealership and Secondary Market Liquidity

Zambia does not yet operate a formal primary dealer system for government securities. In practice, a small group of large banks underwrite most auctions and quote prices in the secondary market, so the building blocks for such a system already exist. The Capital Markets Master Plan and support from international partners treat a primary dealer framework as an unfinished reform. The task now is to put that framework in place and tie it to continuous price making rather than auction participation alone.

First, primary dealer obligations must centre on secondary market making and transparency rather than auction participation alone. This includes clear minimum firm quoting commitments on interbank trading screens, routine reporting of firm two-way prices over the curve, and participation in regular market making windows coordinated between the central bank and the Debt Management Office in the Ministry of Finance. Dealers that meet these obligations retain access to privileged auction allotments and central bank operations. Those that do not lose that status. This turns primary dealership from a label into a performance contract. Transparent criteria and published scorecards would support fairness and reduce perceptions of favouritism. Nigeria and South Africa already use versions of this model. Their primary dealers are named, bound by quoting rules, and rewarded through access to auctions and operations. Zambia can adapt those elements without copying the systems wholesale.

Second, the Bank of Zambia should extend repo lines explicitly to support market making. A dealer that commits firm prices on a five-year bond should be able to finance inventory at policy-linked rates through the standing facility. This allows dealers to hold inventory without draining balance sheet capacity, and it lets the central bank anchor market rates through liquidity provision rather than direct intervention.

For repo and securities lending to work at scale, there must be a third-party pool of bonds available to lend. In Zambia, pension funds and insurers already hold a large share of domestic fixed income and are among the main buyers of government securities. They are the natural long-term holders that can supply securities into the repo market.

Investment guidelines issued by the Pensions and Insurance Authority can therefore be adjusted so that a modest slice of each scheme’s government bond portfolio sits in an explicitly defined trading and lending bucket, while the bulk remains in a hold-to-maturity bucket. Within this small bucket, funds would be permitted to lend securities under standardised agreements and to adjust duration more actively, subject to liquidity and risk limits. This preserves prudential protection for retirement savings but frees enough paper to support a functional repo market.

Risk mitigation: this adjustment requires targeted upskilling for pension and insurance investment teams in duration management, valuation, and basic hedging so that they can run a small trading and lending bucket deliberately while keeping the bulk of retirement savings in long-term hold positions. The central bank, PIA, and the SEC can co-sponsor short, practical programmes on duration, basic hedging, and mark-to-market valuation.

Third, the framework must address the current fragmentation of trading rails. Most government bond trading in Zambia runs over Bloomberg E-Bond between dealers, with the Lusaka Securities Exchange (LuSE) acting mainly as a listing venue and registry for secondary reporting rather than as the main venue for price discovery. The exchange is not the real trading venue or price maker for these flows. Price discovery happens on the auction results and on dealer screens, not on the exchange board.

Secondary market transparency is therefore weak. Dealers execute on Bloomberg E-Bond and then report selected trades and quotes to the SEC. The regulator publishes a single average price per bond each day based on information submitted at ten in the morning, not a full tape of executed trades across the day. Households and smaller institutions do not see where bonds actually trade, and LuSE screens capture only a fraction of over-the-counter flows. The state expects investors to commit long-term savings into a market where live prices sit in dealer systems and regulatory spreadsheets rather than in the public domain.

Government bonds are issued and held in dematerialised form at the Bank of Zambia central securities depository, which is integrated with the real-time gross settlement system. LuSE operates a separate central securities depository for listed instruments and maintains investor accounts for listed debt, while relying on the Bank of Zambia system for settlement of government securities. By regulation, trades in listed bonds must be routed or reported through LuSE as a securities exchange, even though dealers quote and execute on the Bloomberg E-Bond platform. The exchange collects a fee on every reported trade without running the trading screen or carrying settlement risk. That is rent extraction, not infrastructure.

The SEC fee rules set a levy of 0.125% on the buy side and 0.125% on the sell side of every securities exchange trade, and apply the same rates to off-market trades. This is instrument neutral. It applies to equities and to bonds. LuSE then layers an exchange commission on top. On the published equity trading schedule, each side of a trade pays 0.125% to the SEC and 0.25% to LuSE, with brokerage commissions around 1.0%, and some brokers also note a small central depository levy. The Capital Markets Master Plan itself acknowledges that the LuSE business model relies heavily on trading fees from both bond and equity markets. The effect is that any secondary market round trip in a government bond that is executed through the exchange or registered as an off-market trade pays 0.25% of face value to the SEC alone, before exchange, depository, or broker commissions are added.

By regional standards this is punitive. Kenya’s central depository charges a 0.002% levy on bond transactions that it clears and settles. Nigeria’s Securities and Exchange Commission charges 0.025% of the value of all secondary bond market trades, with the exchange allowed to charge a similar amount. Zambia’s regulatory levy on a bond round trip is 0.25%, roughly ten times the Nigerian rate and more than one hundred times the Kenyan clearing levy, before any exchange or broker fees. It is very difficult to build a retail bond market on that cost base. Every time a pensioner, insurance saver, or retail investor turns over a government bond, statutory levies consume a much larger share of the ticket than in peer markets. A framework that claims to support capital markets should not tax secondary liquidity at these levels.

Treat Bloomberg E-Bond as the primary trading venue for government bonds and align the rules around it. LuSE can either integrate its post-trade reporting directly into that venue or step back into a pure reporting role with a fee that reflects the marginal cost of record-keeping. Over time, Zambia should move toward a single integrated architecture: one primary central securities depository at the central bank, a fully electronic bond trading platform with transparent quotes, and a repo and derivatives market built around that curve. South Africa shows what that looks like in practice, with an electronic interest rate market, a single central depository, and dealer trading that takes place on a deep electronic platform with transparent reporting. At present, liquidity must pass through three separate rails for the same asset: Bloomberg for trading, Bank of Zambia for settlement, and LuSE and the SEC for fees.

3.4 Consolidating the Curve: Benchmark Bonds, Switch Auctions, and the Auction Calendar

Even with better primary dealers, repo lines, and trading rails, the policy rate cannot speak through a fragmented curve. Zambia government bonds remain scattered across many small lines with limited depth at each maturity. That is expensive for a government that now relies heavily on domestic markets and has limited room for failed auctions or sudden jumps in yields.

Until January 2024, Zambia ran a benchmark bond programme. The domestic curve centred on a small set of core tenors, and the debt office reopened those lines to build size and liquidity. That architecture only paused when the government shifted to a par issuance regime in January 2024, issuing bonds at face value with market-driven coupons. The shift coincided with ZRA practice notes that extended withholding tax to discount income on bonds issued below par, which made standard taps and reopenings more costly for domestic investors. The mechanical problem was not the benchmarks themselves. It was the way tax policy treated discounts. Section 3.5 returns to that friction.

The 2026 Annual Borrowing Plan now commits to keeping bonds at face value and, at the same time, to restart active portfolio operations built around benchmarks. It states that Government bonds will continue to be issued at face value with market-driven coupon rates and that, from 2026, the government will undertake market-based domestic debt portfolio optimisation operations intended to deepen the domestic market through the reintroduction of the benchmark bond programme and to elongate and smooth the redemption profile of existing debt. In other words, benchmark bonds only stopped in January 2024 and are now being brought back under the current tax and par issuance regime.

Countries that run deep local markets combine benchmark bonds with exchanges and reopenings rather than relying on simple rollovers. Kenya, Botswana, Nigeria, and South Africa all use switches, buybacks, and reopenings to concentrate liquidity in a small set of lines and to reduce redemption walls instead of rolling them at any price. Zambia should follow the same path. The Ministry of Finance and the Bank of Zambia can define a small set of benchmark maturities and commit to reopening them until they reach credible sizes. Alongside new money issuance, the authorities can run switch auctions where investors in illiquid legacy bonds are invited to exchange into the benchmark lines. This reduces the number of small issues, lengthens the maturity profile where needed, and builds real depth at key points on the curve. It also lowers refinancing risk, because near-term peaks can be traded into longer tenors instead of rolled at every auction.

As we argued as far back as 2022, slow fiscal consolidation was always going to find its reckoning in 2026, when a heavy cluster of local bond maturities comes due. The warning was simple. If adjustment lagged, the government would not be able to roll that wall at acceptable yields. It would have to restructure its domestic bond stock in some form. Switch auctions are now the instrument that delivers that outcome. They are voluntary and market-based, and they respect legal contracts, but they change the timing and shape of cash flows. The state will present this as portfolio optimisation and redemption smoothing. In economic substance, it is a restructuring of the local bond stock through exchanges rather than through coercive losses.

The way auctions are scheduled matters for a sovereign under cash pressure. A rigid calendar that forces bonds into the market at fixed dates, regardless of liquidity conditions, creates a mechanical refinancing cycle. It increases the risk of failed auctions or forces the state to accept higher yields that compound the interest bill. The 2026 plan already allows some flexibility. It announces that indicative timing will be published through quarterly issuance calendars, with monthly bond auctions and fortnightly bills, and that separate calendars will be published for domestic debt portfolio optimisation operations with their own terms. That framework can support more flexible practice, where the government communicates its funding needs and intended maturities but retains discretion on timing, size, and the balance between new cash and switches within each quarter.

Kenya and Botswana show the advantage of this approach. They publish borrowing plans and auction windows but adjust issuance volumes and run switches when market conditions change. The lesson for Zambia is not to abandon transparency but to protect the balance sheet. A sovereign that is still largely shut out of affordable external markets cannot afford to be mechanical. It needs benchmark lines that are large and liquid, switch auctions that turn a fragmented stock into a curve, and auction flexibility that avoids paying crisis prices when the market is thin.

A future primary dealer system, a working repo market, and a rational fee structure will only function well on top of a curve that has depth at key tenors. Consolidation and flexible issuance are what create that depth. Without them, Zambia will continue rolling a scattered bond stock at high cost, and the policy rate will continue transmitting through a market that has no true benchmark. Section 3.5 turns to the final piece of this architecture: tax policy that does not quietly penalise the very mechanics that benchmarks and switch auctions require.

3.5 Benchmarks Need Tax Neutrality

Government intends to consolidate issuance into benchmark bonds and to reopen these lines through tap and switch operations. The 2026 Annual Borrowing Plan confirms that bonds will continue to be issued at face value with market-driven coupon rates and that the benchmark bond programme will be reintroduced as part of a wider set of domestic portfolio optimisation operations. In design terms, this returns Zambia toward the earlier benchmark structure that existed before the par issuance change in January 2024. It only works, however, if tax policy remains neutral across coupons, discounts, and premiums.

The Income Tax Amendment and ZRA practice notes now extend withholding tax to discount income on government paper that is issued below face value, not only to coupons, and the 2025 budget then lifts the rate from 15.0% to 20.0%. This is a reversion to a world where Treasury bills and discount bonds carried the discount, and coupons on bonds did the rest of the work. In a benchmark world, it becomes the reintroduction of a friction resolved a long time ago to support benchmark curves and secondary market trading. Each time the state reopens a bond line at a discount, investors face tax on both coupons and the embedded discount. Each time it reopens at a premium, investors pay a higher price for the same coupon but receive no corresponding tax relief.

The result is simple. Duration becomes more expensive at the very moment Zambia needs longer tenors and deeper secondary trading. Domestic households and institutions face the full 20.0% rate, while some foreign investors under double tax treaties pay closer to 10.0%. The tax wedge on local savings widens, not narrows. A benchmark programme that rests on taps and switch auctions therefore needs a clear decision. Tax coupons. Leave discounts and premiums on bonds outside the withholding net. Otherwise, the structure will continue to privilege short-term positions and offshore holders over local duration. The move from 15.0% to 20.0% withholding on coupons and discounts is, in effect, a silent restructuring of the government debt stock. It raises the tax burden on local savers relative to treaty-protected foreign investors and increases the gross coupon the state must pay to clear the market.

Extending withholding tax to discount income on bonds may deliver a short-term revenue boost, but over time it functions as a selective capital gains tax on duration. It penalises the very investors who are willing to hold longer tenors and deepens the bias toward short-dated, foreign-held paper. A state that claims to want benchmark bonds and a deep domestic market cannot simultaneously tax the mechanics that benchmarks require.

4. Chokepoint Two: Dollarisation Hysteresis

Zambia’s monetary system is structurally bifurcated. Foreign currency deposits account for approximately 44.2% of broad money. Foreign currency loans represent 45.7% of total lending. This creates a zone where the Bank of Zambia’s Kwacha interest rate signals are irrelevant. The policy rate operates only on the Kwacha portion; the dollar portion responds to Federal Reserve policy and the foreign currency reserve requirement.

4.1 The Limits of Sentiment-Based De-dollarisation

Zambia did not choose dollarisation by statute. It drifted into it. Ecuador adopted the United States dollar formally in 2000 as a deliberate response to crisis and in the process surrendered monetary policy. Zambia instead lives with de facto dollarisation driven by instability and mistrust of the Kwacha. That path is more corrosive. It weakens monetary policy without the clarity or discipline that comes with an explicit regime change.

High dollarisation damages four parts of the system at once. It blunts monetary policy because the policy rate does not speak to a large share of deposits and loans. It makes the economy more fragile to external shocks because every movement in the exchange rate hits balance sheets directly. It increases banking risk through currency mismatches between dollar liabilities and Kwacha cashflows. It also narrows exchange rate policy space because any FX adjustment passes quickly into prices. That is the backdrop against which any serious de-dollarisation strategy must be judged.

The expectation that macroeconomic stability alone will reverse dollarisation is contradicted by evidence. Economic literature and regional experience confirm the presence of hysteresis: once economic agents learn to distrust the local unit, they do not switch back merely because inflation stabilises or the exchange rate appreciates temporarily. Uruguay is a textbook case. Even after it restored macroeconomic stability and strengthened its policy framework, deposit dollarisation stayed near 69.0% and loan dollarisation around 49.0% for a long period. The central bank had to add targeted tools, such as tighter limits on foreign currency lending to non-tradable sectors and higher reserve requirements on foreign currency liabilities, before dollarisation began a slow, persistent decline. The lesson is structural: reducing dollar dominance, in countries like Zambia where hysteresis is entrenched, requires friction that makes holding foreign currency costly and incentives that make holding Kwacha attractive.

In Peru, the central bank combined asymmetric reserve requirements with other macroprudential measures, including higher risk weights for foreign currency loans to unhedged borrowers and liquidity requirements that favoured local currency instruments. Over two decades, this package reduced deposit dollarisation from about 80.0% to around 33.0%, but the process was gradual and required consistent policy over many years. Zambia needs to approach de-dollarisation with the same patience and the same realism about hysteresis.

The experience of Uruguay and Peru is clear. Prudential tools only work if they apply broadly. Every new exemption weakens the wedge and creates arbitrage opportunities. The lesson for Zambia is to apply the framework uniformly and resist pressure to carve out special cases, or the incentive structure collapses.

The current framework essentially subsidises dollarisation. Banks can accept USD deposits, lend them to exporters, importers, or the government, and earn a spread with minimal regulatory friction. The Statutory Reserve Ratio at 26.0% on both currencies is a symmetric blunt instrument that punishes Kwacha intermediation just as much as dollar intermediation.

Black markets do not appear because a state reduces the domestic use of foreign currency. They appear when enforcement is weak and rules are applied inconsistently. Nigeria and Kenya show that you can have thriving parallel markets without any formal de-dollarisation at all.

4.2 The Asymmetric SRR Proposal

The solution is an asymmetric Statutory Reserve Requirement. Reduce the current SRR on Kwacha deposits to 20.0% but raise the SRR on foreign currency deposits to 35.0% or higher. Crucially, require that the FX reserve be fulfilled in Kwacha, not dollars. This creates structural local currency demand: banks holding dollar deposits must acquire Kwacha to meet their reserve obligations, thereby tightening dollar liquidity while expanding Kwacha demand.

Risk mitigation: The specific rate requires calibration to ensure reserve adequacy and financial stability. Phased implementation allows banks to adjust funding structures. Additionally, when dollar deposits plateau or decline, banks may need to purchase dollars to fulfil customer withdrawals or to replenish core foreign currency deposits, so the net effect depends on flow dynamics.

Implementation should accompany finalisation of the Currency Directives that have been under consultation. These directives would restore Kwacha-based pricing for domestic transactions while leaving genuine foreign currency loans and accounts in place. Together, the asymmetric SRR and currency directives create a two-pronged approach: the SRR taxes dollar intermediation at the bank level, while the directives restrict dollar pricing at the transaction level.

Implementation can follow a staged sequence: Phase one focuses on new contracts and large-value payments; Phase two extends to existing contracts with defined transition windows; Phase three restricts foreign currency accounts to verified cross-border needs. The risk is delay, not overreach. Extended delays weaken the institutional signal precisely when the currency requires the strongest reinforcement.

4.3 The Currency Mismatch Problem

About 45.7% of total lending is denominated in foreign currency, yet the majority of borrowers operate in an economy where most revenues, working capital cycles, and shock absorbers remain in Kwacha. Importers pay USD invoices but sell into a Kwacha market. Some suppliers to mines receive USD on specific contracts, yet wages, logistics, rentals, and local services remain Kwacha-settled. Mall landlords may charge USD-indexed rent while tenants earn in Kwacha and must buy dollars in the market, so the strain of currency scarcity sits with the domestic side of the chain. From a distributional perspective, anchoring property values in USD is also one of the most exclusionary pricing structures in the system because it shifts housing and commercial space into a currency that most households and firms do not earn, which deepens inequality and financial exclusion over time. Local suppliers sometimes price goods in USD even when their own inputs are domestic, which is why currency directives and the draft Currency Regulations are designed to restore Kwacha-based pricing for domestic transactions while leaving genuine foreign currency loans and accounts in place. These arrangements meet the technical conditions for USD lending, but the borrower’s true repayment capacity still depends on Kwacha cash flow. When the exchange rate moves sharply or USD liquidity tightens, the mismatch becomes visible in arrears and non-performing loans, especially in construction, property, and trade.

Kenya offers a recent warning on how this structure can crack under pressure. Between 2021 and 2023, the shilling depreciated three years in a row, including a slide of about 26.8% in 2023, and by January 2024, the exchange rate briefly peaked around KES 160 per dollar before subsequent policy actions pulled it back. Over the same period, foreign currency loans climbed to about KSh 1.2 trillion by June 2023 as firms borrowed in dollars to cope with shortages. The IMF later reported that as dollar scarcity intensified, some FX borrowers who could not obtain dollars began offering repayment in shillings instead, which effectively counted as default and contributed to a rise in non-performing loans in the foreign currency portfolio, while Kenya’s overall NPL ratio rose to about 16.3% by June 2024 from 14.8% at the end of 2023. Zambia has stricter expectations regarding foreign currency linkage and is moving to re-anchor domestic contracts in Kwacha, but the underlying risk remains similar: when the currency comes under sustained pressure, balance-sheet dollarisation in an economy that still earns and spends mainly in local currency quickly becomes a credit risk.

Transmission, therefore, requires a functional derivatives market, not just a change in loan labels. Firms must be able to borrow in Kwacha, where the policy rate speaks, and use instruments like forwards, swaps, options, and non-deliverable forwards to manage the foreign component of their input costs. Today, the forward market is thin, and premiums often exceed the interest rate differential. That is a symptom of shallow balance sheets, weak market-making, and the absence of a proper netting and collateral framework.

The structural tax on dollar intermediation should remain in place, but firms should not be forced into naked currency risk as the price of accessing credit. Deep, fairly priced hedging instruments allow the real economy to carry trade and commodity risk, while the prudential and reserve framework discourages the banking system from treating dollar deposits as the default asset class.

5. Chokepoint Three: Interbank Segmentation

The transmission mechanism relies on the interbank market to distribute liquidity from surplus to deficit banks. In Zambia, this market is segmented. Tier 1 international banks and a few large domestic banks hold the surplus but are reluctant to lend to smaller local banks due to counterparty risk limits. The October 2025 Financial Stability Report indicates that a single lender supplied close to 39.0% of all interbank liquidity. This is not a market; it is an oligopoly.

The consequence: smaller banks bid up deposit rates to fund themselves, keeping the overall cost of funds high regardless of the policy rate. When the policy rate is cut, cheaper liquidity often fails to reach the banks that lend to SMEs.

5.1 Tradeclear and the Umbrella Guarantee

Frontclear is an international market development institution that provides guarantees and technical assistance for money markets. Tradeclear is its onshore Umbrella Guarantee Facility, a platform-based structure under which Frontclear guarantees the counterparty credit risk of participating banks in eligible interbank trades. The objective is simple: allow liquidity to flow across tiers of the banking system without each bilateral line being constrained by hard counterparty limits.

In Zambia, the authorities and Frontclear have already moved beyond concept. A feasibility study was completed in 2022, followed by legal and regulatory work on documentation and netting. Regulatory approval to launch Tradeclear Zambia was obtained in January 2024, with a target go-live in the second half of 2024. Public updates through 2024 and 2025 show that banks such as Zambia Industrial Commercial Bank and Indo Zambia Bank have signed up to participate in Tradeclear Zambia, and the Financial Stability Report notes that the central bank is facilitating implementation of the Umbrella Guarantee Facility to address segmentation in the interbank market.

What remains unclear from public information is not whether Tradeclear exists, but whether participation and transaction volumes will be large enough to change system-level behaviour. The policy priority is therefore to move from design and early onboarding to broad-based, routine use.

The reform pathway is threefold. First, the guarantee should be fully integrated into prudential and risk frameworks so that using Tradeclear-backed lines is clearly capital and liquidity-efficient for both local and international banks. Second, participation must become the norm rather than the exception: a clear roadmap for onboarding all banks that meet minimum governance and risk standards, combined with time-bound incentives for early adopters. Third, if segmentation persists despite the guarantee being in place, a narrow, time-bound official bridge can be considered: a limited co-guarantee or collateralised liquidity line for trades executed under the umbrella facility, for a defined period and size.

5.2 Term Repo Framework

The policy corridor must regain its role as the main reference for short-term liquidity. The operating target is the overnight interbank rate within a corridor defined by the standing deposit and lending facilities, but beyond the overnight point, term cash markets often look to Treasury bill auctions for direction. Liquidity therefore clears through the sovereign market because that is where depth exists, and term pricing reflects auction outcomes more than expectations of the policy path.

The solution is not to replace existing open market operations, but to extend them into a predictable term structure. A structured term repo framework, built on standard documentation and collateral schedules, would extend the central bank footprint beyond overnight operations and anchor more of the curve to the policy stance.

Regular auctions at a small set of standard tenors (7-day, 30-day, 90-day, and 180-day) would allow the policy stance to be heard beyond the front end. Term repos should be open to all banks that meet prudential criteria, with allotment rules that prevent a single large institution from capturing all liquidity. Smaller and mid-tier banks that can present eligible collateral would be able to access policy-anchored term funding without breaching internal counterparty limits.

6. Chokepoint Four: Credit Exclusion

The 2022 MSME Finance Survey reveals that 97.0% of MSME startup capital comes from personal savings or family, with formal credit contributing a negligible 3.0%. Only 6.5% of MSMEs have a bank account. The banking sector views MSMEs not as a market but as a liability due to informational opacity and collateral mismatches.

Crucially, the binding constraint is not price. FinScope 2020 shows that low interest rates sit near the bottom of borrower priorities when choosing a lender; only a very small share of adults cite cost of credit as the most important criterion, well below factors like proximity, speed, and simplicity. In the MSME Finance Survey, 21.6% of MSMEs who struggled to obtain loans point to lack of security or collateral, and 29.4% of formal business owners whose loan applications were rejected cite missing financial records as the main reason. The barriers are collateral, documentation, and information asymmetry. A lower policy rate cannot help borrowers who never meet a credit officer.

6.1 The Collateral Revolution: Movable Assets

The insistence on fixed collateral (land and buildings) creates a deadweight loss. Most MSMEs possess movable assets: inventory, accounts receivable, and equipment. But banks discount these to zero due to enforcement risks. The Movable Property (Security Interest) Act exists, but utilisation is low. Only about 30.8% of informal sector business owners report awareness of the movable collateral facility, with awareness of the broader collateral registry and guarantee schemes also low.

The movable property security interests regime already allows banks to register security over live assets such as cattle, poultry, and equipment in the PACRA collateral registry. Warehouse receipts will complement, not replace, this framework. They cover storable commodities such as grain and processed livestock products that can sit in certified warehouses. Live animals will continue to sit on the movable collateral side, where the challenge is valuation and monitoring rather than storage.

The solution lies in aggressive operationalisation of the electronic collateral registry, integrated with the PACRA database and the credit bureau. Crucially, the insolvency regime must be streamlined. If it takes two years to foreclose on a vehicle or seize inventory, the collateral is worthless. A specialised fast-track commercial court or tribunal for movable asset recovery would reduce the loss-given-default explicitly modelled in banks’ capital calculations under Basel norms.

Ghana’s experience is instructive: between 1 June 2016 and 31 December 2019, an IFC-supported programme with the Bank of Ghana updated the secured transactions law, upgraded the web-based collateral registry, and trained lenders, courts, and bailiffs. By the end of June 2019, the improved registry had recorded more than 269,000 secured charges. Over the same period, the project facilitated approximately $53.1 billion in financing, exceeding the initial target of $44.0 billion. For the sampled institutions, movable assets secured roughly 80.0%-83.0% of SME loan value over 2017-2019, and Bank of Ghana data for 2018 show that 88.0% of secured assets registered were movable.

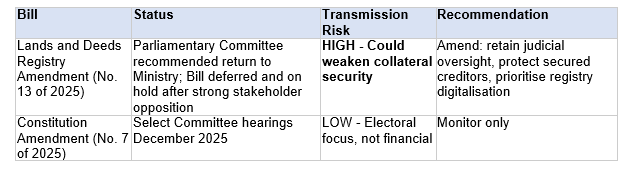

6.2 The Lands and Deeds Registry Amendment Bill (No. 13 of 2025)

Parliament has been considering the Lands and Deeds Registry (Amendment) Bill, No. 13 of 2025. Its core objective is to amend the Lands and Deeds Registry Act to grant the Chief Registrar the power to cancel a Certificate of Title. The bill generated significant opposition from ZiCA, the Law Association of Zambia, and legal practitioners. Following stakeholder objections, the Parliamentary Committee recommended return to the Ministry; the Bill is now deferred and on hold.

ZiCA warned that the bill’s provisions could “erode lender confidence, making financial institutions more cautious in accepting land and buildings as security,” with knock-on effects for access to credit, especially for smallholder farmers and emerging businesses that rely on title as their main asset. Senior counsel argued that title cancellation should remain under judicial supervision rather than be left to purely administrative discretion.

A transmission-aligned approach would keep the fraud problem in view but protect the credit channel. First, title cancellation for fraud or error should continue to pass through a defined judicial process, with clear timelines and a dedicated commercial or land division, rather than resting solely on administrative discretion. Second, a fast-track commercial and land court track for disputes over registered property would give lenders and borrowers predictable resolution on enforcement. Third, the priority in the near term should be full digitalisation and clean-up of the registry, including back-capturing of historical records, before any major expansion of administrative cancellation powers. Fourth, the law should explicitly protect bona fide purchasers and secured creditors who acted in good faith.

6.3 Deposit Insurance as a Transmission Tool

The impending operationalisation of the Deposit Insurance Fund (DIF) via the 2025 framework is a transmission opportunity often overlooked. The draft framework sets a coverage limit of K150,000 with a 0.05% premium, parameters that the Bank of Zambia can adjust as the Deposit Insurance Fund matures. Banks currently hoard liquidity partly to self-insure against runs. The DIF transfers this tail risk from individual bank balance sheets to the collective fund.

As the DIF builds, the Bank of Zambia can justify lowering liquid asset ratios and potentially the SRR for compliant banks. The logic is explicit: the insurance fund replaces the need for excessive prudential liquidity. This releases trapped capital for lending.

To ensure released liquidity does not flow back to government bonds, the relaxation should be conditional on maintaining a minimum private sector Loan-to-Deposit Ratio. The mechanism: 50.0% private LDR = 200bp SRR relief; 60.0% private LDR = 400bp SRR relief. This links the prudential tool directly to credit behaviour. The exact numbers require calibration and consultation, but the principle is clear: prudential tools should reward genuine intermediation into households and firms rather than balance sheet rotation into sovereign assets.

Once the Deposit Insurance Fund reaches critical mass, it should sit alongside the Liquidity Coverage Ratio as the first line of defence for depositors. Under Basel standards, banks hold high-quality liquid assets to survive a stress run over thirty days. Deposit insurance does something different. It reduces the incentive for households to run in the first place. When both are in place, the supervisor can afford to rely more on LCR and DIF and less on blunt tools such as a very high statutory reserve requirement. Over time, Zambia should set an explicit glide path where rising DIF coverage and full Basel liquidity implementation allow the statutory reserve ratio to fall. That is how you free cash for credit without weakening resilience.

Emerging-market central banks, such as SARB, have supplemented the LCR with committed liquidity facilities that allow banks to pre-position government securities and pay a fee for a contingent line of credit from the central bank. In systems where government paper dominates liquid assets, this kind of facility helps reconcile three goals at once. It lets banks count a portion of their government bond holdings as LCR eligible, supports a market for those bonds, and frees up cash for private credit. Zambia does not need to copy the South African model in full. It can, however, use the same principle. As DIF accumulates and Basel liquidity standards bed in, the policy mix should gradually move away from static cash reserves and toward a combination of LCR, DIF, and well-designed central bank liquidity facilities.

6.4 The SME Guarantee Fund

The September 2025 Budget Speech announced a K5.0 billion fund to guarantee bank loans to qualifying small and medium enterprises. This addresses the collateral gap directly. However, guarantee funds only work if claims are paid quickly and criteria are transparent.

For guarantees to become transmission tools, three changes are required. First, coverage should apply to incremental lending rather than the entire legacy portfolio—this focuses the fiscal and risk support on new credit creation, not on de-risking what banks would have lent anyway. Second, claims must be honoured within defined timelines (90 days maximum) so that guarantees function as capital substitutes rather than political promises. Third, pricing should reflect performance: guarantee fees should decline for institutions that demonstrate low default rates, creating a virtuous cycle.

7. Chokepoint Five: Information Asymmetry

Banks reject borrowers not only for lack of collateral, but for lack of information. The credit bureau contains negative data (defaults), but “positive data” (repayment histories of millions of Zambians who use digital loans, pay utility bills, and participate in village banking) is largely absent from the formal credit score.

7.1 Full-File Credit Reporting

Zambia already has a legal framework for full-file credit reporting. Bank of Zambia guidelines on credit data sharing require providers to submit both positive and negative information on borrowers to licensed credit bureaus, and the newer credit reporting law builds on this foundation. In practice, coverage remains thin and tilted toward defaults. Bank of Zambia has noted that only a small share of adults are visible in credit bureaus and that many lenders use the system mainly to blacklist customers rather than to price risk over the life of the relationship.

NFIS II already treats stronger credit infrastructure as a national priority. It calls for an integrated digital data warehouse and better use of alternative information to support MSME and household lending, with indicators that track both negative and positive reports in the credit reporting system. The gap is therefore not vision. It is implementation. Digital lenders, mobile money credit products, and large utilities already hold detailed records of how households handle small obligations. Some of these providers already consult and list with credit bureaus, usually when loans fall into arrears. Transmission requires that this information moves from scattered private scoring engines into a shared credit infrastructure that counts good behaviour as well as default.

Regulators should therefore require every licensed provider that extends credit or postpaid services to submit both on-time and overdue payment histories to licensed bureaus in a standard format. Credit bureaus in turn should be required to produce simple retail and small enterprise scores that blend bank loans with this full-file data and make those scores available to banks and regulated microfinance institutions on equal terms. A trader who has repaid dozens of small digital loans on time, or a salaried worker whose utility bills are current, should be able to present that record inside a mainstream bank application. NFIS II already points in this direction. The reform is to turn that aspiration into a live, regulated data pipeline rather than a policy statement.

7.2 Bridging Informal and Formal Credit Systems

In Zambia, village banking groups already straddle both worlds. The lending decisions and pricing live inside the group, where members lend to each other from a common pool at rates that can reach 10.0% per month. The pooled funds, however, increasingly sit in group accounts at commercial banks such as Zanaco, ZICB, Access Bank, and FNB. The link to the formal system is therefore already present in the funding leg. The missing piece is the credit pipe. Very little of the information on who borrows, who repays, and who defaults makes its way into the formal credit registry. That is where monetary policy transmission is lost.

SaveNet groups alone mobilise over K70.0 million in savings, but this capital circulates in closed loops, disconnected from the sovereign yield curve. The Lusaka and Copperbelt provinces (with the highest density of bank branches) have the highest proportion of adults in informal savings groups (17.7% and 14.6% respectively in FinScope 2020). This is not exclusion due to distance. This is active substitution. Urban populations with access to banks are choosing informal groups.

The way forward is not to turn every village banking leader into a mini bank manager. It is to make it easy, and attractive, for groups to record their credit histories in a standard format that plugs into the CRB. Banks that already hold VB group accounts can offer a simple digital ledger as part of their product, where groups tag their loans and repayments to individual members. Over time, members who consistently save and repay can graduate into formal credit products without dismantling the group itself. The group remains the primary lender for small, fast loans. The bank becomes a second-tier lender for members who need larger, longer-term credit and have demonstrated discipline through the group.

The transmission implication is profound: for the urban working class, the “social contract” of the savings group is superior to the “commercial contract” of the bank. The impediment is behavioural, not infrastructural.

Banks should be incentivised to treat Village Banks not as individual customers but as corporate entities or aggregated units. The solution: group accounts with sub-accounts or digital wallets. Banks can absorb the liquidity of the informal sector onto their balance sheets, increasing the deposit base and lowering the cost of funds. In return, the group gets a credit line based on its collective savings history.

This structure transmits the policy rate: if the Bank of Zambia lowers rates, the wholesale line to the Village Bank becomes cheaper, lowering the cost of capital for micro-entrepreneurs within the group. Evidence replaces absence. Risk is priced rather than avoided. The community credit ledger treats the group as one balance sheet with many sub-accounts, not as scattered individuals.

The BoZ’s July 2023 literature review on linking informal savings groups to formal FSPs provides the framework. Digital platforms like Jamii.One demonstrate viability, recording every meeting’s savings, loans, and repayments to build credible financial histories.

8. Chokepoint Six: Agricultural Disconnection

Agriculture employs the majority of Zambians but receives a fraction of formal credit. The sector is characterised by a “subsidy dependence” model rather than a “finance” model. The 2022 MSME Finance Survey shows that 62.7% of MSMEs operate in agriculture, yet the Stability and Resilience Facility directed 83.3% of its K2.5 billion in approved funds specifically to agriculture, forestry, and fishing. This pattern underscores that commercial banks are unwilling to carry agricultural risk at market pricing. The policy rate transmission fails, forcing the central bank to step in with targeted, subsidised bypass.

8.1 The Legislative Package

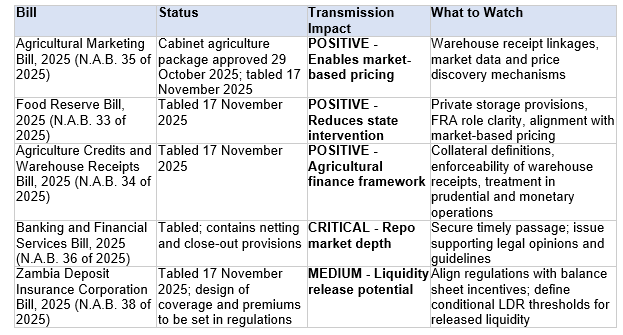

The September 2025 Budget Speech announced three legislative initiatives: the Agricultural Marketing Bill, amendments to the Food Reserve Act (2020), and amendments to the Agricultural Credits Act (2010). These proposals have since come to Parliament as standalone Bills: the Food Reserve Bill, 2025 (N.A.B. 33 of 2025), the Agriculture Credits and Warehouse Receipts Bill, 2025 (N.A.B. 34 of 2025), and the Agricultural Marketing Bill, 2025 (N.A.B. 35 of 2025). Together they mark a shift from ad hoc state intervention toward a market-based architecture built around a redefined Food Reserve Agency, a new agricultural marketing council, and a modern warehouse receipt regime.

The Warehouse Receipt System is the crux of agricultural transmission. If a farmer can deposit grain in a certified warehouse and receive a receipt that is legally recognised as a tradable financial instrument, they can use it as collateral for a bank loan. This financialises the harvest. ZAMACE already operates the infrastructure, though it remains underutilised. The Agriculture Credits and Warehouse Receipts Bill, 2025 continues the Warehouse Licensing Authority, establishes an electronic warehouse receipt system, and defines the rights and obligations of warehouse operators, depositors, receipt holders, and lenders.

The Bank of Zambia should accept Warehouse Receipts as eligible collateral for its own liquidity operations. Subject to conservative haircuts and strict quality controls on warehouses and commodities, if a commercial bank knows it can repo a warehouse receipt with the central bank, it will be far more willing to lend against it. This connects the policy rate directly to the farm gate price. If the central bank accepts warehouse receipts as collateral, the farm gate enters monetary operations.

8.2 Weather Index Insurance

The volatility of rain-fed agriculture makes it a “bad risk” for banks. FinScope 2020 shows that 65.8% of adults report experiencing climate change effects such as heat waves, drought, crop failure, pollution, or excessive rainfall. The 2022 MSME Finance Survey shows that less than 2.0% of MSMEs have savings, insurance, investment, or securities accounts, which implies that agricultural insurance coverage sits in the low single digits.

Bundling credit with mandatory weather-index insurance (where payouts are triggered by satellite data on rainfall and related indicators rather than individual claims assessment) de-risks the loan portfolio. The R4 Insurance-for-Work model in East Africa demonstrates viability for low-income farmers. The Pensions and Insurance Authority and Bank of Zambia must coordinate to ensure these hybrid products are regulatory-compliant and capital-efficient for banks. If drought risk sits in an index insurance pool instead of the bank credit book, the risk premium in loan pricing can fall without endangering solvency.

9. Chokepoint Seven: Transparency and Pricing

Transparency is a structural reform disguised as a procedural adjustment. The transmission mechanism does not end at the corridor. It ends at the loan contract. If borrowers and depositors cannot see how banks price money, they cannot tell whether policy easing supports the real economy or mainly supports margins.

9.1 The Current Opacity

Zambia already has part of the picture. The Bank of Zambia publishes detailed lending rate data by segment. For the week ending 26 September 2025, average rates were 28.59% for retail borrowers and 23.74% for non-retail borrowers. What the public cannot see is the cost of funding that sits underneath those rates. Without that anchor, spreads remain abstract and debate becomes emotional rather than factual.

True lending spreads include three components: the marginal cost of term funding at the relevant tenor; expected loss from default based on historical performance and sectoral risk; and the cost of capital required by regulation. When critics compare savings rates with multi-year loan rates, they miss these layers and misdiagnose the spread. Transparency realigns incentives without destabilising balance sheets.

9.2 The Kenya KESONIA Model

Kenya has moved first. The Central Bank of Kenya has issued a revised Risk-Based Credit Pricing Model under which the Kenya Shilling Overnight Interbank Average (KESONIA) is adopted as the common reference rate for Kenya shilling variable loans, effective for new facilities from 1 September 2025, with existing variable loans transitioning by February 2026. Where KESONIA use is not practical, the Central Bank Rate (CBR) is allowed as a fallback reference. The lending rate is expressed as KESONIA plus a premium. The premium covers operating costs, return to shareholders, and the risk profile of the borrower. Banks must disclose the reference rate, the premium, and all fees and charges for each product.

The design is simple. The market can see what part of the rate reflects system funding conditions and what part reflects bank behaviour. Monetary policy speaks through KESONIA. Banks express their judgement through the premium.

9.3 India’s Progression

India took a different route with the same objective. In 2010, the Reserve Bank replaced the Benchmark Prime Lending Rate with a Base Rate system that forced banks to compute a cost-based internal benchmark. In 2016, RBI moved further with the Marginal Cost of Funds Based Lending Rate (MCLR), requiring banks to set tenor-specific benchmarks based on marginal rather than average funding costs. From 2019, most new retail and MSME loans link to external benchmarks such as the policy repo rate.

Research using firm-level data shows that pass-through improved from 11-19 basis points under Base Rate to 26-47 basis points under MCLR. Borrowing costs fell once banks could no longer hide margins behind opaque benchmarks and discretionary spreads.

9.4 The Zambian Implementation

Zambia should build on these lessons. The Bank of Zambia should require every bank to publish its weighted cost of funds on a regular, standardised schedule. That figure is the average rate a bank pays across its deposits and other funding sources. It is the anchor for credit pricing and the clearest indicator of whether margins reflect genuine risk and capital requirements, or whether they mainly reflect market power and information gaps.

Alongside this, banks should publish the weighted marginal cost of term funds for core tenors: 3 months, 6 months, 1 year, and 3 years. Term lending is not priced off overnight deposits. It is priced off the cost of matching the tenor of a loan to the tenor of funds raised.

Loan offer letters would present the price as a simple equation: reference rate plus bank margin plus fees, with an annual percentage rate that includes all mandatory charges. When rates reprice, banks inform customers whether the change comes from the reference rate, from an adjustment in the margin, or from a change in fees. Once this structure is in place, public debate can focus on each component rather than on a single headline rate.

9.5 Funds Transfer Pricing

Internally, regulators should align this transparency with funds transfer pricing. Business units inside banks should borrow from the treasury desk at the same marginal cost of term funds that underpins the disclosed cost of funds, not at opaque internal rates. This anchors product pricing to the real funding curve and prevents cheap central bank liquidity and low-cost deposits from being marked up inside the bank before they reach the customer. The treasury desk should face a documented funding curve tied to deposits, term instruments, and central bank operations, and that curve should be available to the supervisor. Bank of Zambia can then review funds transfer pricing models as part of supervision, checking that internal prices track published benchmarks rather than shadow rates that disconnect customer pricing from system conditions.

Banks may argue that this level of scrutiny is competitively sensitive. The argument is weak. Banks already study each other’s funding structures and pricing through published financial statements, and large corporates already compare offers across institutions. The current opacity only leaves households, small firms, and depositors without visibility. A requirement that internal funds transfer prices line up with disclosed funding costs does not reveal trade secrets. It simply closes the gap between what banks know about each other and what the public can see, and it gives monetary policy a clean line of sight from the policy rate to lending rates.

10. Chokepoint Eight: Legal and Market Infrastructure

The June 2025 Zambanker highlights several initiatives aimed at improving market infrastructure, acknowledging that gaps have hindered the policy transmission mechanism. Legal reforms are necessary but not yet complete.

10.1 Netting Legislation

The Bank of Zambia has been working to enhance the legal enforceability of key financial agreements, notably the ISDA Master Agreement for derivatives and the Global Master Repurchase Agreement (GMRA) for repos. The substance of netting provisions is now incorporated in the Banking and Financial Services Bill, 2025 (Bill No. 36), with sections on netting and close-out currently before Parliament.

This reform is essential for deepening interbank and derivative markets. Without a netting framework, banks are reluctant to trade or lend to each other for fear that claims could not be safely settled in a default. This inhibits the development of a robust money market, thereby weakening monetary policy transmission. When policy changes, banks and non-banks need to adjust portfolios through market transactions; a functioning repo market makes this fluid.

The netting provisions should be prioritised for passage. They are technical, non-controversial, and foundational for every other market development initiative. With enforceable netting, banks can safely run larger books of repos and swaps. That depth is what allows portfolios to move when the policy rate changes.

10.2 Payment System Upgrades

In early 2025, the operating hours of the Zambia Interbank Payment and Settlement System (ZIPSS) were extended to 07:00-19:30 on weekdays with Saturday hours introduced. This supports the push toward a 24/7 economy with improved liquidity availability, reduced collateral costs, and faster settlement.

The National Financial Switch links banks and mobile service providers, enabling interoperability of digital payments. By expanding the financial services ecosystem and reaching underserved areas, the NFS improves the reach of monetary policy. When policy changes influence banks’ interest or liquidity, those effects can be passed on via mobile wallets and agent banking to a broader population. For these gains to hold, digital payment pricing must remain aligned with financial inclusion objectives, since high transaction costs can mute the very channels the payment infrastructure is designed to strengthen.

11. Legislative Assessment: Bills and Transmission

Several legislative initiatives are in various stages of development. Their design and implementation will materially affect transmission strength.

11.1 Bills Currently Before Parliament

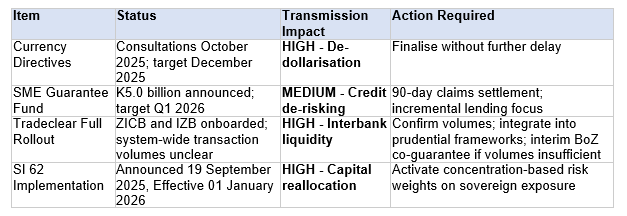

Table 2: Bills Before Parliament—Transmission Assessment

11.2 Bills Tabled in Parliament (November 2025)

Table 3: Agricultural and Financial Services Bills—Transmission Assessment

11.3 Regulatory Frameworks Pending (Non-Legislative)

Table 4: Regulatory Frameworks—Status and Action Required

12. Sequencing: The Order of Reform

Reform must follow sequence because each foundation enables the next. Zambia cannot fix transmission by adjusting the stance. It must build the system that carries it.

12.1 Phase One: Immediate (Q1-Q2 2026)

This phase consolidates stability and sets direction. The policy rate remains in restrictive territory while the plumbing is prepared.

• Implement asymmetric SRR (20.0% Kwacha / 35.0%+ FX, fulfilled in Kwacha)

• Activate SI 62 concentration-based risk weights on sovereign exposure

• Mandate MNO and utility data integration with Credit Reference Bureau

• Finalise Currency Directives without further delay

• If Tradeclear volumes insufficient: activate BoZ interim interbank co-guarantee

• Secure passage of Banking and Financial Services Bill, 2025, including netting provisions

• Publish weighted and marginal cost of funds disclosure framework

12.2 Phase Two: Medium Term (2026-2027)

This phase rebuilds transmission inside the current stance. It can begin while the policy rate remains elevated.

• Launch retail bond platform (mobile-direct T-bill access)

• Operationalise DIF with conditional liquidity release tied to private LDR targets

• Scale Warehouse Receipt System with BoZ eligibility for discount window

• Integrate village bank data into CRB via aggregator model

• Extend regular and calendarised term repo framework to 180-day tenor

• Operationalise SME Guarantee Fund with 90-day claims settlement

• Implement KESONIA-style reference rate framework

12.3 Phase Three: Long Term (2027+)

This phase completes the architecture. Easing becomes structurally effective.

• Full village bank aggregator model operational nationwide

• Liquid hedging market with market-maker support

• Complete agricultural transmission infrastructure (WRS + index insurance + credit)

• Primary dealer two-way quote obligations active

• CCyB inversion operational (buffer release tied to credit targets)

13. Novel Combinations: Tools Working Together

The interventions described above gain power when combined. Several novel pairings merit explicit attention.

13.1 LDR Floor + Tiered SRR

Linking the Loan-to-Deposit Ratio to reserve requirement relief creates a direct incentive for lending. A bank achieving 50.0% private sector LDR receives 200bp SRR relief; 60.0% LDR earns 400bp relief. This connects the prudential tool to credit behaviour rather than treating them as separate policy domains.

13.2 DIF + Private Credit Mandate

Deposit insurance releases liquidity that banks previously held as self-insurance against runs. Without conditions, this released capital flows back to government bonds, the path of least resistance. Conditioning DIF liquidity release on private LDR targets prevents recycling and ensures released capital reaches the real economy.

13.3 Asymmetric SRR + Kwacha Fulfilment

Requiring FX reserves to be fulfilled in Kwacha creates structural local currency demand. Banks holding dollar deposits must sell dollars to buy Kwacha to meet their reserve requirements. This is not a one-time shock but an ongoing flow that supports the currency while taxing dollar intermediation. It is also important to remember that when USD deposits plateau or start to decline, banks may need to purchase dollars to fulfil withdrawals from customers or to replenish core foreign currency deposits.

13.4 SI 62 + 8NDP Priority Sectors

Aligning capital adequacy with development planning means lower marginal risk weights for lending to agriculture, manufacturing, tourism, and mining. This directs released capital toward productive sectors identified in the 8th National Development Plan rather than allowing it to recycle into sovereign paper.

13.5 Warehouse Receipts + BoZ Eligibility

If commercial banks can repo warehouse receipts with the central bank, agricultural collateral enters the monetary operations framework. This financialises the harvest at the level of central bank operations, not just commercial bank balance sheets. The policy rate connects directly to the farm gate.

14. Closing: Structure Before Sentiment

Monetary policy is the last mile of state architecture. It does not create stability on its own. It reflects whether the system beneath it can carry the signal.

Zambia must earn the right to ease. That requires balance sheets that allocate to the productive economy, liquidity that hears the corridor, a currency structure that anchors expectations, a credit architecture that includes the majority, and pricing that is transparent and disciplined.

Without these foundations, easing is sentiment. With them, easing becomes policy.