Zambia Monetary Policy: Structure Before Sentiment. Part 2.5 Interlude: Why One Third Matters in a Shallow System

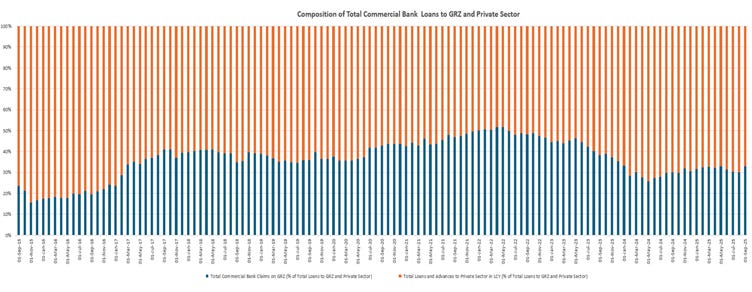

Shares of Total Commercial Bank Kwacha Loans and Advances to GRZ and the Private Sector, 2015 to 2025

Editor’s Note (December 5, 2025): Following clarifications from the Bank of Zambia on how foreign currency loans are reported in kwacha-denominated returns, some figures in this article have been refined. Part 2.75 of this series documents the corrections and provides updated analysis. The directional findings and core thesis remain unchanged. [Link to Part 2.75]

All charts are compiled from Bank of Zambia data and author calculations.

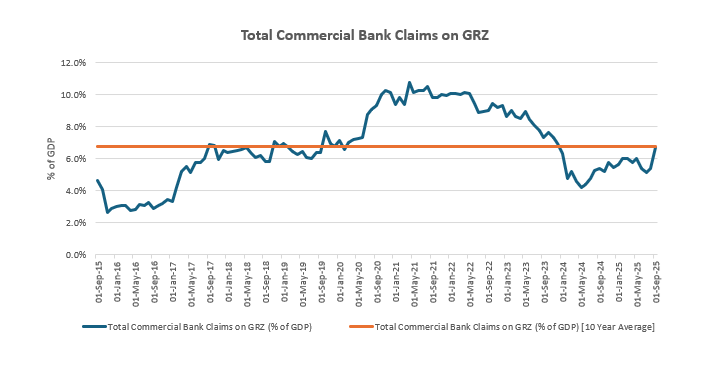

Over the last decade, total commercial bank claims on government (current stock: 6.7% of GDP; decade average: 6.8%) have averaged about 36.5% of total kwacha loans and advances to government and the private sector. In September 2025, the share stood near 33%. On the surface, a third does not look excessive. Many larger banking systems carry similar or even higher sovereign shares without impairing private credit.

The difference in Zambia is the depth of the system underneath that ratio. Kwacha loans to the private sector are around 13.6% of GDP (decade average: 11.5%), and total kwacha loans, including government, are around 20.3% of GDP (decade average: 18.3%). When total commercial bank domestic kwacha credit accounts for only about 20% of GDP, allocating a third to the government is not a neutral portfolio choice. It pits the sovereign and the entire private economy against each other for scarce balance-sheet capacity.

This is why a third matters. In deep systems where bank credit and non-bank finance reach 60% to 80% of GDP, a one-third sovereign share still leaves ample room for firms and households. Zambia does not have that depth. A one-third sovereign allocation inside a shallow system creates structural crowd out, not because the share is internationally unusual but because the base cannot absorb it.

It is also essential to clearly define the private economy. Large formal firms rely almost entirely on commercial banks. Small and medium-sized businesses rely on banks, suppliers, digital lenders, and guarantee facilities. Households, microenterprises, and informal producers rely mainly on village banks, savings groups, and community credit. With no deep non-bank markets, the entire economy feels the impact when bank balance sheets lean heavily toward the government.

In a shallow system like Zambia’s, only two near-term levers can free up space for private-sector credit. Fiscal consolidation can reduce domestic issuance. Prudential rules can cap the growth of sovereign exposures when fiscal adjustment falls short. Both tools work and often work best together. Ghana achieved meaningful progress when domestic borrowing needs fell and the yield curve stabilised after the domestic debt exchange. The earlier HIPC and MDRI period showed the same effect. Nigeria relied more on prudential measures, imposing differentiated reserve requirements on excess sovereign holdings and binding loan-to-deposit targets that rewarded real-sector lending. The lesson is clear. When the credit base is narrow, banks have no incentive to move away from high-yielding, zero-risk-in-principle sovereign assets. A shift of this nature requires deliberate fiscal action, deliberate regulatory action, or both.

Zambia also needs to expand its credit base. A system with domestic credit near 20% of GDP cannot transmit policy with discipline or absorb shocks. Expanding the base requires stronger savings mobilisation, broader formalisation, deeper institutional investors, and a credit architecture that draws in the informal majority. This is the long-term lever that supports every other reform. Without a broader foundation, Zambia will continue to debate the allocation of a small pool rather than build a financial system that can support real economic growth.

Part 1 explained why cutting into an inflation overshoot and a fragile external position carries risk. Part 2 showed why shallow, FX-driven money and sovereign anchored pricing prevent stance from moving behaviour. Part 3 will set out the foundations for transmission to work and the sequence that can move Zambia from a stance that communicates to a system that responds.

Disclaimer

This article does not constitute legal, financial, or investment advice. The author shares views for perspective and discussion only. Do not rely on them as a substitute for professional advice tailored to your specific circumstances. Always consult a qualified legal, financial, investment, or other professional adviser before making decisions based on this content.

Canary Compass and the author accept no liability for actions taken or not taken based on the information in this article.

About the author

Dean N. Onyambu is the Founder and Chief Editor of Canary Compass. His insights draw on experience across trading, fund leadership, governance, and economic policy.

The Canary Compass Channel is available on @CanaryCompassWhatsApp for economic and financial market updates on the go.

Canary Compass is also available on Facebook: @CanaryCompassFacebook.

For more insights from Dean, you can follow him on LinkedIn @DeanNOnyambu, X @InfinitelyDean, or Facebook @DeanNathanielOnyambu.