Zambia Monetary Policy. Structure Before Sentiment. Part 4: The World Will Not Wait

Surviving the squeeze, the shadow fiscal arm, and the illusion of easy exits

Image: AI-generated illustration of “Copper Dollar’s Journey” (Section 3)

0. Executive Summary

Zambia’s monetary policy debate still defaults to a single instinct: cut rates, push credit, ease pain.

That instinct ignores two binding constraints this series has proven.

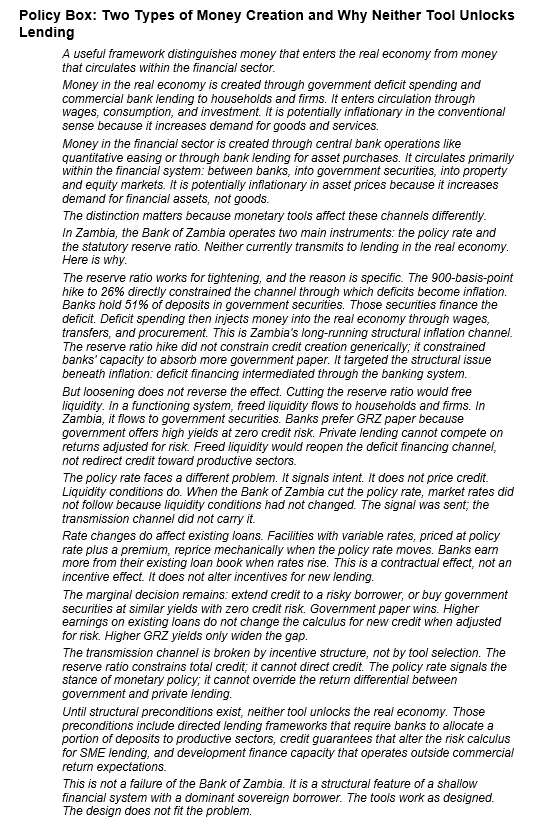

First, the domestic transmission engine is structurally impaired. Broad money is shallow; a large share of deposits and credit sits in foreign currency; and banks hold government securities at a scale that turns the system into a closed circuit. Commercial banks hold 21.6% of all government securities. Pension funds hold 29.1%. Genuine kwacha private credit sits at 7.4% of GDP. The policy rate cannot transmit through a balance sheet that does not carry broad-based kwacha intermediation.

Second, the global environment is no longer a neutral utility. Trade, finance, and technology are reorganising into tighter blocs. Ambiguity carries a cost. Voter sentiment increasingly aligns with survival instincts rather than ideology.

So, Part 4 makes one clean claim.

Zambia cannot treat monetary policy as a standalone lever. Zambia must treat it as one instrument inside a design problem: how to preserve sovereignty, protect affordability, and rebuild transmission in a world that rewards depth and punishes shallow systems.

The test throughout is sovereign dignity: does each intervention give Zambia a fair chance to price its own risk, protect its own data, add value to its own resources, and transmit its own policy signals to the real economy?

1. Executive Intent

This is not a Part 3 repeat.

Part 3 did the heavy lifting. It mapped the plumbing, showed the leak points, and made the core argument unavoidable: a policy rate cannot transmit through a balance sheet that does not carry broad-based kwacha intermediation.

Part 4 steps outward, then returns home.

It steps outward to show why the global regime now behaves like a strategic arena, not a passive backdrop. It returns home to show what discipline looks like when you accept that reality.

This part has three objectives.

First, reset the context. The global order is moving from integration to fragmentation. Capital flows are no longer only about returns; they are increasingly about alignment, access, and security.

Second, remove the false exits. Many policymakers assume we can escape constraint through slogans: dedollarise faster, borrow elsewhere, find a new tap, ride a new rail. Those exits fail because they substitute narrative for balance sheet reality.

Third, define the governing principle that closes the series.

Structure before sentiment means this: affordability does not come from decreeing a low price of money. Affordability comes from building a system where the price of money reaches households and firms without collapsing the banking base, the currency, or the sovereign funding curve.

2. The End of the Benign Global

For a long time, Zambia could treat the global economy as a neutral utility.

Sell copper. Borrow dollars. Absorb shocks. Repeat.

That era is ending.

The world is reorganising in ways that compress time and narrow options. Trade, finance, and technology are moving into closed regional systems. Countries are compelled to declare strategic allegiance. Ambiguity becomes costly. Elections and voter sentiment shift toward survival instincts rather than ideology.

This matters for Zambia because Zambia is not insulated from global architecture. Zambia lives inside it.

When settlement networks fragment, the cost of FX hedging changes. When technology access becomes conditional, the cost of building digital rails rises. When capital allocators start pricing alignment risk, frontier countries pay a premium even when their domestic numbers improve.

The global environment now behaves less like weather and more like terrain. Monetary policy is a terrain instrument. It works when the terrain is stable and the engine is deep. It fails when the terrain shifts quickly and the engine is shallow.

2.1 The Structural Power Framework

Susan Strange, the intellectual architect of structural power analysis in international political economy, distinguished between relational power and structural power. Relational power compels: A forces B to do something B would not otherwise do. Structural power shapes: it determines the framework within which actors operate. Strange identified four structures that matter: security, production, finance, and knowledge. Her central insight was that the most overlooked channel of power is financial access. One cannot comprehend how the world works without understanding who controls the mathematics of sovereign risk assessment.

For Zambia, this framework is not abstract. The country does not set the terms on which it borrows. It does not control the rating methodologies that determine its cost of capital. It does not own the data infrastructure that will price AI services and health partnerships. Disputing rating methodologies is insufficient. Sovereignty requires either shaping the methodology through institutional voice or building alternative frameworks that price African risk on African terms. That requires architecture, not argument. (For a deeper treatment of how Africa can own the math behind its risk premium, see ‘From Grievance to Design,’ Canary Compass, December 2025.)

2.2 The Cost of Ambiguity

Countries that defer structural choices face compounding costs. Each year of ambiguity widens the gap between what the domestic system can carry and what the global environment demands. Reserve buffers erode. Data flows outward. Conditionalities accumulate. The negotiating position weakens precisely when negotiation matters most.

The global regime now prices alignment risk explicitly. From semiconductor access to energy corridors to military deployments in contested regions, the assumption of neutral markets has collapsed. Zambia cannot remain neutral in a world where neutrality itself carries a premium.

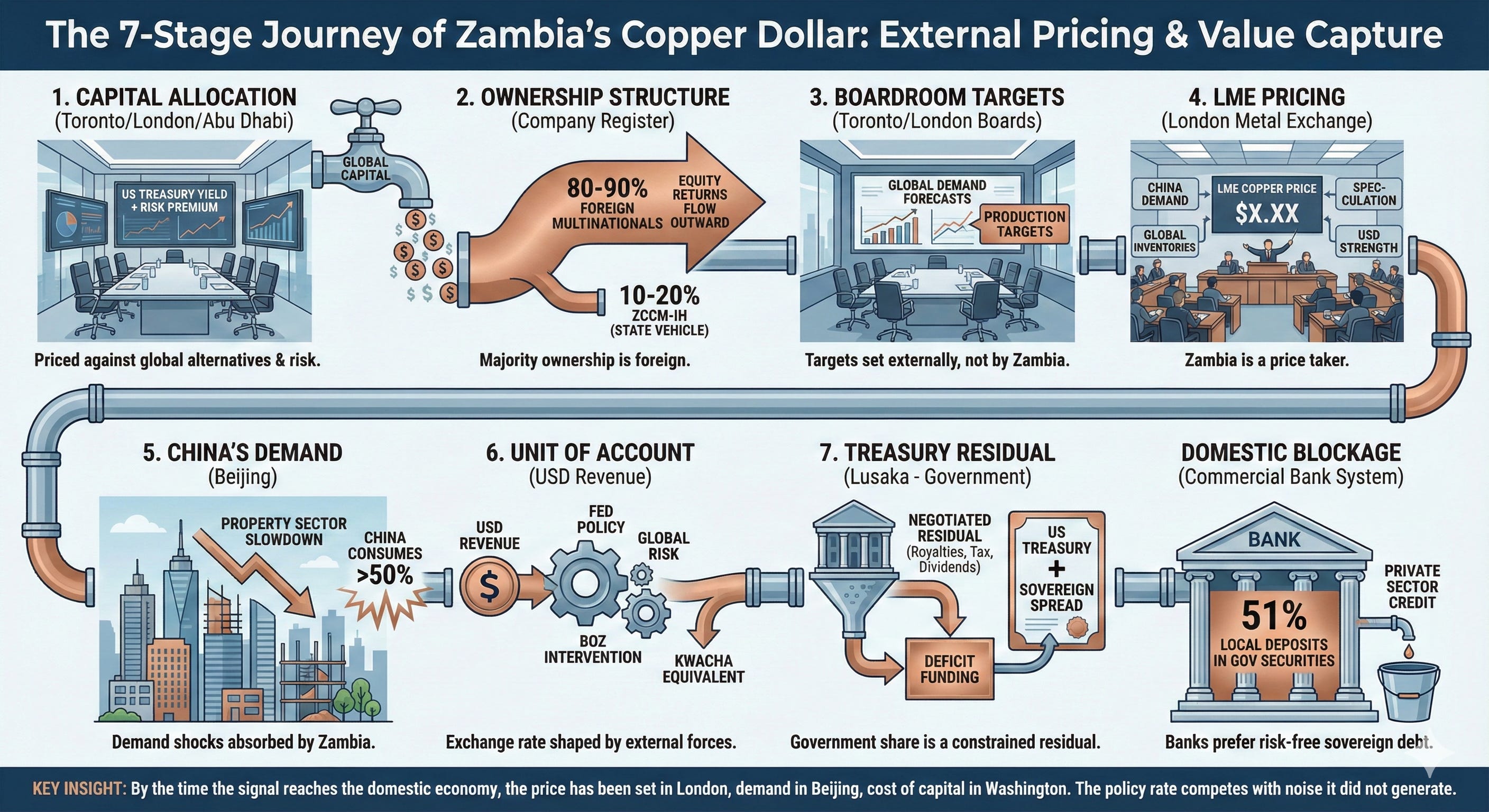

3. The Journey of Zambia’s Copper Dollar

Before the K100 enters a Zambian bank, it has already been priced seven times by forces Zambia does not control.

First, in Toronto, London, or Abu Dhabi. A foreign investor decides to allocate capital to Zambia’s copper sector. This decision is priced against alternatives: Chile, Peru, the DRC. The hurdle rate is set by the US Treasury curve plus an equity risk premium. Zambia competes for capital it does not own.

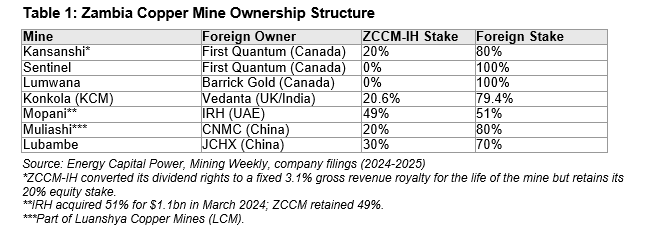

Second, on the company register. Foreign multinationals primarily hold 70% to 100% of Zambia’s major copper mines. ZCCM Investment Holdings, the state vehicle, retains 0% to 30%. The majority of equity returns flow outward.

Third, in the boardroom. Production targets are set by boards in Toronto and London, calibrated to global demand forecasts and company balance sheet needs. Zambia hosts extraction. It does not set production targets.

Fourth, on the London Metal Exchange. Copper is priced in London, not Lusaka. The price reflects Chinese construction demand, global inventory levels, speculative positioning, and the strength of the dollar. Zambia is a price taker.

Fifth, in Beijing. China consumes over half of global copper. When China’s property sector slows, copper demand falls and prices follow. Zambia absorbs the shock.

Sixth, in the unit of account. Export revenues arrive in US dollars. The kwacha equivalent depends on an exchange rate shaped by Federal Reserve policy, global risk appetite, and the Bank of Zambia’s intervention capacity.

Seventh, at the Treasury. The government’s share comprises royalties, corporate tax, and dividends on its minority stake; it is itself a negotiated residual, constrained by the threat of capital reallocation to jurisdictions offering better terms. What remains finances a fraction of the deficit. The rest requires bond issuance: external bonds priced against the US Treasury curve plus sovereign spread; domestic bonds placed into a banking system already saturated with sovereign paper.

Only now does the K100 enter the banking system. And here the domestic impairment begins. Commercial banks hold 51% of local currency deposits in government securities. The policy rate speaks, but the audience has already committed its balance sheet elsewhere.

This is structural power made operational. The policy rate is not weak because the central bank lacks credibility. It is weak because by the time the signal reaches the domestic economy, the price has already been set in London, the demand in Beijing, the cost of capital in Washington. Zambia’s monetary policy competes with noise it did not generate and cannot silence.

The sovereign dignity test asks whether each intervention gives Zambia a fair chance to price its own risk. The copper dollar’s journey shows where that chance is lost: not at one chokepoint, but at every stage from investment to transmission.

4. The Structural-Cyclical Distinction: Why It Matters Now

Mary Daly, President of the Federal Reserve Bank of San Francisco, offered a framework in November 2025 that deserves direct application to Zambia’s policy debate.

The economy, Daly argued, is being buffeted by both cyclical and secular forces. In real time, it can be hard to know which will have the larger impact. The example she gave was labour supply: immigration decline is a structural shift, while declining labour demand is cyclical. Only wages reveal the answer. If wages rise despite slower hiring, the structural constraint is binding. If wages soften, the cyclical slowdown dominates.

The implication is direct: if policy changes are structural, monetary policy cannot fix them.

For Zambia, this framework clarifies a hard truth. The transmission impairment is not cyclical. It is not a temporary disruption that will self-correct when global conditions ease. The shallow credit base, the sovereign-bank nexus, the foreign currency deposit share, the auction-anchored pricing of loans: these are structural features of the system. A rate cut does not alter them. Only institutional and market design can.

4.1 Structure Over Sentiment in the World’s Deepest Market

Governor Christopher Waller’s December 2025 remarks at the Yale CEO Summit revealed a striking insight even for the United States. He observed that the primary constraint on housing demand was not interest rates but employment security: “Everybody’s afraid for their jobs. I’m dead serious... The biggest reason people are not buying homes is that they’re worried about losing their jobs. It’s not about interest rates.”

If this is true in the world’s deepest capital market, with its transparent pricing and sophisticated transmission mechanisms, how much more does it apply to Zambia? When confidence is broken, the rate channel cannot fix the real problem. Rate cuts that leave bank balance sheets concentrated in government securities do not automatically produce credit expansion to households and firms. The signal speaks. The system does not respond.

5. The Nonmonetary Era: When the Policy Rate Stops Being the Main Character

The clean textbook story says the central bank moves the policy rate, the money market follows, banks reprice loans and deposits, demand cools, inflation comes down, and the currency stabilises. That story still matters, but it no longer runs the world on its own.

In the current cycle, some of the most powerful forces shaping inflation, growth, and financial conditions sit outside the policy rate. Fiscal posture, tariffs and trade restrictions, migration and labour supply, regulation, and the credibility of institutions now move outcomes as much as, and sometimes more than, the level of the policy rate.

Michelle Bowman, a Federal Reserve Governor, made a related point in September 2025: tariff-related price increases are likely a one-time effect, and the appropriate response is to look through temporary inflation readings rather than tighten mechanically. This matters because it shows even the Federal Reserve distinguishing between price level shifts and persistent inflation dynamics.

For a small, open, commodity-exposed economy, this is the trap: global decisions move the price of capital, the price of fuel, the price of food, and the value of the dollar, and we inherit the downstream conditions. We can be disciplined, or we can be loud. The global system rewards discipline.

6. The Global Rebalancing: Why Neither Pole Offers Friction-Free Partnership

Michael Pettis has described a model that shaped the last two decades of global growth: China suppresses domestic consumption to subsidise manufacturing; the United States runs massive deficits to absorb that excess supply.

That model has reached its limit.

Brad Setser of the Council on Foreign Relations quantified this in December 2025: China has been growing via net exports since its property bubble burst in mid-2021. Net exports contributed more than one percentage point to annual growth and may now be the main driver. China runs a customs trade surplus approaching $1 trillion against almost everyone except Middle East oil exporters. China’s manufacturing surplus has grown to approximately 10% of its GDP.

China’s policy response has not yet produced a durable rebalancing toward consumption. The December 2025 stimulus package focuses on expanding personal consumer lending, channelling credit toward green, health, and digital sectors, and boosting service sector spending. But consumer confidence remains weak, and the measures operate at the margin rather than altering the export-dependent structure of growth.

6.1 The China Consumption Problem

We have heard of a China market for African goods for years. In reality, where is this market?

China has weak consumer demand and that means weak import demand. China also faces demographic pressures and elevated youth unemployment. A surplus economy absorbs rather than emits liquidity. This is the inverse of the Triffin constraint that historically governed the dollar’s reserve role.

As a result, the yuan does not circulate organically. China runs persistent trade surpluses, restricts capital account openness, and offers limited depth in safe domestic assets, so trading partners do not accumulate yuan through trade in the way the world accumulated dollars.

China therefore relies on swaps and directed lending to place yuan offshore. The oil-yuan-gold corridor that some envision will take considerable time. Meaningful internationalisation would require China to deepen its financial markets substantially and accept the capital account openness that reserve currency status demands.

For African economies hoping to export to China, this poses a fundamental constraint. Where is the Chinese market for African goods? China runs trade surpluses against almost everyone except Middle Eastern oil exporters. Without sustained domestic consumption growth, it cannot absorb African exports at scale. The Belt and Road financing model works largely in one direction: infrastructure loans flow out, commodity repayments flow back. It does not create diversified trade relationships. This is not partnership. It is extraction with infrastructure.

6.2 The Hamiltonian Frame: Why China Is Not Cheating

China demonstrated long ago that dominance cannot be sustained without treating corporate alignment as a national strategic instrument of sovereignty. Once supply chains, capital formation, and technology became instruments of state power, the assumption of neutral free markets collapsed.

The fault line is not ideology but mechanism. In the East, alignment is enforced directly. In the West, it is achieved by reshaping incentives and constraints. Different tools, same outcome. When strategic sectors are defined, corporate autonomy becomes conditional, not absolute. Free markets cannot survive asymmetric rules indefinitely.

China is not cheating. They are executing a known playbook. Alexander Hamilton’s framework of sovereign capital formation: infant industry protection, directed credit, state-backed balance sheets, tariff walls, procurement discipline, capital controls, forced technology transfer. The United States used it. Germany used it. Japan used it. South Korea used it. China used it. At scale.

The difference is discipline and coherence, not morality.

China uses Hamiltonian tools for itself. Africa often uses China’s capital against itself. China protects domestic industry, exports overcapacity, uses foreign markets to absorb surplus, and forces learning before liberalising. Many African states open markets prematurely, import finished goods, kill local industry, finance visibility projects, and avoid tariffs for political convenience.

Same tools available. Radically different outcomes. That is not the global system’s fault.

China did not beat anyone at their own game. They simply had the courage to play it properly and for themselves. The tragedy is not that Africa lacks options. It is that we keep choosing comfort over coherence.

6.3 The US Pole: Transactional Alignment as Strategic Fit

For Zambia, neither pole offers friction-free partnership. The question is not ‘who is good’ but ‘who offers more negotiating space and faster development velocity.’

The United States approaches Africa through a lens of transactionalism: security cooperation and market access in exchange for alignment on critical minerals, data flows, and exclusion of strategic competitors. China offers infrastructure financing and market access but with conditions that often entrench consumption dependence rather than building industrial capacity.

From a purely transactional framework, US alignment offers several advantages. First, US capital markets offer depth that no alternative matches. The Treasury market trades over $20 trillion monthly (SIFMA, November 2025). That depth creates liquidity options unavailable elsewhere. Second, the Lobito Corridor and critical minerals partnerships offer infrastructure investment tied to value chain participation, not just extraction. Third, dollar-denominated trade allows hedging instruments, secondary market liquidity, and benchmark pricing that yuan-denominated alternatives cannot yet replicate.

This transactional preference does not ignore troubling developments. It acknowledges them while maintaining strategic coherence.

7. The Sovereignty Warning: Data, Health, and the New Extraction

The colonial extraction model focused on physical commodities: copper, cobalt, agricultural products. The emerging extraction model targets intangibles: health data, genomic information, agricultural patterns, financial behaviour. These assets compound in value as artificial intelligence systems require ever-larger training datasets.

7.1 Kenya: The Canary in the Data Mine

In early December 2025, Kenya signed a bilateral health agreement with the United States committing approximately $1.6 billion in US investment over five years in exchange for $850 million in additional Kenyan domestic health expenditure over the same period. The deal, part of the ‘America First Global Health Strategy’ launched in September 2025, replaces NGO-mediated funding with direct government-to-government arrangements.

Trump sold the death of USAID as austerity. The new health compacts with African capitals reveal something else: a redistribution of power, not a retreat. Washington signed a 5-year agreement; Kenya must absorb more than 13,000 donor-funded health workers onto its own wage bill by 2028, take full responsibility for key health commodities by 2031, and raise domestic health spending in lockstep. This is not charity. It is a balance sheet swap that trades short-term dollar inflows for long-term fiscal obligations.

The real innovation is not the money. It is the data. The original US template required a 25-year pathogen and specimen sharing commitment. Kenya negotiated this down to a seven-year data sharing agreement covering only aggregated, de-identified data. Kenya refused to sign the specimen sharing agreement entirely. Paragraph 8 requires all specimen testing and pathogen data exchange to comply with Kenyan law. Paragraph 15 establishes that separate data sharing and specimen testing agreements will be negotiated later.

Within a week, Kenya’s High Court suspended the data-sharing provisions. Judge Bahati Mwamuye issued a conservatory order on December 11, 2025, blocking the ‘transfer, sharing or dissemination of medical, epidemiological or sensitive personal health data’ pending a February 2026 hearing. The petitioners, including the Consumers Federation of Kenya and Senator Okiya Omtatah, cited concerns about pathogen sharing, intellectual property ownership on vaccines developed from Kenyan samples, and the absence of transparency in the agreement’s full terms.

The lesson is temporal: establish data sovereignty legislation before signing health, AI, or digital infrastructure agreements. Retrofitting protections after deals are signed is legally complex and diplomatically costly. Kenya had the Digital Health Act of 2023 and the Data Protection Act of 2019 in place. These laws gave it negotiating leverage. Countries without such frameworks accept terms they cannot later contest.

7.2 Zambia: Health Funding and Mining Conditionality

On December 11, 2025, the day the Zambia-US health agreement was scheduled to be signed, the date was abruptly scrapped. Instead, Caleb Orr, the US Assistant Secretary of State for Economic, Energy, and Business Affairs, travelled to Zambia, met with President Hakainde Hichilema, and announced that economic cooperation supersedes and is a pre-requisite for health funding.

The State Department announced that Orr and President Hichilema had ‘committed to a plan that aims to unlock a substantial grant package of US support in exchange for collaboration in the mining sector and clear business sector reforms.’ The $1.5 billion health package now depends on terms set for mining cooperation.

December 11th, 2025, marks the moment the curtain fully rose on the 21st-century scramble for Africa. Access to the region’s natural resources and markets is central to America’s geopolitical ambitions and supersedes every other consideration that has historically motivated health foreign aid.

7.3 The 15% Rejection: Sovereignty Under Constraint

In November 2025, Zambia’s Presidency rejected a draft change to mining regulations that would have raised state participation to a minimum 15% in copper and other critical mineral mines, with provisions that contemplated a path toward a higher effective stake, including figures discussed up to 40%, funded through dividend forfeitures and tax concessions rather than upfront cash.

This was not external pressure. This was the Presidency overruling its own ministry’s draft. Jito Kayumba, President Hichilema’s Special Assistant for Finance and Investment, stated: “From the view of the presidency, it’s not something that will be brought to fruition, because we do not support it.”

Read the signal with discipline. This episode does not prove Zambia held leverage. It proves Zambia recognised constraint.

The reporting around the draft made the macro trade-off clear. The proposal risked disrupting roughly $10 billion in planned mining investment tied to copper expansion. In that context, a sudden shift in ownership terms would have conflicted with the administration’s strategy of protecting investor confidence and accelerating production growth.

The sovereignty lesson is not that Zambia should stop pursuing value. The sovereignty lesson is that Zambia must choose instruments it can enforce without triggering capital rationing.

That is why the credible negotiating space sits less in headline ownership jumps and more in sequenced, enforceable levers: local content rules, supplier development, processing incentives, infrastructure trade-offs, and contractually defined technology transfer that is priced into projects from the start.

Zambia earns bargaining power before it demands it.

8. The Tenor Trap: Liquidity-Constrained Systems Cannot Pretend to Be Long-Term

The most dangerous lie in a shallow system is the fantasy of long-term pricing without long-term balance sheets.

The Kiel Institute’s African Debt Database separates two regimes. Some countries behave like market builders: they invest in local market infrastructure, manage duration risk deliberately, and foster stable domestic investor bases. Others behave like liquidity-constrained borrowers: they turn to domestic borrowing reactively when external financing tightens, and they remain concentrated in short-term instruments because they cannot extend maturities without paying crisis prices.

OECD data shows low-income countries average 3-5 years weighted term to maturity, compared to 7+ years for upper-middle-income countries and 8+ years for OECD members. Every rollover is a repricing event. Every repricing event transmits external volatility directly into domestic fiscal conditions.

If the sovereign and the banking system fund themselves short, they will price the economy short. That is not a preference. It is arithmetic. A short funding base produces rollover risk. Rollover risk produces a term premium. A high term premium kills mortgages, long project finance, and patient capital.

The core instruction becomes simple: earn the right to lend long.

9. The Digital Rail: Stablecoins as Competitor and Opportunity

Stablecoins are not a niche sideshow. According to IMF data, USD-denominated stablecoins represent over 97% of outstanding stablecoin value. On-chain payment and transaction tracking shows that USD stablecoins also dominate usage, approaching near-universal share in active flows. Their reserve assets sit heavily in short-term US Treasuries.

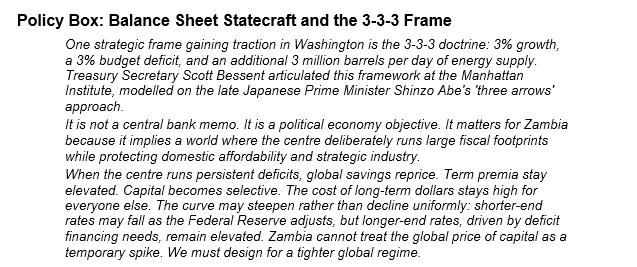

Treasury Secretary Scott Bessent stated that stablecoins could unlock $2 trillion in demand for US Treasury bills. This is not hyperbole; it reflects a strategic vision. Stablecoins are digital liquidity rails for the US government that corporations will build, users will adopt, and Treasury will benefit from. Every widely used stablecoin is ultimately an investment in the sovereign credit of the United States.

As Eswar Prasad noted in IMF Finance & Development in December 2025, stablecoins pose an existential threat to the currencies of smaller economies. People in some corners of the developing world are likely to trust stablecoins issued by well-known companies more than local currencies that have suffered from high inflation and volatile exchange rates.

For Zambia, the practical message is direct: if we do not make the kwacha system useful and liquid, the public will import utility through digital rails. Regulators who treat this as only a consumer protection issue will misread the direction of travel.

9.1 The Regulatory Response: Dedollarisation with International Access

The goal is not to ban stablecoins. The goal is to enforce dedollarisation domestically while allowing international use.

Will Zambians use stablecoins to settle domestic transactions? That is the first question. The answer must be no, through regulatory design. We do not mind USD use for international transactions, but locally, transactions must settle in kwacha.

In October 2025, Flutterwave partnered with Polygon to deploy stablecoin payments across 34 African countries. The design is instructive: they work with regulators rather than around them, enforce strict KYC and KYB requirements, start with verified merchants, and use stablecoins for cross-border settlements while respecting local currency for domestic transactions. Chainalysis estimates such rails are 60% cheaper than traditional remittances.

Zambia could follow this model: partner with compliant platforms, enforce KYC through agreements with crypto and remittance companies for data sharing, allow stablecoins for international remittances while enforcing kwacha for domestic settlement.

The Bank of Zambia has drafted a framework for crypto assets and stablecoins, set for stakeholder review. The ZIPSS payment system transitioned to ISO 20022 messaging standard on October 14, 2023, the first central bank to use the Swift ISO Accelerator Pack. The BoZ 2024 Annual Report shows ZIPSS processed 73.5% more transactions in 2024. The infrastructure exists. The regulatory posture determines whether digital rails strengthen or bypass kwacha utility.

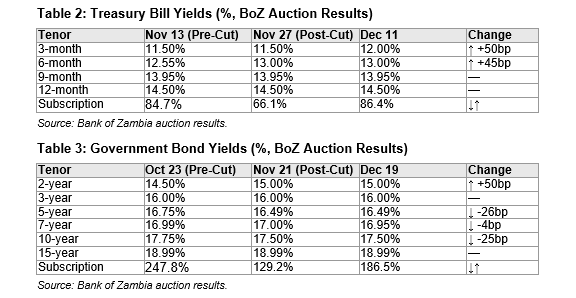

10. Post-Decision Snapshot: What the November 2025 Cut Actually Produced

On November 19, 2025, the Bank of Zambia’s Monetary Policy Committee reduced the policy rate by 25 basis points to 14.25%. The series has argued that structure matters more than sentiment. That rate decisions change signals, but not the underlying architecture that determines whether signals transmit. The post-decision data allows us to test this proposition.

10.1 What the Data Shows

The 25-basis point policy rate cut did not produce uniform yield declines. Short-end Treasury bill rates actually rose: the 3-month increased 50 basis points to 12.00%, while the 6-month rose 45 basis points immediately post-cut. The 12-month T-bill yield remained anchored at 14.50% throughout. The first post-cut T-bill auction was undersubscribed at 66.1%.

In the bond market, the 2-year yield rose 50 basis points to 15.00%, opposite of rate cut expectations. The middle of the curve compressed slightly: 5-year fell 26 basis points, 10-year fell 25 basis points. The long end remained anchored with the 15-year unchanged at 18.99%.

This is precisely what ‘structure before sentiment’ predicts. Rate cuts change the policy signal but not the underlying liquidity conditions or balance sheet constraints that determine market-clearing yields. The real story of pre-cut to post-cut was not the rate decision but the fluctuation in subscription rates—a function of liquidity conditions, not monetary stance. The transmission mechanism remains impaired regardless of where the policy rate sits.

11. Who Holds the Sovereign: The Investor Base Challenge

Understanding the current holder structure clarifies the design problem.

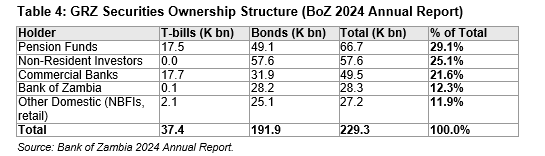

At year-end 2024, Zambia’s government securities totalled K229.3 billion. The ownership structure reveals both concentration and opportunity.

Several features stand confirming the design problem.

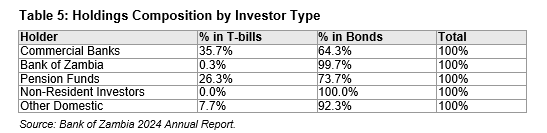

Pension funds are the largest holders by total stock at 29.1%, not commercial banks. This is patient capital with duration-matching needs that naturally align with longer-dated instruments and a more stable curve.

Non-resident investors sit entirely in bonds, with zero exposure to Treasury bills, and they own approximately 30% of outstanding GRZ bonds. Their participation reflects a long-standing preference for duration when compensation is sufficiently high. Zambia saw large inflows during 2020–2021 when local-currency bond yields exceeded 33%, followed by renewed interest after the 2021 election and further improvement as the debt-restructuring process advanced. When roughly one-third of the bond market sits with non-residents, the long end is materially shaped by external risk pricing, not only by domestic liquidity.

Commercial banks dominate the short end. They hold 47.3% of Treasury bills but only 16.6% of bonds, consistent with liquidity preference and regulatory treatment rather than duration appetite. This is why the policy signal weakens beyond the front end: banks anchor the bill curve, not the term curve.

The retail investor base remains thin. The “Other Domestic” category at 11.9% is not retail-only; it includes insurance companies, non-bank financial institutions, corporates, SACCOs, and retail individuals, with retail not separately disclosed. Global benchmarks place retail-only participation at roughly 1–5% in comparable markets. Japanese households hold about 1.3% of JGBs, and Kenya’s retail participation was around 2% prior to M-Akiba. The DMO retail bond programme is explicitly designed to expand this slice and make the investor base stickier.

The policy relevance is direct. With material non-resident ownership of bonds, large maturity walls can translate into FX pressure if exits are disorderly or rollovers fail. That is why benchmark building, switch auctions, and liability-management operations are not optional plumbing. They are sovereign risk management.

The sovereign-bank nexus is not abstract. Commercial banks hold government securities equivalent to 51% of their local currency deposits. This is the transmission bottleneck: deposits flow into banks, banks allocate to government securities, and the policy rate speaks to an audience that is already committed elsewhere.

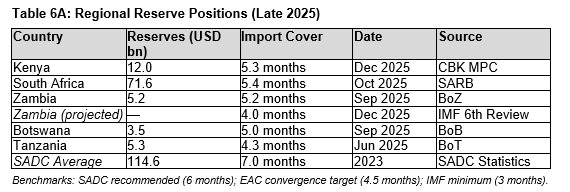

12. The Reserve Anchor: Position and Trajectory

Gross international reserves stood at approximately $5.2 billion as at September 2025, equivalent to roughly five months of import cover at that date.

The IMF’s December 2025 press release (PR/25/431) on the sixth and final ECF review projects approximately four months of prospective import cover by year-end.

The arithmetic matters: import cover is calculated on a rolling average of imports. The year-end denominator will be higher due to increased imports as the economy normalises post-drought, hence lower months despite similar dollar reserves. This is not deterioration. It is normalisation of the import base.

The sixth review of the IMF’s Extended Credit Facility remains on track. Total disbursements since August 2022 will reach approximately $1.7 billion. As Finance Minister Situmbeko Musokotwane stated: ‘This agreement is not just a technical milestone with the IMF. It is confirmation that the difficult reforms undertaken by the Zambian people are working.’

Zambia’s projected four months of prospective import cover by the end of 2025 marks progress from earlier lows, but the buffer remains thin for a commodity-dependent economy exposed to external shocks. The IMF’s Sixth Review press release puts the constraint plainly. Despite higher international copper prices, the current account deficit is projected to widen to about 2.1% of GDP in 2025, driven by import growth across categories and lower official grants, even as gross international reserves are expected to reach four months of prospective imports.

That combination is not a contradiction. Zambia earns significant foreign exchange through mining exports and taxes paid in foreign currency and channelled through the Bank of Zambia. These inflows are regularly sold into the domestic market. But they are insufficient to offset total demand, and the balance of payments remains in deficit. Reserve rebuilding is occurring mechanically, not inside a surplus environment. This is why the IMF urges the Bank of Zambia to scale up net international reserve accumulation by taking advantage of periods when supply conditions are stronger, and the central bank can purchase reserves without forcing disruptive exchange rate moves. Four months is a buffer under construction, not a buffer completed.

Kenya’s higher headline cover, at 5.3 months, reflects a broader mix of inflow channels and deeper access to external financing, but it too operates under rollover constraints highlighted in IMF surveillance. The shared lesson is structural: headline import cover does not equate to surplus foreign exchange or discretionary policy space. Inflows support functioning from one day to the next; reserve stocks constrain policy over time. Reserve adequacy is therefore not only about the level of buffers, but about their usability, their durability, and their freedom from encumbrance.

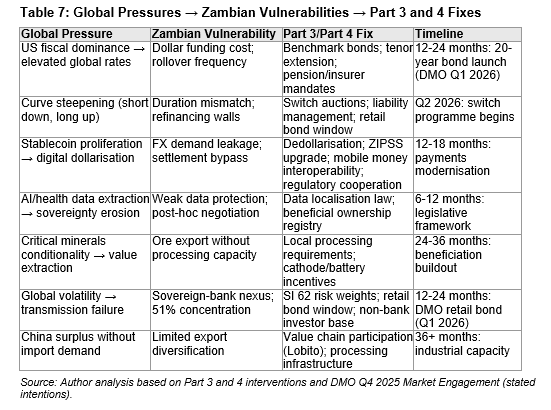

13. The Bridge: Global Pressure to Domestic Fix

Part 3 established the eight structural chokepoints. Part 4 has shown the global pressures. The bridge connects them: for each external constraint, there is a domestic design response.

This bridge is not theoretical. The Ministry of Finance’s Q4 2025 DMO Market Engagement confirms that the government is already moving on several fronts: a 20-year benchmark bond launching January 2026 with target critical mass of K10 billion, a retail bond with monthly coupons priced off the 15-year benchmark with initial target of K100 million, and a liability management programme beginning Q2 2026 with switches and buybacks. The state is thinking in curve language. Part 4 provides the global context for why this matters now.

14. What If Copper Rides High?

A reasonable counterargument: copper prices are projected to remain elevated for the next decade. Should Zambia not simply ride the commodity cycle and defer structural reform?

The answer is no, for three reasons.

1. First, high copper prices do not fix transmission. They increase FX receipts, strengthen reserves, and ease the fiscal position. They do not change the fact that 51% of local currency deposits sit in government securities or that genuine kwacha private credit is 7.4% of GDP. Windfall revenues that flow through a broken transmission mechanism do not reach households and firms as affordable credit.

2. Second, commodity windfalls create complacency. The history of resource-dependent economies shows that reform windows close when prices are high. The discipline required to build domestic funding depth, extend tenor, and diversify the investor base becomes harder to sustain when dollar inflows paper over structural weaknesses.

3. Third, high prices are precisely when value addition is most negotiable. Zambia’s leverage over mining partners increases when copper is scarce and valuable. Waiting for prices to decline before demanding local processing and beneficiation surrenders the best negotiating position.

The windfall should be used to build, not to defer building.

15. The Discipline of Design: The Bridge to Tenor

Zambia does not have a rate problem first. Zambia has a time problem.

The overnight market can behave, the corridor can hold, and liquidity can look stable in the aggregates. Then you look up and realise the real economy still prices credit off 91-day, 182-day, and 364-day Treasury bills, not off the policy stance. Transmission works at the front end, then collapses beyond three months because the sovereign curve becomes the anchor.

15.1 Pillar One: Diversify the investor base with sticky retail capital

Part 3 identified the most practical lever: a digitised retail bond window, accessible via mobile money, integrated into the Central Securities Depository. Two design points are not optional. First, the minimum ticket must drop below K1,000 so ordinary households can participate. Second, the portal must integrate fully into mobile channels and agent networks. Retail capital is sticky. It does not vanish because an auction cleared badly.

15.2 Pillar Two: Rebuild benchmark discipline and consolidate the curve

Define a small set of benchmark maturities. Reopen them until they reach credible size. Then run switch auctions that invite holders of illiquid legacy lines into benchmark lines. That single move reduces fragmentation, builds depth at key points on the curve, and smooths redemption walls by changing the timing of cash flows through voluntary exchanges.

15.3 Pillar Three: Fix interbank segmentation, then build a term money market

A corridor cannot transmit if liquidity does not circulate across tiers of the banking system. Tradeclear and the Umbrella Guarantee Facility are designed to break interbank segmentation by guaranteeing counterparty credit risk for eligible interbank trades. Then comes the term structure: extend the central bank footprint beyond overnight into a predictable term repo framework, with regular auctions at 7-day, 30-day, 90-day, and 180-day tenors.

15.4 Pillar Four: Use buffers as shock absorbers

Link the release of capital buffers to private-sector credit extension targets, and penalise banks that keep expanding sovereign exposure while ignoring private credit. Buffers exist so they can be released in stress to support continued credit provision.

16. Sovereign Dignity 2035: The Scorecard

Zambia does not need a prettier argument. Zambia needs a scoreboard.

If we cannot define success in measurable terms, we will keep cycling between the same debates every tightening cycle. This scorecard defines direction, not perfection. Each metric is defensible, measurable, and within Zambia’s control to influence.

The test throughout is sovereign dignity: does each intervention give Zambia a fair chance to price its own risk, protect its own data, add value to its own resources, and transmit its own policy signals to the real economy?

Economic dignity at the household level requires sovereign dignity at the national level. A system that cannot price its own risk cannot offer fair terms to its own citizens. A nation subject to external data extraction cannot protect the information assets of its firms. A country that exports ore without processing cannot build the industrial base that creates jobs. And a central bank whose signal does not transmit cannot deliver the stability that households need to plan.

17. What This Series Was Really About

This series never tried to make the Bank of Zambia look heroic or foolish. That is not the point.

The point is to say out loud what many people feel but cannot formalise.

The policy rate is not magic. It is a signal. Signals only matter when markets can hear them.

Part 1 showed the CPI level gap: the accumulated purchasing power loss of 30-38% since 2019 that month-on-month improvements cannot erase.

Part 2 showed the money supply structure: M3 as an exchange-rate-driven aggregate, foreign currency deposits at 44% of broad money, and genuine kwacha private credit at 7.4% of GDP.

Part 2.75 showed the sovereign-bank nexus: government securities at 51% of local currency deposits, and how the banking system became a closed circuit for sovereign funding.

Part 3 showed the eight structural chokepoints and their three-phase sequencing: stabilise liquidity first, deepen markets second, lengthen tenor third.

Part 4 placed the domestic architecture inside the global environment. The conclusion is not dramatic. It is quiet.

Zambia earns the right to ease, and to fund affordability, only after it has built a system that can carry that easing into real credit without destabilising the currency, the curve, or the banks.

Sentiment is cheap. Design is expensive.

But only design survives the squeeze.

— End of Series —

Sources and References

Primary Data Sources

• Bank of Zambia 2024 Annual Report (GRZ securities ownership data)

• Bank of Zambia Monetary Policy Statement, November 2025

• Bank of Zambia Auction Results, November-December 2025

• IMF Extended Credit Facility Review (PR/25/431, December 2025)

• Zambia Ministry of Finance DMO Q4 2025 Market Engagement (stated intentions)

Federal Reserve and Central Bank Sources

• Mary Daly, ‘Policymaking Amid Change’, Federal Reserve Bank of San Francisco, November 2025

• Christopher Waller, Remarks at Yale CEO Summit, December 2025

• Michelle Bowman, ‘Thoughts on Monetary Policy Decisionmaking’, Federal Reserve, September 2025

• Stephen Miran, Address at BCVC Summit, Harvard Club of New York, November 2025

• Scott Bessent, Remarks at Manhattan Institute (3-3-3 doctrine)

Canary Compass Series

• Dean Onyambu, ‘From Grievance to Design: Why Africa Must Own the Math Behind its Risk Premium,’ Canary Compass, December 2025

Global Analysis

• Brad Setser, ‘Can China Continue to Export its Way Out of its Property Slump?’, Council on Foreign Relations, December 2025

• Michael Pettis, Carnegie Endowment for International Peace (global rebalancing framework)

• Susan Strange, States and Markets (structural power framework)

• Eswar Prasad, ‘The Stablecoin Paradox’, IMF Finance & Development, December 2025

• Kiel Institute African Debt Database (tenor structure analysis)

• OECD Global Debt Report 2025, Chapter 3 (Sovereign Debt Markets in EMDEs)

Market and Technology

• Flutterwave-Polygon partnership announcement, CoinDesk, October 2025

• SWIFT News, Bank of Zambia ZIPSS ISO 20022 migration, October 14, 2023

• Chainalysis 2024 (remittance cost comparisons)

• FSD Kenya M-Akiba case study (retail investor benchmarks)

• Energy Capital Power, ‘7 Largest Copper Mines in Zambia’, May 2024

• Mining Weekly, company filings (mine ownership data)

US-Africa Policy

• Emily Bass, ‘US Delays Zambia Health Agreement’, Substack, December 2025

• EATG, ‘US Delays Zambia Health Agreement as Signing Becomes Contingent on Mining Deal’, December 2025

• Bloomberg, ‘Zambian Presidency Shuns Plan to Give State Free Stake in Mines’, November 26, 2025

• Miningmx, ‘Hichilema Rejects Shake-up of Mining Regulations’, November 2025

• US Department of State, Kenya Health Cooperation Framework, December 2025

• Kenya High Court, Judge Bahati Mwamuye conservatory order, December 11, 2025

Disclaimer

This article does not constitute legal, financial, or investment advice. The author shares views for perspective and discussion only. Do not rely on them as a substitute for professional advice tailored to your specific circumstances. Always consult a qualified legal, financial, investment, or other professional adviser before making decisions based on this content. The analysis reflects proprietary research undertaken by Canary Compass and the author.

Canary Compass and the author accept no liability for actions taken or not taken based on the information in this article.

About the Author

Dean N. Onyambu is the Founder and Chief Editor of Canary Compass. His insights draw on experience across trading, fund leadership, governance, and economic policy.

The Canary Compass Channel is available on @CanaryCompassWhatsApp for economic and financial market updates on the go.

Canary Compass is also available on Facebook: @CanaryCompassFacebook.

For more insights from Dean, you can follow him on LinkedIn @DeanNOnyambu, X @InfinitelyDean, or Facebook @DeanNathanielOnyambu