Zambia Monetary Policy: Structure Before Sentiment. Part 2: Money Base and Credit

Why Easing Will Struggle to Transmit

Editor’s Note (December 5, 2025): Following clarifications from the Bank of Zambia on how foreign currency loans are reported in kwacha-denominated returns, some figures in this article have been refined. Part 2.75 of this series documents the corrections and provides updated analysis. The directional findings and core thesis remain unchanged. [Link to Part 2.75]

All charts are compiled from Bank of Zambia data and author calculations.

0. A Cut into Structural Fragility

On 12 November, the Bank of Zambia reduced the policy rate by 25 basis points to 14.25%. The move changes the level of the rate, but it does not change the architecture that governs liquidity, credit allocation, and transmission. It confirms the argument in Part One. Structure still dominates the system. Transmission remains weak. Dollarisation shapes behaviour. Intermediation is shallow. Pricing remains opaque. The cut enters an economy that cannot carry its intended effect.

Headline inflation has eased but remains above the 6-8% target band. The external position remains fragile. As the IMF noted in August, the central bank sold about $230 million in the first quarter of 2025 against a programmed allowance of $79 million, a gap that signals structural fragility rather than comfort.

Zambia displays a structurally K-shaped household economy and a four-track credit economy. A small formal segment accesses credit. A larger formal segment earns income but has no access to formal credit. The informal sector carries unstable income and the harshest inflation burden. A separate informal credit ecosystem sits outside monetary policy. One policy rate. Four different outcomes.

Under these conditions, a policy rate cut speaks loudly to the small formal minority that already borrows from banks and very softly, if at all, to the majority. Four in five workers operate in the informal economy, and most have no access to bank credit at any price. Lower inflation only means slower price increases. It does not ease the real cost of living for those outside the formal channel. Monetary signals reach only the part of the economy that sits on bank balance sheets.

The IMF staff were clear in their assessment. They noted that the central bank raised the policy rate by 300 basis points in 2024 and by 50 basis points in early 2025 to contain inflation, and that the real policy rate, at the time, remained negative. In their view, a gradual, data-driven move to a positive real policy rate would still be necessary to anchor expectations and return inflation to the target band by 2026. Easing before that convergence runs ahead of the prescribed path, placing greater pressure on credibility, particularly given the length of time headline inflation has persisted above the target band.

The core question is no longer whether the MPC should cut. The real question is whether a cut can move through a shallow, dollar-dominated, sovereign-heavy system and reach households, small businesses, and productive firms. This article answers that directly. It shows that the money base is too small, the deposit structure too fragile, and the credit system operates with wide opaque margins and is also material enough in government securities to prevent easing from delivering broad relief. The recent rate cut changes the optics. It does not repair transmission. In a system funded by short-term deposits that support longer-term variable-rate loans, price stability and structural reform matter more than cosmetic relief.

Part One showed why cutting into these conditions risks renewed pressure on the currency and a slower return to the target band. Part Two explains why the cut will struggle to deliver broad relief. Transmission remains impaired. Easing into this architecture shifts the benefit onto those with the least vulnerability, leaving the majority unchanged. Monetary policy will struggle to deliver broad impact until the country strengthens transmission. That work begins with the structure of money, liquidity, and credit. These foundations decide who hears the policy signal and who remains outside its reach.

1. The MPC Decision in Structural Context

The Monetary Policy Committee reduced the policy rate from 14.5% to 14.25%. On the surface, the move signals confidence in stabilisation and a desire to ease pressure on lending rates. In practice, it lowers the headline price of money in a system where the deeper structure still blocks transmission.

Bank of Zambia’s 2025 credit and business conditions surveys, along with private conversations with practitioners, confirm this disconnect. Banks cite weak household credit demand, cautious corporate borrowing, tighter collateral requirements, and persistent concerns about income volatility. These assessments remained unchanged even as the MPC reduced the policy rate, signalling that the move shifted the stance but will likely not shift expected behaviour.

Bank balance sheets rest on a shallow, foreign-currency-heavy deposit base. Liquidity shifts with valuation effects when the exchange rate moves rather than with the policy stance. Treasury bills and government bonds absorb a large share of bank assets and set a floor under lending rates. Deposit pricing typically follows liquidity conditions and bill auctions rather than the policy rate. Credit models remain conservative, especially for households and small- and medium-sized firms. Under this architecture, a small cut does not change the channels through which money flows. It changes the signal, but it rarely changes who receives it.

The rest of this article examines those channels in detail. Section 2 turns to the structure of the money supply, liquidity and credit. It shows how broad money has become an exchange-rate-driven aggregate and why shallow money depth prevents the policy rate from shifting credit volumes. Sections 2.3-2.7 analyse credit allocation, deposit pricing, lending rates, the sovereign nexus, and foreign currency dynamics. Section 2.8 consolidates the structural constraints. The conclusion explains why easing under current conditions risks slower disinflation and why structure must come before sentiment if monetary policy is to work for the majority.

2. Money Supply, Liquidity and Credit

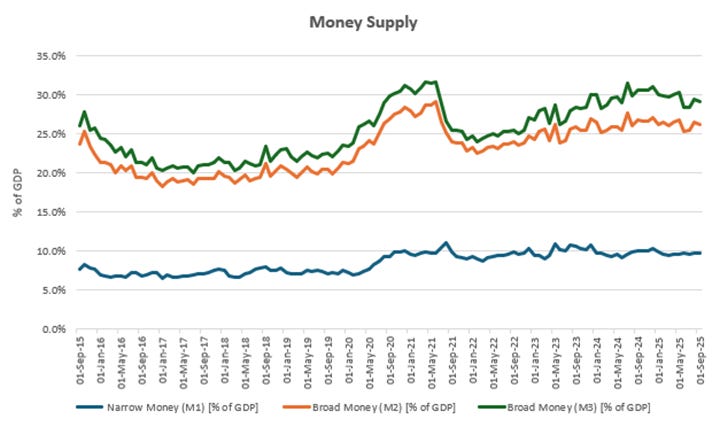

2.1 M1, M2, M3 Structure

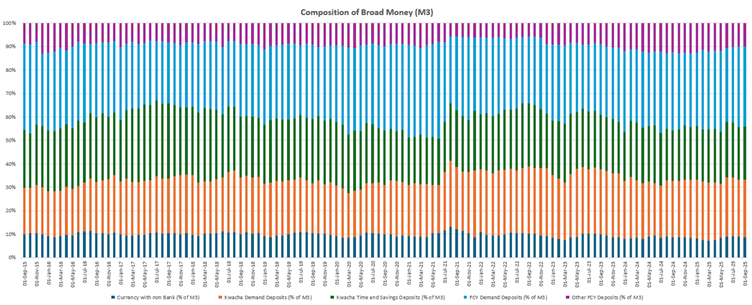

M1, M2, and M3 track the liquidity that supports payments, savings, and credit, but in Zambia, these aggregates do not behave like traditional monetary layers. M1 captures local currency with non-banking institutions and demand deposits. M2 adds local-currency time and savings deposits, and foreign-currency demand deposits. M3 incorporates other foreign-currency deposits. In deeper financial systems, these layers primarily expand through credit creation and subsequently contract through repayment. In Zambia, they expand and contract largely through the exchange rate.

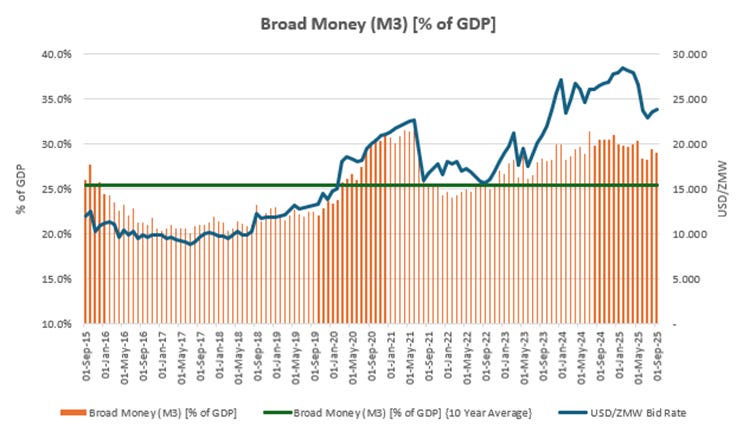

At around 44% in September 2025, foreign-currency deposits account for a material share of broad money. Changes in the exchange rate alter the kwacha value of these deposits and, in turn, M3, even when the underlying dollar balances remain unchanged. The result is a money aggregate that moves with valuation effects rather than with lending decisions, creating a structural disconnect between the policy rate and the growth of broad money.

Research from AERC (2021) supports this pattern. Zambia’s broad money growth correlates strongly with external sector conditions and exchange rate movements rather than domestic credit dynamics. When the exchange rate depreciates, M3 expands mechanically. When the exchange rate stabilises, broad money appears to contract even without changes in credit, thereby weakening the information content of M3 and limiting the impact of monetary policy on liquidity conditions.

These dynamics matter for transmission. When valuation effects rather than credit drive broad money, a lower policy rate does not materially alter liquidity in the system. It changes the headline price of money, but not the stock of money circulating through the economy. The structure of the deposit base, therefore, decides who receives the policy signal and who remains outside its reach.

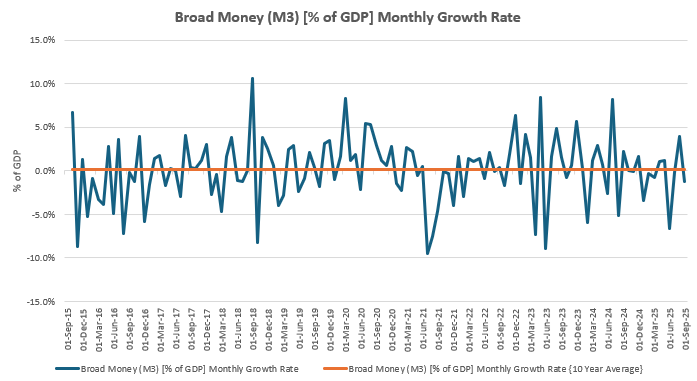

The chart above highlights the sharp month-to-month swings in broad money relative to GDP. These movements reinforce that M3 behaves as a highly volatile series rather than a stable monetary layer. The pattern aligns with the earlier discussion: liquidity in Zambia does not follow a smooth, credit-driven path but shifts abruptly when underlying valuation effects change. The volatility shown here is therefore not noise but a structural feature of the system, and it limits the usefulness of M3 as a guide for policy transmission.

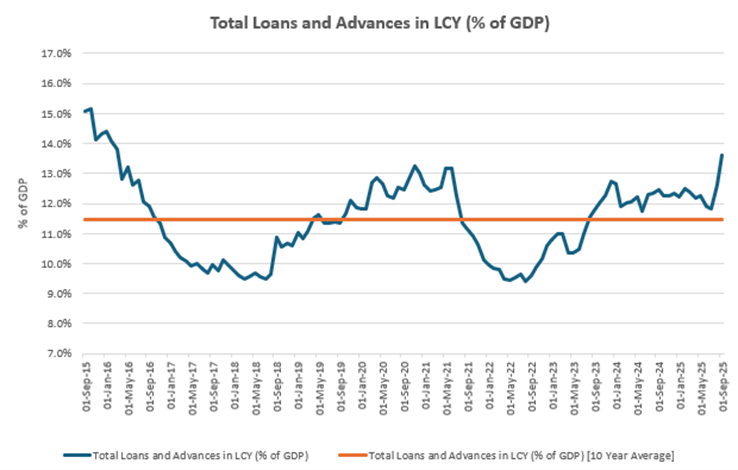

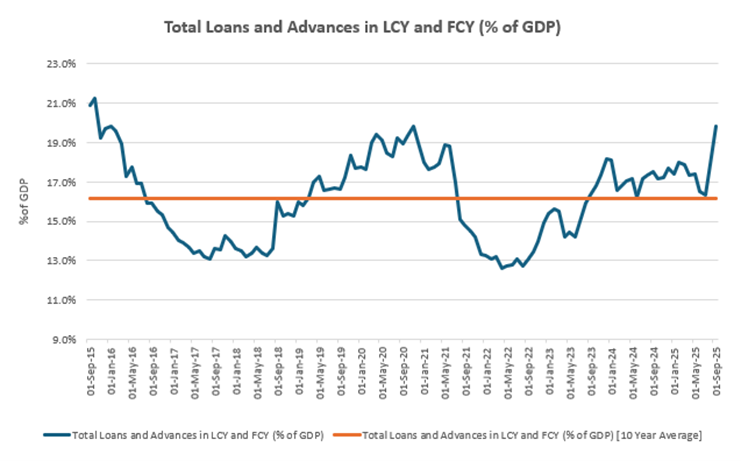

2.2 M3 to GDP and Money Base Depth

Zambia’s M3-to-GDP ratio stood at roughly 29% in September 2025, according to the central bank’s recent fortnightly data. Deeper financial systems typically range between 60% and 80%. This gap represents a foundational structural constraint. Broad liquidity is too shallow to meaningfully shift behaviour across the economy in response to changes in the policy rate. Monetary policy moves the headline price of money, but it cannot meaningfully influence the stock of money that circulates through banks and households when the base itself is this thin.

Low money depth amplifies external shocks and weakens internal transmission. When the exchange rate moves, broad liquidity changes even if domestic conditions remain constant. When the central bank adjusts the policy rate, the transmission is limited because a shallow system cannot pull credit volumes in response to a lower headline rate. The depth of the money base, therefore, determines the reach of monetary policy. In Zambia, the base is too shallow for stance changes to affect behaviour meaningfully.

This is why easing under current conditions cannot drive broad relief. Without deeper money formation, the policy rate influences only the narrow formal channel. The majority of households and small- and medium-sized firms remain outside the financial layer where the policy rate operates. A system cannot transmit what it does not have.

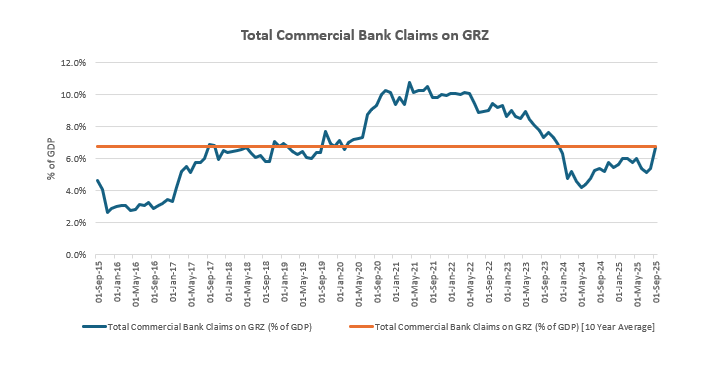

2.3 Credit Allocation and the Structural Break in Transmission

Credit allocation in Zambia remains narrow and heavily concentrated. Bank balance sheets prioritise government securities and large corporate exposures. These portfolios offer predictable cash flows, low capital charges, and strong collateral. They allow banks to preserve capital in a system where liquidity is scarce and income volatility is high. This optimisation aligns with shareholder incentives, but it limits the reach of monetary policy.

The BOZ’s 2025 credit market surveys reinforce this pattern. Banks consistently report that SME loan applications fail due to insufficient collateral, incomplete financial records, and cash flow volatility. Banks expect only marginal credit growth over the next year.

The vast majority of households sit outside the formal credit channel. Their incomes are unstable, their collateral is limited, and their borrowing histories are thin. Meanwhile, a significant portion of SMEs lack audited financial statements, consistent tax filings, or trackable cash flow. Credit models, therefore, treat them both as high risk regardless of the policy stance. Lowering the policy rate does not change these assessments. It changes the price of money but not the criteria for receiving it.

Zambia’s four-track credit economy reinforces this pattern. The small formal minority with stable incomes and established personal networks and banking relationships receives the majority of new credit. A larger formal segment earns income but has no access to formal lending. The informal sector carries the deepest inflation burden but remains largely outside the banking system. A separate informal credit ecosystem functions entirely outside monetary policy. One policy rate. Four different outcomes.

In this structure, easing supports the group least likely to change their spending behaviour. Large corporations and high-quality borrowers have the lowest marginal propensity to consume. Their credit capacity is already intact. The policy rate, therefore, provides relief to those already protected while leaving the majority unchanged.

Remember, banks behave exactly as their shareholders expect them to. They defend margins, shorten tenors, and allocate credit toward the safest exposures. Until the underlying information, collateral, and risk environment changes, credit will continue to flow along this narrow path regardless of the policy stance.

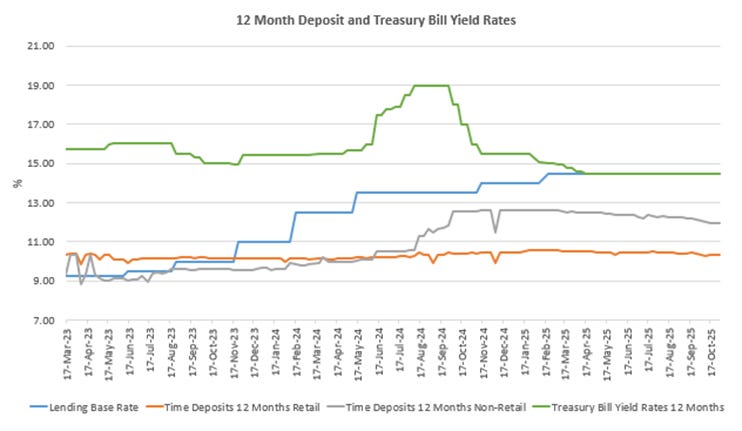

2.4 Deposit Pricing, Cost of Funds, and Transmission Failure

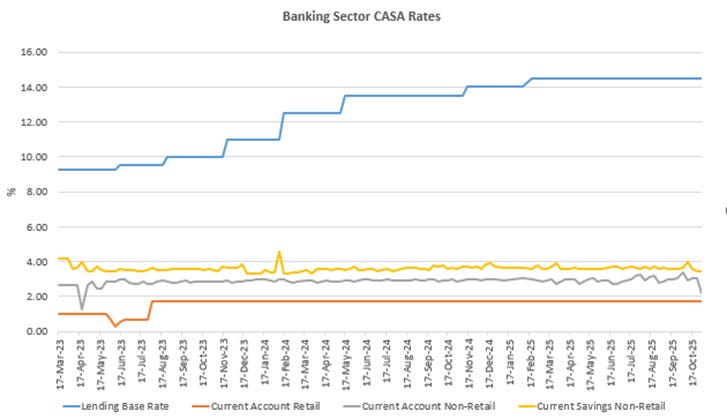

CASA rates remain almost unchanged across the entire period, even as the lending base rate rises. Retail and non-retail current account and savings rates track a narrow band and do not respond to movements in the lending base rate or to changes in monetary stance. This stability reflects the low elasticity of transactional deposits and confirms that the cost of funds at the bottom of the system remains fixed regardless of policy adjustments. The lack of movement in CASA rates partly anchors the wider funding structure and impedes the ability of lending rates to fall when the central bank reduces the policy rate.

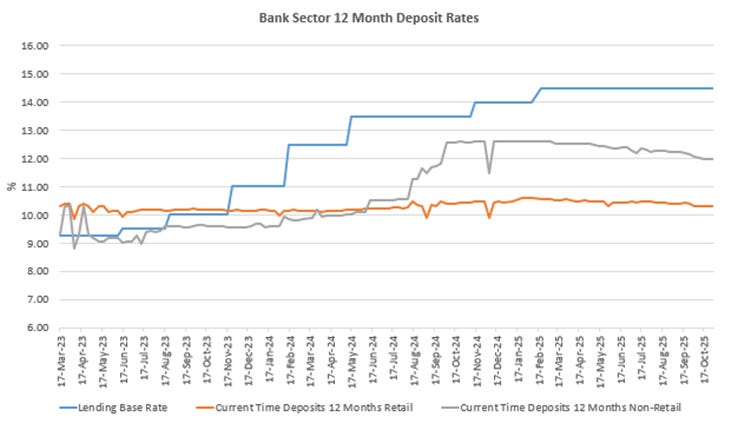

Deposit pricing also shows limited responsiveness to changes in the policy rate. The chart above shows that retail twelve-month deposits remained effectively flat at about 10% to 11% across the entire period, even as the BOZ increased the policy rate.

Meanwhile (see below), non-retail deposits remained flat between March 2023 and August 2024 and began to adjust only when treasury bill yields increased. Their movements follow the liquidity cycle reflected in bill auctions rather than the monetary policy stance.

Treasury bill yields move largely independently of the policy rate. They rose when government refinancing needs increased significantly and declined midway through the tightening cycle, thereby confirming that deposit pricing responds more to liquidity and sovereign funding pressures than to the MPC. The cost of funds, therefore, anchors itself in the bill market rather than in the policy signal.

This disconnect has direct consequences for transmission. Lending rates cannot meaningfully fall unless the cost of funds falls. Banks price loans off their base funding cost, adding operational costs, capital charges, and risk premia. When deposit rates remain flat, the base of the lending rate corridor remains fixed. A lower policy rate does not alter this floor. It changes the headline signal but not the cost of funds that drives actual lending behaviour.

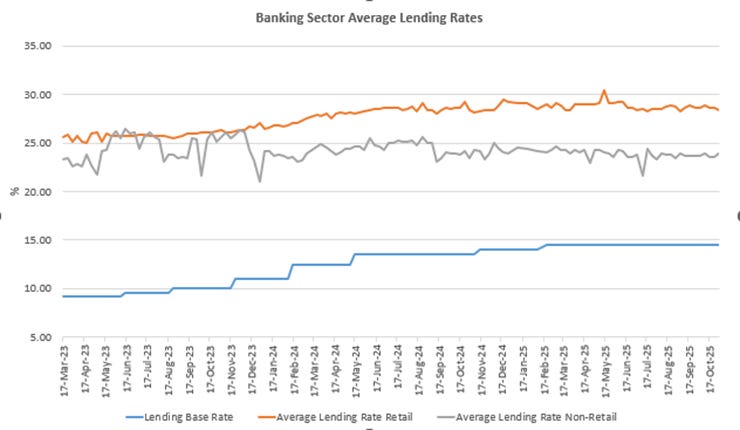

2.5 Lending Rates and Borrower Segmentation

The chart above shows that retail lending rates rise faster and remain higher throughout the tightening cycle. In contrast, non-retail rates remain more stable, reflecting households’ and small businesses’ weaker bargaining power and the banking sector’s tendency to price the retail channel defensively. We should expect this pattern to hold in an easing cycle. Retail will likely not receive the relief. Its rates will remain firm at elevated levels, while corporate rates adjust sooner and more visibly. This segmentation creates a transmission path in which the retail channel bears more of the burden during tightening phases and receives less of the benefit when conditions ease.

Risk premia remain elevated across the system, with the retail channel carrying the highest adjustments. Income volatility, weaker collateral, and limited negotiating power push banks to price this segment conservatively. Even when borrowers qualify, the risk adjustments raise effective borrowing costs.

Tenor compression reinforces this behaviour. As uncertainty rises, banks shorten loan maturities. Shorter terms raise monthly instalments and increase the effective interest burden even when nominal rates fall at the margin. Affordability does not improve because the repayment structure tightens as the tenor shortens.

In summary, banks anchor the pricing of new loans to the sovereign curve and to internal risk assessments rather than to the policy rate. When treasury bill and government bond yields rise, lending rates on new credit rise. When yields remain flat, new lending rates remain flat. When perceived risk stays high, new lending rates stay high. Transmission does not occur because none of the components that determine the pricing of new credit respond sufficiently to the change in stance. Existing variable-rate loans may adjust through movements in the base lending rate, but new credit does not reprice meaningfully in response to easing.

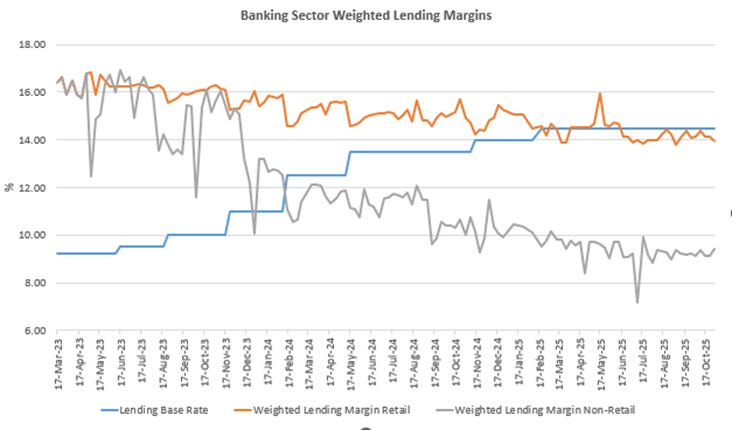

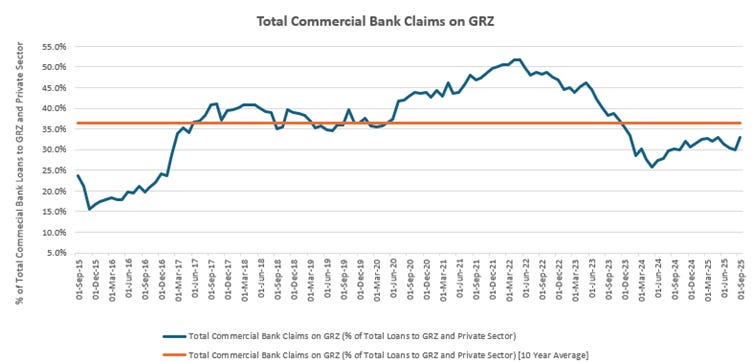

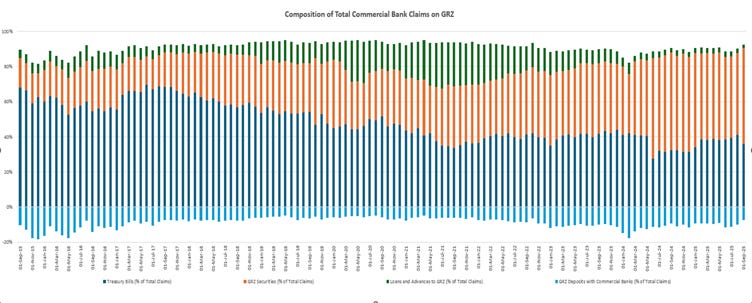

2.6 The Sovereign Nexus and Balance Sheet Preference

The sovereign curve is the spine of Zambia’s financial system. Treasury bill and government bond yields determine the cost of funds, the base of the lending rate corridor, and the structure of bank balance sheets. These yields follow the government’s refinancing pressures, liquidity conditions, and auction dynamics rather than the MPC signal. When refinancing needs rise, yields rise. When refinancing needs stabilise, yields stabilise. The policy rate has limited influence on this curve.

Banks allocate heavily to government securities because these exposures offer predictable cash flows, low capital charges due to favourable risk weighting, and practically zero non-performing loan risk. The return on equity from lending to the government is therefore higher and more stable than lending to the private sector, especially households and SMEs. These incentives create a structural preference for sovereign exposures. Transmission, therefore, remains severely limited unless the sovereign curve moves.

The sovereign nexus is therefore the core constraint. Easing enters a structure that cannot respond commensurately, if at all—the policy rate changes, the sovereign curve does not.

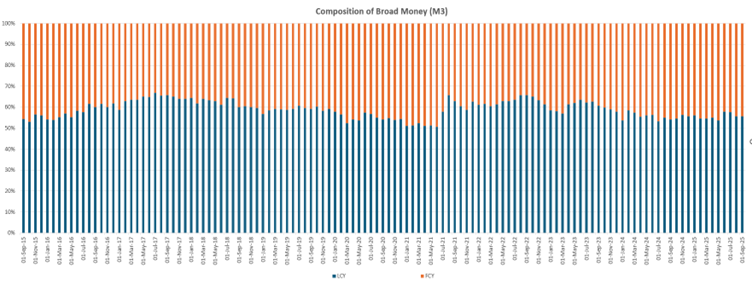

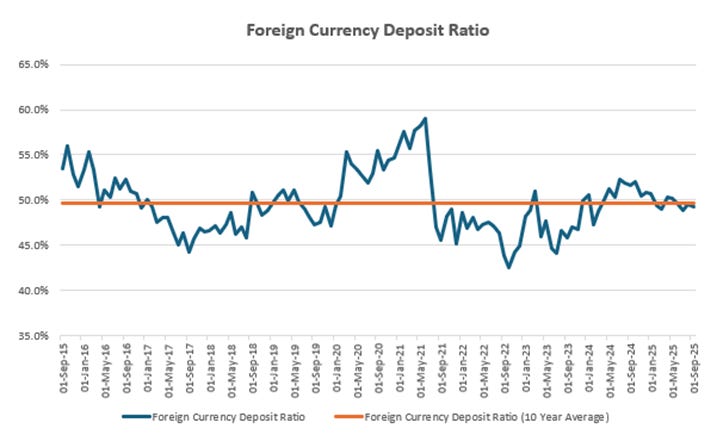

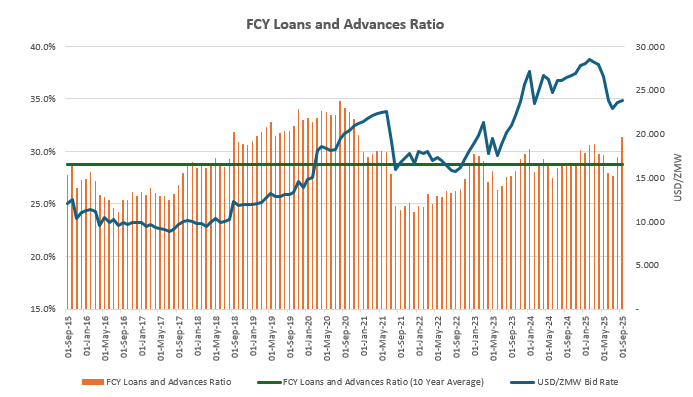

2.7 Foreign Currency Dynamics and the FX Constraint

Foreign currency deposits account for a material share of commercial bank funding, and this structure shapes how banks manage liquidity and price credit. Unlike the M3 measure, which includes non-bank holdings, this chart captures the funding base on bank balance sheets. A liability mix with this level of foreign currency exposure makes banks more sensitive to exchange rate movements than to changes in the policy rate, reinforcing weak transmission even when the stance eases.

FX volatility reshapes how banks manage balance sheet risk. Depreciation raises the kwacha value of foreign-currency liabilities and increases funding pressure, so banks preserve liquidity, shorten tenors, and widen risk premia. An appreciation reduces that pressure but does not trigger immediate easing, because banks loosen only when the currency strengthens on a sustained, flow-backed basis. The recent gains in the kwacha appear sentiment-driven rather than anchored in durable inflows, so banks are likely to maintain a defensive posture for longer. In both directions, banks respond more to currency risk rather than the policy stance, and this behaviour keeps lending conditions firm even when the central bank eases.

2.8 Consolidation of Structural Constraints

The structural constraints described in this section operate together, not in isolation. The sovereign curve anchors the cost of funds. Deposit pricing reflects treasury bill yields, not the policy rate. Credit allocation remains narrow because banks price defensively in a volatile environment. Foreign currency exposure weakens the influence of domestic policy.

Inflation remains above target, the real policy rate is only modestly positive, and the sovereign curve remains elevated relative to the stance. Under these conditions, the policy rate cannot meaningfully influence price formation or credit volumes until the structure itself changes. The policy rate still matters as a public signal, but signalling alone cannot shift behaviour when the channels that typically transmit the stance do not function.

This creates a fixed hierarchy. The sovereign curve determines the cost of funds. The cost of funds determines the lending corridor. The lending corridor determines credit allocation. Credit allocation determines who receives the policy signal. Each layer binds the one below it. The policy rate sits outside this hierarchy. Adjusting the stance does not change the structure.

Transmission weakens at every stage. Broad liquidity does not respond when the stance eases. Lending rates on new loans do not fall because the cost of funds remains unchanged. Credit does not expand because risk assessments remain unchanged. Households and small and medium-sized firms do not receive relief because the financial system does not reprice in their direction. A lower policy rate supports a narrow credit access segment dominated by corporates and high-quality formal borrowers, a group with the lowest marginal propensity to consume, while leaving the majority unchanged. This slows the adjustment path and checks the disinflation impulse.

The system’s structure neutralises the stance. Until the sovereign curve moves, the cost of funds changes, risk premia fall, and the information environment improves, monetary easing cannot deliver broad relief. Transmission requires structure. Without structure, the signal travels, but the system does not move.

3. Conclusion: Why Easing Cannot Transmit

Monetary policy can only influence behaviour when the system has channels through which to convey the signal. Zambia does not yet have those channels. A system bound to the sovereign curve, dependent on short-term deposits, and shaped by defensive credit pricing cannot translate a lower policy rate into broader liquidity, lower lending rates, or meaningful credit expansion.

This does not invalidate the stance. The policy rate still serves as the central bank’s public signal. It frames expectations and communicates intent. However, a signal cannot produce movement when the underlying structure absorbs rather than transmits it. The result is a stance that shifts on paper while conditions on the ground remain unchanged.

The IMF’s own assessment points in the same direction. Durable disinflation requires improvements in fiscal credibility, liquidity management, and the financial architecture that carries monetary signals. Without structural depth, the transmission process cannot support the adjustment path, and easing risks working against the disinflation effort by reinforcing the segment least responsive to price changes.

The lesson is sequence. Monetary policy cannot lift the economy until we repair the channels through which it operates. Transmission depends on a sovereign curve that responds to macro fundamentals, a cost of funds that reflects the stance, and a financial environment where risk premia fall as information improves. These elements lie outside the policy rate itself. They require structural reform.

Part Three, therefore, shifts from diagnosis to design. It outlines the foundations that can restore monetary transmission, the sequencing needed to align fiscal and monetary anchors, and the architecture that can move Zambia from a stance that communicates to a system that responds. Monetary policy matters when the system can hear it. Structure is the condition for that hearing.

Disclaimer

This article does not constitute legal, financial, or investment advice. The author shares views for perspective and discussion only. Do not rely on them as a substitute for professional advice tailored to your specific circumstances. Always consult a qualified legal, financial, investment, or other professional adviser before making decisions based on this content.

Canary Compass and the author accept no liability for actions taken or not taken based on the information in this article.

About the author

Dean N. Onyambu is the Founder and Chief Editor of Canary Compass. His insights draw on experience across trading, fund leadership, governance, and economic policy.

The Canary Compass Channel is available on @CanaryCompassWhatsApp for economic and financial market updates on the go.

Canary Compass is also available on Facebook: @CanaryCompassFacebook.

For more insights from Dean, you can follow him on LinkedIn @DeanNOnyambu, X @InfinitelyDean, or Facebook @DeanNathanielOnyambu.

Part 2.5 Interlude is scheduled to land in about 30 minutes. Part 3, which comes later, will set out the foundations for transmission to work and the sequence that can move Zambia from a stance that communicates to a system that responds.