ZAMBIA PETROLEUM SPECIAL REPORT: Behind the Petrol and Diesel Pump Price

The Formula You Can Run and the Line You Cannot

AI-illustration: The formula you can run, and the line you cannot.

Reader’s note. This essay is heavier than the usual Monday piece: a complete pricing architecture, seventeen tables, and a formula you can run yourself. Read it in sittings; section 8 stands alone as the tool. To give it the week it needs, The Cathode Economy moves to Monday 13 July. And to American readers, happy Independence Day, the 250th.

0. Executive Summary

This essay takes Zambia’s pump price apart and hands the reader the tools it was built with. It is dense by design; this section is the map.

Sections 1 and 2 establish the machine. A published formula prices every litre, built from the ERB’s own practice, made by the Minister of Energy and gazetted in December 2024. This reconstruction reproduces twenty-three consecutive months of announcements exactly. Nothing has to be taken on trust: section 8 hands over the formula itself, four lines and a calculator. Sections 3 and 4 identify what actually moves the price, the Gulf benchmark, the import premium and the exchange rate, and walk one month through the full chain. Section 5 examines the one line the formula cannot produce: Price Stabilisation, set each month with no published rule. It lays out what the line has done in the six months of its life alongside the tax suspension. Section 6 places Zambia’s disclosure against South Africa and Tanzania. Section 7 prices what comes next: what restoring the taxes would cost at the pump, and what the import premium must do for prices to hold anyway. The decision lands at the October review, weeks after the August election. Section 9 states the five disclosures that would let anyone verify the rest.

Read it by need. A treasurer, banker or risk manager pricing fuel-linked exposure can go straight to sections 7 and 8. A reader asking whether the announced numbers are honest starts at section 1; the answer is yes, to the ngwee, except one line. An official who owns these numbers should read section 9 first.

The premise throughout is simple. Fuel prices everything, the machine that prices fuel is almost entirely public, and the gap between almost and entirely is one line, worth K3.62 per litre on diesel this month. Closing that gap costs a paragraph in a press release. This essay shows which paragraph. The alternative is on display in the region this year. Kenya publishes its formula but not the workings of decisions taken beside it. The price went first to its streets; the question is now before its High Court.

1. The July Finding

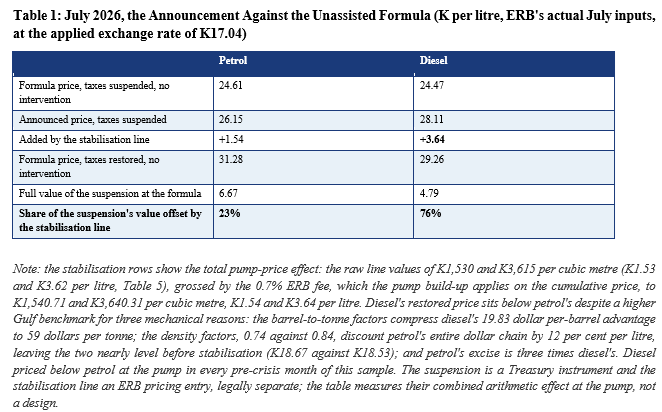

On 30 June 2026 the Energy Regulation Board announced July pump prices. Petrol fell by K1.00 to K26.15 per litre. Diesel fell by K4.00 to K28.11. The build-up published the same evening showed excise duty at zero and VAT at zero per cent. The three-month tax suspension, excise duty suspended and VAT zero-rated, due to expire that day, had been extended. The extension appeared first as those zeros; the accompanying statement did not address the taxes. The following day, 1 July, the government announced a further 90-day extension, 1 July to 30 September, implemented through Treasury instruments issued under the Customs and Excise Act and the Value Added Tax Act. The suspension has never touched Statutory Instrument 77 of 2024, the pricing instrument: it is a Treasury act under the tax statutes, and the ERB’s build-up merely transmits the zeros.

The ERB prices fuel by a published formula. Statutory Instrument 77 of 2024 prescribes the chain in two schedules, from Gulf benchmark to pump, and the Board’s monthly build-up prints every line of it. Section 8 reduces that chain to four lines any reader can run. Now run the ERB’s own July build-up twice with the discretionary support line at its neutral setting of zero: once under the extended suspension, once with both taxes restored.

Read the diesel column. The tax holiday was worth K4.79 per litre to diesel motorists at July’s formula. The stabilisation line offset K3.64 of it at the formula level. Three quarters of the diesel suspension, the headline relief measure of 2026, was offset in the same build-up that extended it, the offsetting line carrying no published rule or explanation.

The instrument is a single line in the wholesale build-up labelled Price Stabilisation/(Support). In July it added K3,615 per cubic metre, K3.62 per litre before the ERB fee, to the diesel price. Other lines in the chain move, and one of them, the import premium, has lost its own disclosure. But the stabilisation line is alone in what it is: not a cost at all, a discretionary instrument with no published rule governing its monthly quantum, no formula, and no disclosed external referent.

This essay reconstructs the pricing architecture line by line. Its origin is a single public question. The July build-up carried an exchange rate of K17.04 per US dollar. The kwacha never traded there in June, and no window of June trading averages to it. When the figure was queried publicly on 1 July, no answer came. It stood unreconciled, and that is what this essay set out to fix. A price this consequential should not contain a number this unexplainable. What follows is the reconstruction that answered the question: twenty-three months of ERB build-ups, September 2024 through July 2026, Statutory Instrument No. 77 of 2024, and the Bank of Zambia’s daily exchange rates. At the end of it, every line in the pump price reproduces to the ngwee, one hundredth of a kwacha. Except one.

The pump price in one paragraph. Zambia imports every litre. The ERB takes the Gulf market price of each fuel and adds the cost of moving it to Zambia. Diesel arrives through the Kigamboni tank farm and the pipeline to Ndola, and also by road; petrol travels by road from Dar es Salaam or Beira. It converts the total to kwacha at a formula rate built from the last two months of Bank of Zambia exchange rate averages, adds fixed fees and margins, and announces the result as next month’s maximum pump price. Every one of those steps is published and checkable. One is not: a line called price stabilisation, set each month at the Board’s discretion, which takes money from motorists when world prices fall and returns some when they spike. This essay shows you how to compute everything else. The one discretionary line then becomes visible each month as the gap between your number and the announcement.

2. What SI 77 Actually Does

The Energy Regulation (Petroleum Products Price Setting) Regulations, Statutory Instrument No. 77 of 2024, were gazetted on 3 December 2024 under the Energy Regulation Act, 2019. The December 2024 prices had been set before gazettal; January 2025 was the first review priced under the instrument, and every monthly review since has run on its formulas. The regulations codified, in two schedules, the exact formulas for the wholesale and pump prices of petrol, diesel, kerosene and Jet A-1. Codified is the precise word. The ERB’s own published build-ups from September 2024, three months before gazettal, already run the full import parity architecture: the same chain line for line, the same 2.5 per cent trigger already exercised product by product. In the three pre-gazettal reviews the slate (the exchange rate rule defined below) can test, October to December 2024, it reproduces the applied exchange rate; the plain previous-month average, the no-slate reading of the same window, misses by 37, 24 and 87 ngwee respectively. The instrument wrote existing practice into law; the machinery predates its statute.

One provision of the schedules has never visibly operated. First Schedule paragraph (b) directs that the diesel wholesale price “shall be calculated as a weighted average on a basis of 30/70% weight basis” between the Board’s paragraph (a) formula and “the wholesale price from a supplier”. Regulations 3(4) and 3(5) build the supplier machinery around it: contract awards, pipeline-savings communications, suppliers selling at Board-determined kwacha prices. No published build-up in twenty-three months shows a blend or a supplier wholesale input, and the pure paragraph (a) chain reproduces every printed diesel price. The instrument’s structural centrepiece for diesel exists on the page and nowhere else in the record.

Three provisions carry the machinery.

Prices are backward-looking by law. Regulation 3(3) requires prices to be set monthly, or as the Board specifies, based on the actual values of cost elements for the previous pricing period. Throughout this essay, the pricing window for a given month’s price is the preceding calendar month. The price announced for August is computed from data already realised when July closes. By announcement day, every input already exists. Prediction, in this system, is not forecasting. It is replication.

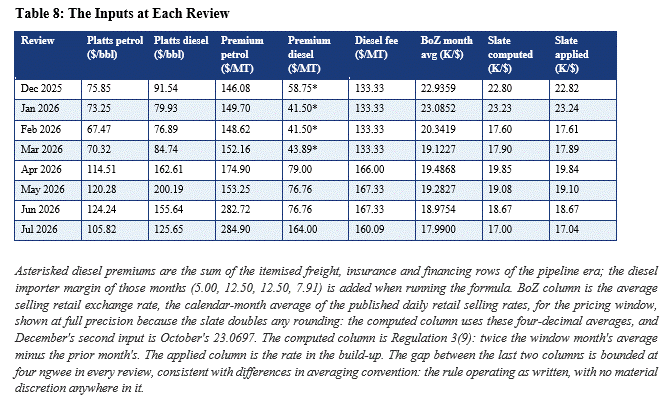

The exchange rate is a formula, not the average. Regulation 3(9) prescribes a slate mechanism: the rate applied in the pricing model equals twice the current month’s average exchange rate minus the previous month’s average. Its mathematical effect is momentum extrapolation. The applied rate deviates from the latest actual average by exactly the previous month’s change, in the same direction.

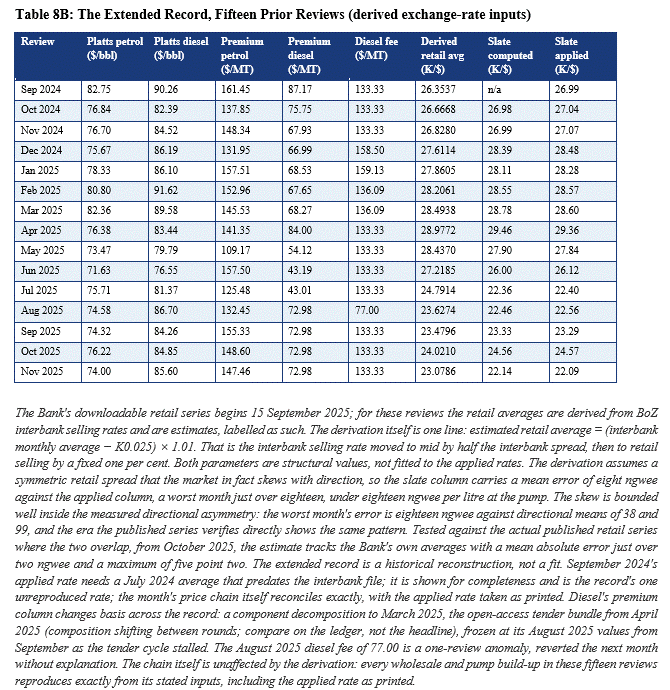

The July build-up demonstrates the consequence, and it resolves the question this essay opened with. The K17.04 is not an error; it is the intended output of the slate. The Bank of Zambia’s average selling retail exchange rate, the calendar-month average of its published daily retail selling rates, was K17.99 in June and K18.98 in May. Twice 17.99 minus 18.98 gives K17.00. The ERB applied 17.04. The same construction reproduces the applied rate in every monthly build-up since December 2025 to within four ngwee; Table 8 sets the computed rule against the applied rate at every review. The instrument carries two definitions of its own input: the interpretation clause reads “the monthly average of the closing daily selling exchange rate”, while Regulation 3(9) reads “market average retail exchange rate ... as published by the Bank of Zambia”. The published-average construction is the one the applied rates fit. The Bank’s downloadable retail record begins on 15 September 2025, so December 2025 is the first review the published series can verify directly. Behind it, this reconstruction derives the retail averages from the Bank’s interbank rates, labelled estimates throughout. On those derived inputs the same slate reproduces the applied rate in every review from October 2024, never worth more than eighteen ngwee per litre at the pump. Table 8B carries the extended record and its error band. The slate beats the plain previous-month average in thirteen of those fourteen reviews. The one exception, March 2025, is the derivation’s worst month at a trend turn, not the mechanism’s. The length of the record is the reader’s guarantee, not a trophy. A chain that reproduces every announced price under every configuration it has run is not fitted to one regime, and the slate’s own record is stated above, era by era. The tool can be carried into months that have not happened yet.

The statement’s exchange rates are a different object. The ERB’s July press statement disclosed exchange rates: the kwacha appreciating from K18.42 to K18.26 over the review period. Those figures describe movement within the window. They are not the model input. The same construction on statement figures fails in six of the eight observed reviews, matches in one, and is untestable in one, the December statement carrying no window exchange-rate figures at all. July’s 2 × 18.26 − 18.42 = 18.10; the build-up applied 17.04. The one match occurs where the statement figures happen to coincide with the BoZ monthly averages. The statement narrates the window; the model applies the slate.

The instrument defines the slate as “a mechanism to address any possible variation in the foreign exchange rate used in the previous month and the foreign exchange rate that shall be used in the current month”. Read as cost recovery, the formula does its declared job. Last month’s price ran on an older average; the market moved; the slate carries that gap into this month’s price, making the supplier whole one month in arrears. The design needs no account and keeps none: each month’s error settles in full at the next review, and the settlement runs both ways. The statute writes the rule in its own notation, with m marking the month:

eafx = em + (em − em−1)

The current month’s average, plus the month’s move, added again: rearranged, it is the twice-minus rule stated above. Subtract the current market average from the applied rate and the identity does the rest:

eafx − em = em − em−1

What remains is exactly the month’s move. The applied rate therefore sits above the market in every depreciating month and below it in every appreciating month by construction: consumers carry the recovery when the kwacha weakens and receive it when it strengthens. The record prices both directions: across the twenty-two reproducible reviews, a mean of 38 ngwee above in depreciation, 99 below in appreciation, and the extreme, February 2026, worth K3.00 per litre at the petrol pump on the chain as printed. Two designs exist for carrying such corrections: settle each month’s error in full through the next price, or accumulate the errors in an account and recover the balance over time through a published levy. Zambia’s instrument chose the first. It keeps no buffer: the whole adjustment travels through the pump, in the consumer’s favour or against it, in the very next review. South Africa’s Basic Fuel Price system chose the second: pricing errors accumulate in a formal Slate Account, and the balance is amortised gradually through a self-adjusting slate levy, shielding the pump from the swing. The South African account carries the whole formula error rather than the exchange rate alone, and section 6 shows what it has just absorbed.

Zambia’s choice has a coda. For seventeen reviews nothing stood between the slate’s amplitude and the pump except the trigger’s 2.5 per cent gate, as the design intends. The February 2026 build-up, computed like every review from the previous month’s data, carried the slate’s largest swing and, for the first time, a stabilisation line: the same document manufactured the windfall and absorbed two thirds of it. Whether the line does an account’s work in general is a harder question, and section 5 answers it product by product: a price pin for petrol, smoothing against far larger benchmark swings for diesel, abandonment for kerosene. What the record settles is narrower and stranger: the design that keeps no buffer acquired a discretionary one, unruled and unpublished, in the slate’s most extreme month.

The Board may add or vary charges directly. Regulation 4 carries two gates: 4(1) permits the ERB, where a new charge, levy, tax or fee is introduced, to add or subtract it within the schedule formulas; 4(2) permits price adjustments on changed cost elements, with a one-month duration under 4(3), extendable under 4(4). The tax suspension enters the build-up as zeros, and the stabilisation line entered in February 2026, under Regulation 4; no located document states through which gate. Regulation 4(5) requires any adjustment under the regulation to be published by press and on the ERB’s website.

One further provision matters for reading the monthly announcements. Regulation 3(10) directs the Board to adjust prices only when the calculated change in the wholesale price exceeds 2.5 per cent. The trigger operates per product, on the wholesale price, against the prevailing published level. Petrol held in January on a latent change of 0.11 per cent and in May on a latent change of minus 1.91 per cent. In hold months the ERB still publishes the freshly computed wholesale price; the pump build-up simply reprints the prevailing column. The latent series is always observable. The extended record shows how fine-grained and how symmetric the gate is. Petrol was held in February 2025 at a latent change of plus 2.4960 per cent, and diesel in August 2025 at plus 2.4847, each a whisker inside the line. An April 2025 kerosene hold denied consumers a 2.23 per cent cut. The trigger absorbs movements in both directions, including favourable ones. The regulation’s text reads only “above 2.5%”, without directional language: on its natural reading the gate tests the size of a change, rather than its direction. The record confirms the Board applies it that way. Cuts larger than the threshold have passed through in every observed instance, and the two documented downside holds blocked cuts that fell short of it.

3. The Layers Inside the Pump Price

The wholesale chain begins with the Platts Arab Gulf assessment in US dollars per barrel, the free-on-board price of the product in the Gulf market. A fixed conversion factor turns barrels into tonnes: 8.42 for petrol, 7.56 for diesel. The chain then adds storage at port, wharfage, and the Bulk Petroleum Supply premium. That produces cost, insurance and freight at Dar es Salaam or Beira. It then adds the transportation fee to Zambia, transportation losses of 0.5 per cent for petrol and 0.3 per cent for diesel, and the importer’s cost-plus margin, producing CIF Lusaka/Ndola. Storage losses at the same rates complete the dollar chain. Conversion factors of 0.74 and 0.84 turn tonnes into cubic metres. The slate exchange rate converts dollars into kwacha. That kwacha figure is the Price Before Stabilisation. The stabilisation line is then added or subtracted. The result is the wholesale price at which suppliers must sell to oil marketing companies (OMCs).

The retail stack adds the Ndola fuel terminal fee of K62.64 per cubic metre and the marking fee of K204.59. It adds excise duty, K2,340 for petrol and K750 for diesel, both zero since April 2026, and transport to depot of K650. It adds the OMC margin, the dealer margin, an ERB fee of 0.7 per cent, and the Strategic Reserves Fund levy of K150 per cubic metre. VAT at 16 per cent, zero-rated since April 2026, completes the stack. Dividing by one thousand gives the pump price per litre.

Across the full record of monthly build-ups verified, September 2024 through July 2026, every one of these lines reconstructs exactly, to the hundredth of a kwacha. That holds through the instrument’s gazettal, the open-access framework’s launch and suspension, the tax suspension, and every repricing in between. The conversion factors never moved. The loss rates never moved. The chain’s structure never changed: the same sequence from Platts to pump in every month. Inside it, the diesel premium’s composition moved with the tender rounds: storage and freight entered and left the bundle between April and August 2025. Each move is visible in the build-ups; none was announced in a statement.

What did move is dated to the month, five administered repricings in twenty-three months. The petrol transport fee moved once, 220 to 210 dollars in March 2025; excise once, at the February 2025 step; the kwacha retail stack three times. October 2024 raised the OMC and dealer margins a uniform 15.5 per cent. November 2025 raised the OMC margin 23.2 per cent, the dealer margin 31.8 per cent and transport-to-depot 25 per cent, worth K1.11 per litre on petrol and diesel. It was executed inside a review whose wholesale costs fell 9 to 12 per cent. Consumers received pump cuts of 5.3 and 3.2 per cent where the prior structure would have delivered 8.9 and 7.5. April 2026 raised the margins again, 18.9 and 24.2 per cent, 82 ngwee per litre, inside the same announcement that carried a 63 to 92 per cent international price shock and a headline tax suspension. Neither of the two repricings with a press statement on record to check was mentioned in it. The formula in section 8 is the instrument that detects them: the November 2025 reset would have printed as a K1.11 residual to any reader running it that evening. A study behind the recent resets had a public trace: an FCDO-funded consultancy on downstream margins, disclosed in the ERB’s December 2025 briefing. The resets themselves, their sizes and their dates, appeared in no statement I could locate. Table 13 carries each change as an era boundary in the reader’s formula.

Five inputs move monthly, and section 8 assigns each a letter. Three are read from the build-up and the market: the benchmark, the exchange rate, the diesel transport fee. The two that remain are this section’s subject, and they behave very differently: one is a cost that lost its documentation, the other is not a cost at all.

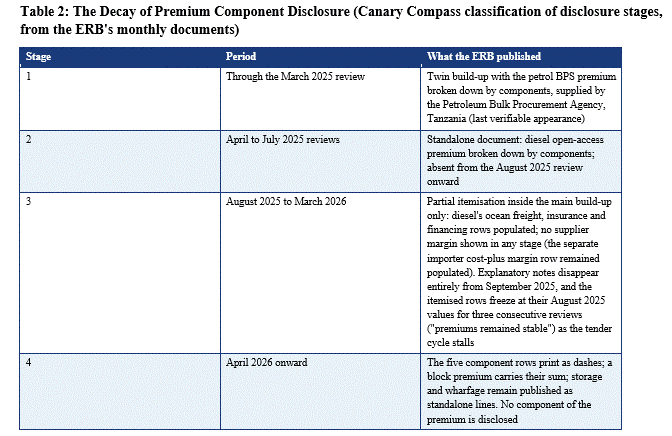

The Bulk Petroleum Supply premium is a documented cost that lost its documentation, in four stages. SI 77 defines the premium as the sum of freight, insurance, financing costs and supplier margin, tipper charges and local charges on the Tanzania bulk supply system. Five of the six have their own rows in the build-up; the supplier margin, the bulk supplier’s own return under the SI’s definition, has never had one. Storage at port and wharfage are separate standalone lines outside the premium, and they remain published in every month, including now. The disclosure record, from the ERB’s own monthly pages, is set out in Table 2.

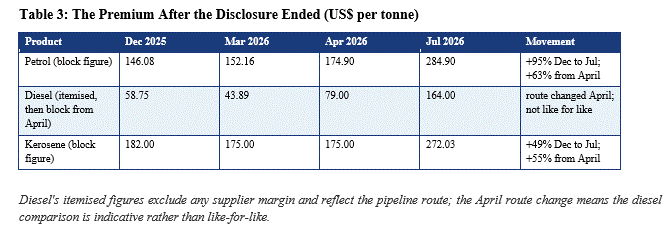

The timing is the finding. The IMF’s May 2026 staff statement records that the suspension of the TAZAMA (Tanzania Zambia Mafuta pipeline) open-access framework removed a mechanism that had previously reduced fuel import premiums by about 50 per cent. The Fund recommends restoring it alongside transparent import auctions. The build-ups also quantify what the framework was worth while it ran, so the Fund’s “about 50 per cent” is not a figure this essay has to borrow. The framework’s official chronology, per the ERB’s 2025 mid-year briefing: guidelines approved December 2024, first tender concluded February 2025, effect from 1 April 2025. The comparable diesel premium bundle fell from US$147.66 per tonne in March 2025 to US$84.00 on arrival, 43 per cent, and to US$43.01 by the July 2025 tender, 71 per cent below the March level on the printed bundles. The bundle’s composition shifted between rounds, so the comparison runs on the component ledger, not the headlines. The tender was let on a bundle wider than the premium line: it carried storage and the importer’s margin. The pre-tender comparator is therefore built on the same basis, and the bundles below are wider than the premium rows in Tables 3 and 8. On the ledger: March’s 147.66 is premium 68.27, storage 9.23 and importer margin 70.16; April’s 84.00 as tendered is freight 28.47, storage 9.23, insurance 2.21, financing 11.46 and margin 32.63, the same three elements present, April’s freight, insurance and financing together standing where March’s undecomposed premium row stood, so the 43 per cent arrival figure is constant-basis. July’s 43.01 carries storage, insurance, financing and margin with ocean freight out of the bundle from June, so the 71 per cent spans a composition change; the arrival figure is the safe one. Either way, the Fund’s about 50 per cent sits inside the record’s own bracket, 43 at arrival and 71 at the trough. A third public quantification exists: the ERB’s December 2025 briefing credits the framework with the whole diesel pump fall from K32.54 in March 2025 to K23.13 in July, approximately 30 per cent. The build-ups decompose that fall: the premium collapse carried roughly a quarter of it, with the benchmark’s decline and the kwacha’s appreciation carrying the rest. The framework’s verified worth is the premium bracket above, and it needs no inflation. The August 2025 round repriced the bundle to US$72.98 per tonne, and there it froze for three consecutive reviews as the tender cycle stalled; the suspension followed. Table 3 quantifies what happened to the premium after its documentation disappeared.

The standalone disclosure had already been discontinued months before the framework was suspended. The framework’s suspension extinguished the last embedded itemisation. In the four months since, the diesel premium roughly doubled, petrol’s rose by nearly two thirds, and kerosene’s by about half, each inside a single undecomposed line.

Why petrol’s premium rose is exactly the question the current disclosure cannot answer. The candidates are real: war-risk insurance, freight and financing all reprice in a Gulf crisis, and financing scales with cargo values that jumped 63 to 92 per cent. The untendered products carry the shared factor: petrol’s block rose 63 per cent from April, kerosene’s 55. Diesel’s rose 108 per cent on a basis that changed in April, so its excess over the road products is consistent with the tender’s death, and not attributable to it alone. From April 2026 the premium is a single number, so the split between cost and margin is not public information. In the disclosure regime of a year earlier, this paragraph would be a table.

Why diesel alone could be tendered. Petrol and diesel are separate finished products moving on separate logistics, and that separation is the premium story’s architecture. A refinery co-produces them from crude in roughly fixed proportions, which is what the crack complex prices, and that was Zambia’s world in the Indeni era, when spiked crude came up the TAZAMA line and Ndola produced all three products. That world ended when Indeni stopped refining and became a marketing company and TAZAMA was converted from crude to finished low sulphur gasoil, both recorded in the introduction to the ERB’s own quality control guidelines. Since then everything arrives as a finished product, and the products part ways at the coast. Diesel ships into the Kigamboni tank farm and comes up the pipeline, a single-product line, and also arrives by road: the 2025 split was roughly 57 to 43 in the pipeline’s favour, per the ERB’s 2025 Statistical Bulletin. Regulation 3(8) prices the diesel transportation fee as the volume-weighted average of the two routes. The pipeline stream is what open access could put to competitive tender.

Petrol and kerosene travel by road, occasionally rail, from Dar es Salaam or Beira. That is why their build-ups carry flat road transport fees of 210 and 205 dollars and untendered block premiums. It is also why the multi-purpose Zambia-Tanzania pipeline project in the ERB’s mid-year briefing exists at all: it is the plan to give petrol what diesel already has. One architectural fact carries the whole divergence of the last fifteen months: a tendered pipeline premium that collapsed under competition and then doubled when the tender died, beside a road premium that floats free because nothing competes for it.

What actually moves the price. Strip the chain to its movers and rank them by their largest single-review worth at the pump. First, the Gulf benchmark: swings of 63 to 92 per cent in the April review, worth up to K10 per litre on diesel and about K5.5 on petrol. Second, the slate exchange rate: a 24 per cent applied collapse in February, worth roughly K6. Third, the stabilisation line: a charge of K3.64 and a credit of K1.40 at its recorded extremes, at the Board’s discretion. Fourth, the import premium: about K1.80 in its largest single move, June’s petrol repricing, and 95 per cent cumulatively across the current sample. Everything else in the build-up is furniture, though the furniture gets repriced: three retail-stack resets in eighteen months, worth up to K1.11 per litre, none carried in a press statement where one exists to check. The benchmark and the premium price the world. The slate and the stabilisation line are the Board’s entries, and only the slate has a published rule.

The stabilisation line is not a cost at all. It is an instrument. Its history occupies section 5, because it is the story.

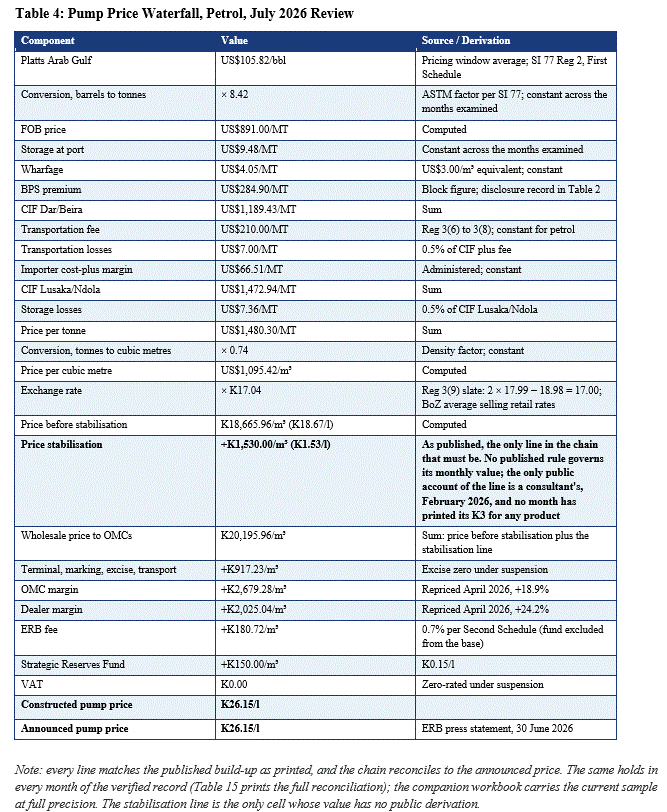

4. The Illustrative Waterfall

Table 4 constructs the July 2026 petrol pump price from source. Every figure is read from the ERB’s published July build-up or derived from SI 77. The constructed price equals the announced price. This is the difference between this market and the lending market examined in Behind the Lending Rate: there, the mechanism was invisible and the constructed rate was a plausibility exercise; here, the mechanism reconciles to the ngwee, and exactly one line has no public derivation.

5. Eight Reviews of Evidence

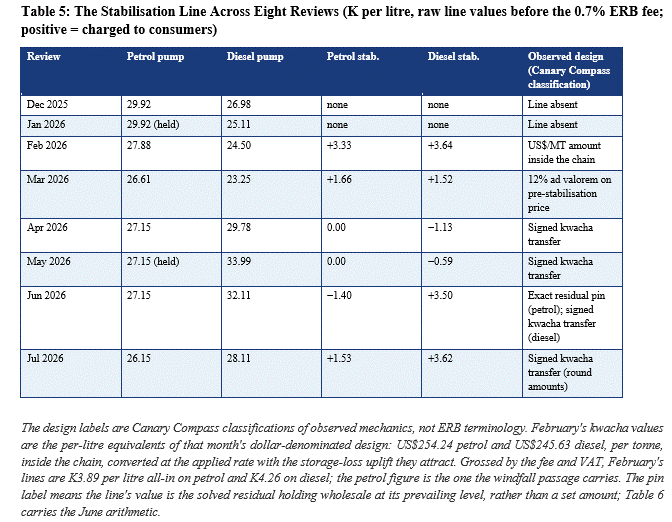

Four designs in six active months, and the line’s printed name moved with its design: Price Stabilisation in February and March, Price Support in April, Price Stabilisation again by July. The line entered under the Board’s Regulation 4 power to add charges directly; no prior announcement was required, and none has been located. The intention had an official trail. In October 2025 the Director-General told the press that a shift to quarterly reviews would need price stabilisation funds in place, and the December 2025 year-end briefing described monthly reviews as continuing prior to consideration of the migration to longer pricing periods. The vehicle, its value and its rule appeared in neither. The line reached the public as the February numbers themselves.

The fullest public account of it belongs to energy consultant Chikwanda, in the Zambia Monitor of 18 February and his own Daily Mail column of 24 February. His account: a K3 per litre surcharge into the energy fund, the cost-line SI 77 defines for price stabilisation and strategic reserves, to underwrite a shift toward quarterly price reviews. The K3 had no official source to cite. The February build-up had been public since 31 January, printing the line at K3.33 on petrol and K3.64 on diesel, and a flat K3 sits just under both. The account reads as arithmetic worked backwards from the prints, because nothing official ran it forwards. No month has printed K3 for any product. In February the line was a dollar amount whose kwacha value of K3.33 on petrol already includes the storage-loss uplift it attracts inside the chain. The ERB fee and, while VAT applied, 16 per cent on top took the all-in consumer cost to K3.89 on petrol and K4.26 on diesel. In March 2026 it became a uniform 12 per cent of the pre-stabilisation price. In April it changed sign.

The February introduction landed in the exact month the slate produced its largest windfall. The mechanism had just turned an 11.9 per cent fall in the monthly average exchange rate into a 24 per cent collapse in the applied rate. Against the prevailing price of K29.92, the no-levy February formula gives K23.99: a windfall of K5.93 per litre. The announced price was K27.88: prices still fell at every pump, a cut of K2.04, and the charge ran invisibly inside the cut, visible only to a reader running the formula. The stabilisation line absorbed K3.89 of the windfall, two thirds of it. Diesel ran the same way, a charge of K3.64 raw and K4.26 all-in inside a price that still fell. The slate manufactured the amplitude; the line absorbed it. The timing is the record’s own; this essay claims nothing beyond it.

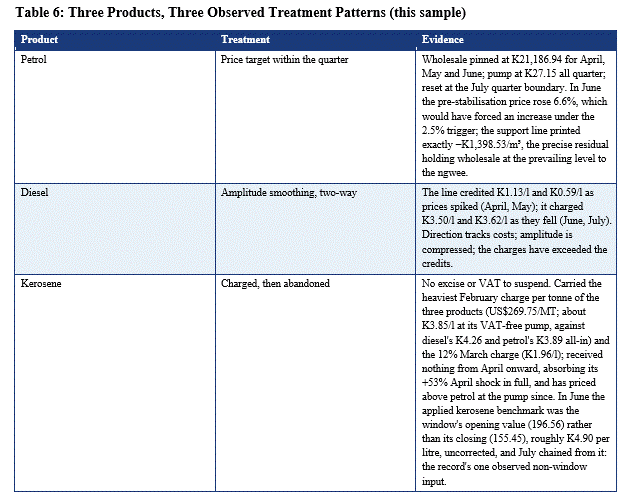

The line has run for six months, and no located document states which gate of Regulation 4 it entered through. Under Regulation 4(1) no duration limit attaches; under 4(2) its duration is one month under 4(3), extendable under 4(4), and no extension determination appears in the record. Under either gate, Regulation 4(5)’s publication duty applies, and no rule has been published. The eight-review record resolves the line’s behaviour into three observed treatment patterns, set out in Table 6, and into the estimated gross charges in Table 7.

Petrol’s pattern is the February intention operating. The purpose on public record was quarterly price stability; reviews stayed monthly, and the line delivered the quarterly outcome on petrol by solving for it each month, with the July boundary reset on schedule. The record shows the execution diverging by product: one design for petrol, four in six months for diesel, nothing for kerosene, and no located statement explains the divergence.

What the accumulation is remains undisclosed, and the possibilities are three. It may be cash in an account, held as a buffer against the next adverse review: the diesel record, charging into falls and crediting into spikes, is consistent with that reading, and a working buffer makes the missing balance more anomalous rather than less, since a buffer is exactly the thing that is its balance. It may be a ledger: no money remitted anywhere, the industry ahead by the balance and owing it back through future credits. That is mechanically how South Africa’s Slate Account works, and it is consistent with the April and May credits, whose financing nobody has disclosed. Or it may already be spent, against the suspension’s cost, against another purpose, or otherwise; if so, nothing was ever parked at all. Nothing published selects among the three. One fixed point exists in law, conditional on a step nobody has disclosed: the destination the press account named, the energy fund, disburses only with the Secretary to the Treasury’s approval under SI 56. Whether this money entered that fund, any fund, or any account at all is the undisclosed step. Section 9’s second demand states what would settle it.

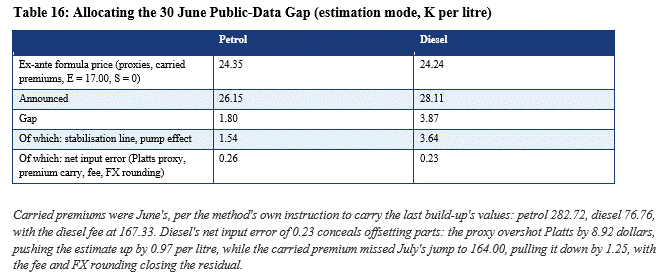

The indeterminacy this architecture imposes on outside estimates can be measured. Section 8 runs the full exercise using only data public on 30 June, and Table 16 allocates the gaps: almost entirely the stabilisation amounts, with net input error under 30 ngwee per litre. In calm months the public-data method lands within roughly one kwacha per litre before the stabilisation scenario. Across a Gulf-specific supply shock the benchmark proxies alone can miss by K3 to 5. The formula is reproducible. The price is not, and the distance between those two statements is one discretionary line.

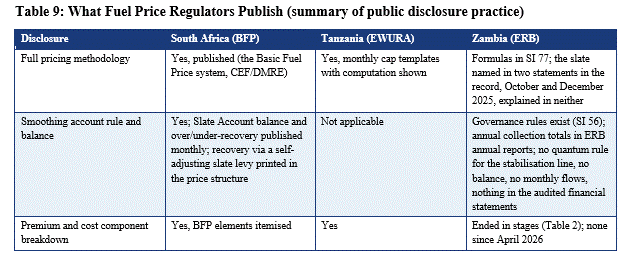

6. The Regional Comparator

Table 9 sets the three disclosure regimes side by side. Zambia publishes more than either comparator on the build-up itself, and less than either on the machinery around it. The monthly build-up is a genuinely transparent document; this essay exists because it is. The gap is a choice, and the record dates it: the ERB published component-level premium disclosure for years and ended it in stages; the fund side has never been published at all. Kenya is deliberately absent from this table: it is section 9’s cautionary case, not a disclosure benchmark.

The account design’s cost and worth are both on display this year. Under the Basic Fuel Price system, daily over- and under-recoveries accumulate in the Slate Account instead of passing straight to the pump. The account stood R4.49 billion positive in April 2025; by April 2026, after the same Gulf crisis this essay prices for Zambia, it stood R18.28 billion negative, and the Self-Adjusting Slate Levy stepped from zero to about R1.58 per litre to amortise the deficit gradually, on a balance the DMRE publishes in its monthly statements. Zambia’s formula keeps no such account: the exchange-rate correction passes to the pump in full at the next review. The smoothing that does occur happens at the stabilisation line, at the Board’s discretion, with no published rule and no published balance. Both countries smooth; one prints the rule and the ledger.

One implication deserves exact statement. If the accumulation the stabilisation line has built is held against future support, in cash or as a score, Zambia is operating the functional equivalent of the Slate Account just described, undocumented. It would rest on two instruments that each stop short: Regulation 4 empowers the Board to insert the price line and says nothing about the money; the Energy Fund is an account with full statutory machinery, but the line is absent from its regulations’ inflow list, and entry would travel under an approval of the Minister responsible for finance that nobody has published. Either the money sits in the legislated account whose machinery has produced nothing public, or the score sits outside any located instrument. A slate account operating undocumented is the precise name for what either reading implies; the difference between the readings is only where the balance lives: in an account, on a ledger, or nowhere.

7. When Can the Taxes Come Back

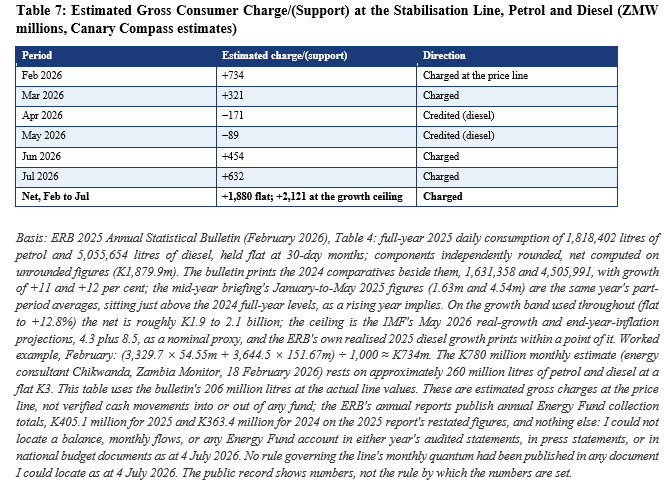

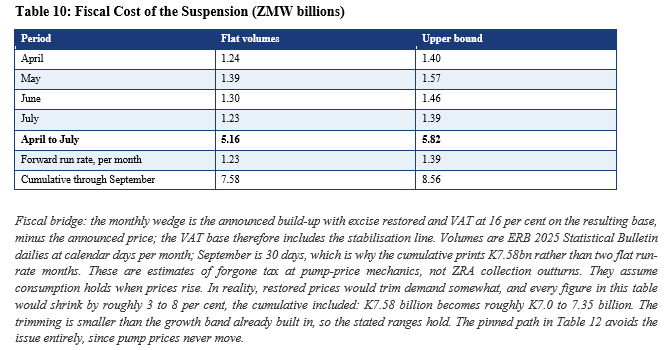

The suspension’s fiscal cost is now material to the national accounts. Measured against the ERB’s actual monthly build-ups, restoring excise and VAT would have added K7.08 per litre to petrol in April through June and K6.92 in July, and between K5.37 and K6.31 to diesel. On ERB 2025 consumption volumes, with growth bounded between flat and 12.8 per cent a year, the cost runs as in Table 10; the ceiling is a nominal proxy built from the IMF’s May 2026 projections, with the derivation at Table 7.

The IMF’s May 2026 staff statement names the suspension among the drivers of the primary surplus falling from a programmed 3.8 per cent of GDP to a projected 1.1 per cent, alongside election-period spending pressures, a civil service wage adjustment, and agricultural subsidy overruns. It separately flags that the VAT refund backlog is weighing on taxpayer compliance. The suspension is no longer a line in an energy story. It is inside the fiscal story.

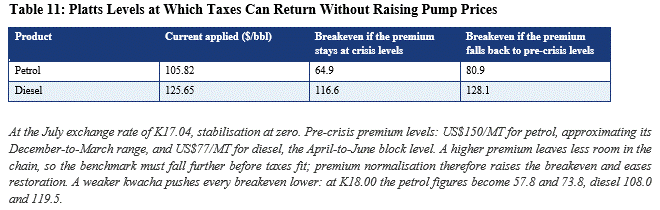

So when does the rationale to extend expire? The formula gives a precise answer. Restoration without pump-price increases requires the wholesale price to fall 29.3 per cent for petrol and 20.8 per cent for diesel from July levels. Inverting the full chain at the July exchange rate produces the breakeven benchmarks in Table 11.

Two conclusions sit in that table. First, diesel reaches breakeven under the normalised-premium case, and premium normalisation is the channel through which restoring the TAZAMA open-access framework, the IMF’s own recommendation, would most plausibly operate. Second, petrol is the binding constraint: even with a normalised premium, its benchmark must fall roughly a quarter from current levels, and it is not falling.

The reason is the crack spread, and the term deserves a definition, because it is carrying the forward story. A crack spread is the gap between what a refinery pays for a barrel of crude and what the refined products from that barrel sell for: the market’s proxy for refining margins. The most quoted version, the 3-2-1, prices two barrels of petrol and one of diesel against three barrels of crude. It widens when products are scarce relative to crude, on demand seasons, refinery outages, or geopolitics, and it is a gross margin proxy, not profit, since it ignores refinery running costs. Right now the spread is doing something unusual: crude has retreated toward pre-crisis levels while the cracks have not. Diesel and jet refining margins remain elevated as Europe and Asia replace the volumes Hormuz used to supply, on the assessment of the US Energy Information Administration (EIA); in the US Gulf Coast market, the proxy this essay uses in section 8, diesel cracks run near three times their year-ago level. Petrol’s crack has widened even as crude fell, and the mechanism reaches Zambia because gasoline is one globally arbitraged market whose regional prices move together, on the EIA’s own account. The northern-hemisphere driving season is tightening that market at the demand end, and refiners chasing the far larger distillate and jet margins have shifted output away from petrol at the supply end, per market analyses of the post-Hormuz refining slate (Stillwater Associates, May 2026). Both forces reach the Arab Gulf assessments the ERB prices from, though not one for one: specification differences mean the seasonal component transmits partially. The seasonal leg starts fading when the US summer specification season ends in September, weeks before the October review, per the EIA’s seasonal account. The formula prices products, not crude. Restoration on the formula path is therefore not a September event. Petrol’s breakevens sit 24 to 39 per cent below the current benchmark; diesel’s require a premium normalisation that has not occurred; and the announced extension runs to 30 September regardless.

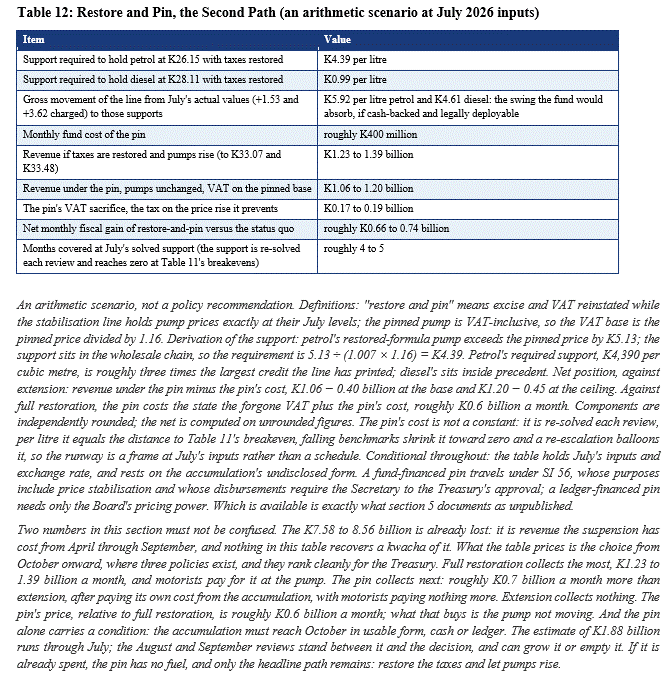

But the formula path is not the only path, and the architecture this essay documents creates a second one. Call it restore and pin. In plain terms: the government reinstates excise and VAT, and in the same review the Board sets the stabilisation line negative by exactly enough that the wholesale price falls by what the taxes add back. The motorist sees the same price at the pump. The Treasury collects excise and VAT again. Someone finances the wedge, and the financing depends on the accumulation’s undisclosed form. If it is cash, the natural home is the energy fund: SI 56 names price stabilisation among the fund’s purposes, and every disbursement travels under the Secretary to the Treasury, who is also restoration’s beneficiary. If it is a ledger, the industry disgorges its own accumulated over-collection through the negative line, and the pin needs no disbursement at all, only the Board’s pricing power. The solver itself is not hypothetical. It is the pin the Board ran on petrol from April to June, pointed at a different target: then it held the pump against moving costs, here it would hold it against returning taxes. Its negative values have printed before, though never near petrol’s required size; the note beneath Table 12 carries the multiple. Table 12 prices the path at July inputs.

The accumulation the windfall months created would, if it reaches October intact, be arithmetically sufficient to finance motorists’ protection from the taxes’ return, while the Treasury resumes collecting.

Extension through September is now announced policy, not a forecast: the 1 July statement extended the suspension a further 90 days, 1 July to 30 September, through Treasury instruments under the Customs and Excise Act and the Value Added Tax Act. Elections fall on 13 August. Extension arrived first as zeros in a build-up; restoration, even the pinned variant, requires a visible act weeks before a vote. From October the calculus inverts. The election passes, and successor-programme negotiations resume with what the IMF itself calls the incoming government. The record shows the timing. It does not show the motive, and this essay does not supply one. The restore-and-pin arithmetic then allows revenue resumption without a pump-price headline. The earliest scheduled restoration decision is therefore the October review, announced at the end of September, exactly where the 90 days expire. Four markers will signal it. Any reinstatement of the TAZAMA open-access framework would move diesel toward breakeven; under Table 11’s normalised-premium case, to breakeven. Continued accumulation at the stabilisation line through the August and September reviews finances the pin, and since the pin began in April, petrol’s line has moved only at the quarter boundary, of which the next is October. And the slate’s next prints matter, since each firmer kwacha month pushes the breakevens further away. The fourth sits above the other three: the crack spreads themselves, running far above their historical relationship to crude. That divergence closes one way or the other, and its direction decides October. Product prices falling to meet crude pulls petrol’s benchmark toward breakeven exactly as the decision arrives; crude rising to meet the products is the escalation scenario, and it entrenches the suspension. One risk cuts the other way: October can bring a further extension rather than a restoration, and each extension normalises the last. At K1.23 to 1.39 billion per month, the suspension annualises to roughly 7 to 8 per cent of the 2026 budget’s K206.45 billion domestic revenue target (2026 Budget Address, 26 September 2025). Somewhere on that path, temporary relief stops being relief and becomes a feature of the tax system nobody legislated.

8. The Reader’s Formula

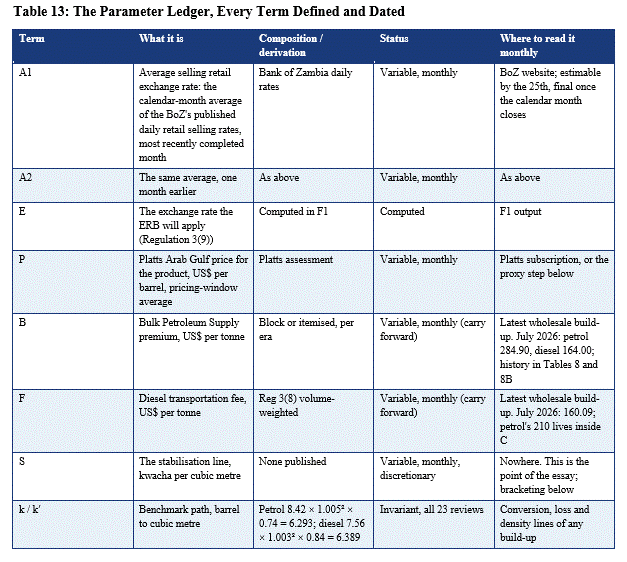

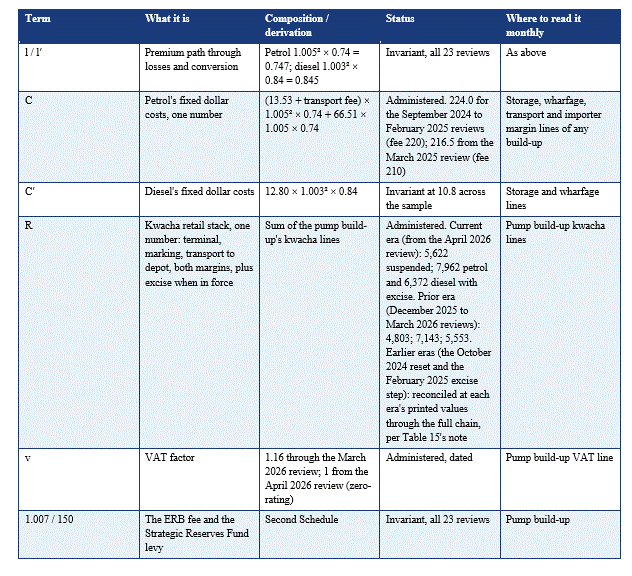

The sixty-second version. The inputs that move monthly carry letters: two exchange rate averages (A1 and A2), the Gulf benchmark (P), the premium (B), the diesel fee (F), and one unknown, the stabilisation line (S), which cannot be computed from anything published and which this section teaches you to bracket. One rate: twice the latest month’s average minus the prior month’s. One chain: the formula below, run at the parameter values in Table 13. The result is the wholesale price; the retail parameters take it to the pump. Every term is defined in Table 13.

The chain in Table 4 collapses, exactly, into four lines of arithmetic, and the model below is presented the way the instrument itself is written: SI 77 prescribes formulas with named components and prints no numeric values, leaving the numbers to the ERB’s monthly implementation. The model’s terms come in three kinds, and the distinction is the tool’s honesty. The first kind moves monthly by design and carries symbols: the benchmark, the premium, the diesel fee, the exchange rate, the stabilisation line. A second group is administered: the kwacha margins, transport, excise and VAT, set by decision and frozen between decisions; the record shows five dated reset events in twenty-three months, each printed in its build-up the evening it took effect. Everything else never moved in the sample: the conversion and density factors, the loss rates, the port costs, the fee percentage, the levy, the trigger, the slate rule. The formula below is therefore written once, in letters; Table 13 is the parameter ledger that dates every change and marks which kind each term is. A reader carries the invariants for good, refreshes the administered values from the latest build-up, and supplies the five variables. One month’s document is enough to read every current parameter; the other twenty-two serve only to confirm the eras. Nothing else is required.

The formula runs in two modes, and every table below states which it is using. Reconciliation mode takes the ERB’s published inputs, including the applied exchange rate and the published stabilisation value, and reproduces the announcement; it answers “does the arithmetic hold”. Before February 2026 the build-ups contain no stabilisation line at all, so the seventeen pre-stabilisation reviews reconcile with no free term anywhere in the chain. Estimation mode uses only what exists before the announcement: the slate rate from BoZ data, benchmark proxies for P, last month’s premium and fee, and a bracketed S; it answers “what can an outsider know in advance”. Tables 14 and 15 run reconciliation. Table 16 runs estimation. Confusing the two is how outside estimates of this price have gone wrong all year.

F1. The exchange rate.

E = (2 × A1) − A2

F2. The wholesale price, kwacha per cubic metre (one structure, instantiated per product).

Petrol: W = E × (k × P + l × B + C) + S

Diesel: W = E × (k′ × P + l′ × (B + F) + C′) + S

F3. The pump price, kwacha per litre.

Pump = (1.007 × (W + R) + 150) × v ÷ 1,000

F4. The trigger, the algorithm’s last step. Compare W to the prevailing published wholesale price. The pump price moves only if the change exceeds 2.5 per cent in either direction; in a hold, the prevailing price reprints, and your W is the latent series the ERB also publishes. Within a quarter, treat a petrol pin as the base case, rather than a law: the Board has pinned it with S throughout the one completed quarter observed, and reset it at the quarter boundary. A pin also neutralises the trigger: when S is solved to hold W at the prevailing level, the gate sees no change to test.

The structure above is the invariant: it reproduces all twenty-three reviews without exception. The formula never changes; parameter values do, and Table 13 dates every change in the sample.

What the coefficients are made of. Nothing in k, l, C or R is opaque; each is a handful of physical and administered components multiplied out, and every component prints in the ERB’s own build-up. Petrol’s k is the benchmark’s path from a barrel in the Gulf to a cubic metre in Ndola: 8.42 barrels to the tonne, times 1.005 for transportation losses, times 1.005 again for storage losses, times 0.74 tonnes to the cubic metre, so k = 8.42 × 1.005² × 0.74 = 6.293. The premium’s path skips the barrel conversion: l = 1.005² × 0.74 = 0.747. Diesel runs the same anatomy at its own physics: k′ = 7.56 × 1.003² × 0.84 = 6.389 and l′ = 1.003² × 0.84 = 0.845. C is petrol’s fixed dollar costs collapsed to one number: port storage and wharfage, 13.53 together, plus the 210 transport fee, riding through losses and density, plus the 66.51 importer margin riding through storage losses only: C = (13.53 + 210) × 1.005² × 0.74 + 66.51 × 1.005 × 0.74 = 216.5. Diesel’s C′ carries only its port costs, 12.80 × 1.003² × 0.84 = 10.8, because diesel’s transport fee is a monthly variable (F) and its importer margin travels with the tendered premium. R is the kwacha retail stack in one number: terminal fee 62.64, marking fee 204.59, transport to depot 650, OMC margin 2,679.28, dealer margin 2,025.04, plus the product’s excise when in force. v is the VAT factor: 1 while zero-rating holds, 1.16 with VAT restored. If any component ever changes, the repair is one multiplication: replace the component, recompute the letter. The build-up that carries the change re-derives the parameter the evening it prints.

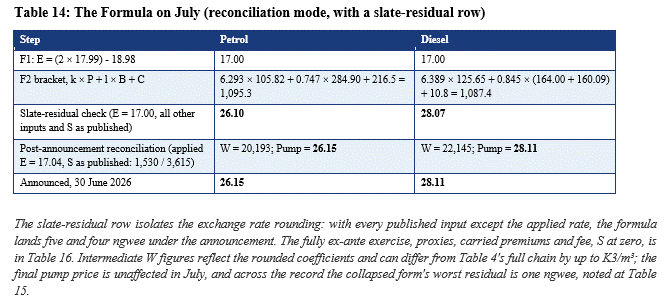

Worked, at July 2026 (k = 6.293, l = 0.747, C = 216.5; k′ = 6.389, l′ = 0.845, C′ = 10.8; R = 5,622; v = 1). Petrol: W = 17.04 × (6.293 × 105.82 + 0.747 × 284.90 + 216.5) + 1,530 = 17.04 × 1,095.3 + 1,530 = 20,193, and Pump = (1.007 × 25,815 + 150) ÷ 1,000 = K26.15. Announced: K26.15. Diesel: W = 17.04 × 1,087.4 + 3,615 = 22,145, and Pump = (1.007 × 27,767 + 150) ÷ 1,000 = K28.11. Announced: K28.11. Two tolerances are worth knowing before running these cold. Run at the computed slate, K17.00, July’s petrol answer is K26.10; run at the applied rate as printed, K17.04, it is K26.15; the five ngwee is the slate-rounding gap, and reconciliation always takes the applied rate. And the collapsed coefficients are rounded consolidations of the schedule values: the full chain of Table 4 reproduces exactly, the collapsed form to within a ngwee at the pump, with intermediate W figures differing from the full chain by up to K3 per cubic metre.

The dollar-chain parameters held across all twenty-three verified months; the kwacha retail stack repriced in October 2024, November 2025 and April 2026, which is why R comes in eras, and Table 13 dates them. There is no fitted parameter anywhere in F1 to F3: the coefficients are the arithmetic of what the ERB already publishes. Any reader holding one build-up can reproduce each of them from Table 13’s derivation column.

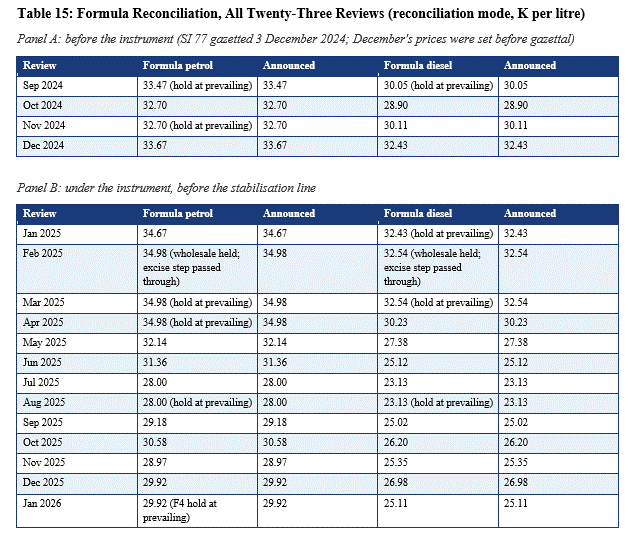

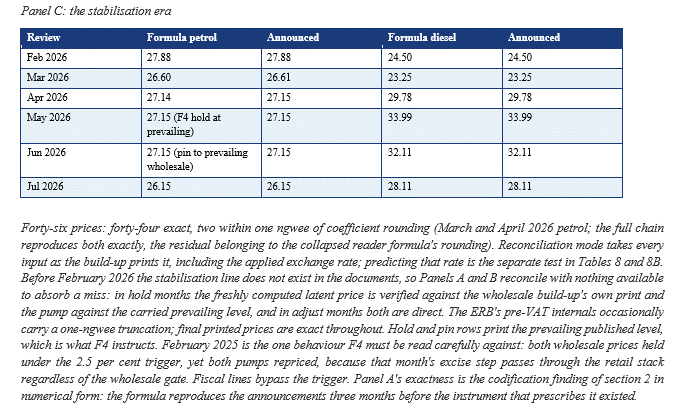

The formula is not fitted to anything. It is the published chain, collapsed. Each constant is an algebraic consolidation of schedule values, individually traceable in Table 13; reproducing the reviews is identification of the mechanism, not predictive validation. Table 15 runs the reconciliation across all twenty-three reviews in three eras: before the instrument, under the instrument before the stabilisation line, and the stabilisation era. Two adjustments apply to the pre-April-2026 reviews: diesel’s premium is the sum of its itemised rows plus that month’s diesel importer margin (Tables 8 and 8B), and February 2026’s stabilisation sat inside the dollar chain, so S is read as the build-up’s own disclosed gap between the pre-stabilisation and wholesale lines. For the reviews before December 2025 the reconciliation runs the full chain at each era’s printed constants; the collapsed coefficients are era-specific algebra, and Table 13 prints every era’s.

Sourcing P without a terminal. The ERB applies the pricing-window average of the Platts assessments, which are subscription data. A reader without a terminal can proxy them from three free daily series published by the EIA. They are mirrored on FRED, the Federal Reserve Economic Data service maintained by the Federal Reserve Bank of St. Louis at fred.stlouisfed.org, and named here in full so a search lands exactly: Conventional Gasoline Prices: U.S. Gulf Coast, Regular (series DGASUSGULF) for petrol; Ultra-Low-Sulfur No. 2 Diesel Fuel Prices: U.S. Gulf Coast (DDFUELUSGULF) for diesel; and Kerosene-Type Jet Fuel Prices: U.S. Gulf Coast (DJFUELUSGULF) for readers extending the method to kerosene, with the one non-window month, June 2026 kerosene, flagged at Table 6. The unit step matters: the series quote US dollars per gallon, and a barrel is 42 US gallons, so multiply the month’s average by 42 for dollars per barrel. The method is then one line: this month’s estimate equals the proxy barrel price plus the most recent month’s differential between the ERB’s applied value and the same proxy. The July run of exactly this method is Table 16’s ex-ante row, where the diesel proxy landed 8.92 dollars above the applied Platts and the differential method carried the estimate to within 23 ngwee of net input error at the pump. This is one-month-ahead testing within the study window: each month’s differential uses only prior months, and no month’s own data enters its own estimate, across seven test months. On that record the proxy lands within about 5 dollars per barrel for diesel and kerosene in calm months (three observations each); petrol is looser, because US gasoline specification seasons can open gaps of up to 15 dollars; and any product can miss by 30 to 40 dollars across a Gulf-specific supply shock (the three crisis months). At the pump that is roughly one kwacha per litre for diesel in calm months, up to two for petrol, and K3 to 5 in a crisis.

Run fully ex-ante on 30 June, public data only, the method gave the July formula prices in Table 16. The residual between a reader’s number and the announcement is, each month, a measurement of the discretionary line; before the announcement that residual also carries the input error, and after it the build-up separates them, because S is printed.

What to do about S, the term with no source. History is the only guide, and Table 5 is the history. Within a quarter, treat petrol as pinned: solve S as whatever residual holds W at its prevailing level, because that is what the Board has done. For diesel, and for petrol at a quarter boundary, set S to zero for the formula price and carry a band of up to K3,700 per cubic metre in either direction, K3.70 per litre, just above the largest magnitude in the record, February’s K3,644 per cubic metre equivalent; future months can print larger. Where the announcement lands inside that band tells you, each month, exactly what the discretionary line did. That is not a forecasting method. It is an accountability instrument. One event can sit inside the residual besides S and input error: a reset of the kwacha retail constants, invisible until the build-up prints it. The record shows three in twenty-three months, each visible the evening it took effect; section 3 carries their dates and sizes, and the November 2025 worked case, a K1.11 residual against a silent statement.

9. What Must Change

The demands below are not transparency for its own sake; they are what the design literature says keeps machines like this one working. The IMF’s technical note on automatic fuel pricing (Coady and others, TNM 12/03, 2012) prescribes what Zambia runs: an explicit formula, published parameters, prices changed at pre-specified intervals, precisely so that pricing cannot be ad hoc. In that design the smoothing gap is never discretionary. Whatever the formula does not pass through must appear as an explicit, rule-computed tax or subsidy line, and the note’s own words carry the standard: “deviations from these should be interpreted as a deviation from the mechanism”. Its assessment of stabilisation funds is equally direct: country experience has been unsatisfactory, with funds regularly exhausted or redirected. The alternative to disclosure is also on display in the region this same year. Kenya’s fuel pricing decisions and its consumer-cushioning levy fund are now before the High Court, after a month of fuel protests, with petitioners demanding the published calculations and fund accounting that Zambia could simply choose to print. Zambia built the textbook machine, and its slate is the textbook’s compliant cost-recovery machinery; the unruled line is the deviation the textbook itself names, and publishing its rule returns the machine to specification.

Five disclosures would close the gap between a transparent document and a transparent system. None obviously requires a new pricing law, though some may require administrative decisions or disclosure protocols.

First, publish the rule, or the absence of one, governing the stabilisation line’s monthly values. The line has printed at four designs, and the K3 of its February press account was never one of them; the ERB itself has stated neither the line’s purpose nor its rule in any document I could locate, and the fullest public account remains a private consultant’s, uncorrected by the regulator for five months. Which gate of Regulation 4 the line entered through is stated in no document I could locate, and Regulation 4(5)’s publication duty applies under either; it has been met in the narrowest possible sense: numbers without a rule. State the gate, state the rule, and publish any extension determination Regulation 4(4) contemplates: if the line entered under 4(2), its duration under 4(3) is one month, it has run six, and no determination appears in the located record. The contrast is the regulator’s own: in the same February, the ERB ran a formal public-comment process on revisions to its uniform pricing guidelines, with published drafts, a structured comment form and a deadline. The stabilisation line received nothing that I could find. Canary Compass will publish, in full, any ERB clarification of the rule governing this line.

Second, publish the energy fund’s balance and monthly flows, and disaggregate its collections by source. The machinery already exists in law: section 44 of the Energy Regulation Act requires proper books of the Fund and an annual audit by the Auditor-General; section 45 requires a report on the Fund’s activities, with an audited statement of financial position appended, laid before the National Assembly within ninety days of year-end; SI 56 requires bank accounts under the Public Finance Management Act and places every disbursement under the Secretary to the Treasury. What the public record shows against that machinery: annual collection totals in the ERB’s annual reports, K405.1 million for 2025 and K363.4 million for 2024, and nothing else. No balance, no monthly flows, no Energy Fund account in the audited financial statements of either year, and no section 45 report in the National Assembly’s tabled records that I could locate.

The naming runs in mirror image: all twenty-three build-ups print Strategic Reserves Fund and never Energy Fund; both annual reports print Energy Fund and never Strategic Reserves Fund; the instrument’s own pump template prescribes Energy Fund; and a parliamentary committee record states the Energy Fund assimilated the SRF. Disaggregation matters because SI 56 directs more than one levy into the Fund and the reports publish one undecomposed number. The disclosure would settle the accumulation’s form: cash remitted to an account, a ledger balance the industry owes back, or money tracked by no one. The 2026 annual report will speak regardless: cash predicts its Energy Fund line printing several multiples of 2025’s K405 million; a ledger predicts no jump at all. It would also show whether the country is running an undocumented slate account. South Africa publishes its Slate Account balance monthly. The precedent is regional and live.

Third, restore the component disclosure of the import premium, and restore the framework whose suspension ended it. The IMF has recommended both. In the four months since the breakdown disappeared, the diesel premium roughly doubled and petrol’s rose by nearly two thirds. Those two facts should not be allowed to remain merely adjacent.

Fourth, publish the administered repricings. The kwacha retail stack has been reset three times in twenty-three months, and the petrol transport fee and excise each moved once; none of the five appeared in a press statement I could locate. The November 2025 event, the largest, ran inside a review of falling wholesale costs and reached consumers unexplained; section 3 carries the record. The margins study behind the recent resets was disclosed where the resets themselves were not. One line in the monthly statement would close this.

Fifth, state the slate arithmetic in every press statement, and state, for every product, the assessment window and the applied benchmark values. The rule is sound cost recovery; publishing its arithmetic each month costs two numbers and a subtraction, and would have answered a question that, this month, was asked publicly and went unanswered. The statements in the reviewed record have named the slate twice, October and December 2025, and shown its arithmetic never; the applied rate itself surfaces in every statement’s airfield price conversion, unidentified as the pricing input. Until these five disclosures are made, the formula in section 8 is the only audit the public has. Every reader now holds it.

Sourcing note. All figures derive from public documents. The core record is the ERB’s monthly press statements and wholesale and pump price build-ups, September 2024 through July 2026: twenty-three consecutive monthly reviews, all independently transcribed and verified. The regulatory text is Statutory Instrument No. 77 of 2024, quoted from the gazette, together with Statutory Instrument No. 56 of 2024, the Energy Regulation (Energy Fund) Regulations, gazetted 27 September 2024, and the Energy Regulation Act, 2019, read in full. The ERB Annual Reports for 2024 and 2025, with their audited financial statements, supply the Energy Fund collection figures; where the two reports differ on 2024, the 2025 report’s restated figures govern. The National Assembly Committee on Energy action-taken record supplies the Energy Fund assimilation statement. Exchange rates are the Bank of Zambia’s published daily retail selling rates (downloadable from 15 September 2025) and its daily interbank rates, from which the pre-archive retail averages in Table 8B are derived and labelled as estimates. Volumes are the ERB 2025 Annual Statistical Bulletin (February 2026), Table 4, with the mid-year press briefing supplying the open-access timeline and the part-year comparatives. Benchmark context uses EIA/FRED daily Gulf Coast product assessments, the EIA Short-Term Energy Outlook (June 2026), the EIA’s published seasonal account of gasoline crack spreads, and contemporaneous market analyses of the post-Hormuz refining slate (Stillwater Associates, May 2026) for the yield-shift observation. The IMF staff statement concluding the 30 April to 13 May 2026 mission (published 14 May 2026) supplies the premium finding, the primary surplus figures, the driver list, the VAT refund backlog observation and the post-election negotiation sequencing. The February 2026 public account of the K3 surcharge is energy consultant Chikwanda’s, in the Zambia Monitor (18 February 2026) and his own Zambia Daily Mail column (24 February 2026). The monthly-yield arithmetic is from the Monitor piece. The quarterly-review intention is traced through News Diggers (2 October 2025) and the ERB Director-General’s end-of-year press briefing (24 December 2025). The briefing also supplies the downstream-margins consultancy disclosure and the framework attribution adjudicated in section 3. The ERB’s February 2026 UPP public-comment notice (13 February 2026) supplies the consultation contrast in section 9. The South African comparison rests on the DMRE’s June 2025 and June 2026 price statements and the Fuels Industry Association of South Africa (June 2026). The design literature cited in section 9 is Coady and others, “Automatic Fuel Pricing Mechanisms with Price Smoothing” (IMF Technical Notes and Manuals 12/03, December 2012), with Kojima, “Fossil Fuel Subsidy and Pricing Policies: Recent Developing Country Experience” (World Bank Policy Research Working Paper, 2016) as the country-experience survey; the Kenyan comparative material is from contemporaneous court and press reporting, April to June 2026. The reconstruction confirms the build-ups are internally exact and reproduces every announced price in all twenty-three reviews. A companion workbook carrying the eight current-era build-ups, the exchange rate series, the proxy series with errors, and the formula derivations accompanies this essay. What is new here, against that public record: the twenty-three-month reconstruction across two margin regimes and the instrument’s gazettal, the finding that the architecture and the slate predate SI 77, the slate decoding against the BoZ retail-selling series with the derived pre-archive extension, the margin-reset record, the tender-arc arithmetic behind the Fund’s premium finding, the collapsed four-line formula with its parameter ledger, the two-designs analysis of the exchange-rate slate, the taxonomy of the stabilisation accumulation’s possible forms, the recapture arithmetic, the breakevens, and the restore-and-pin scenario. Extension chronology and legal status were checked as at 4 July 2026 against the ERB website, ministry statements and available gazette indices. This essay supersedes the counterfactuals in “A Little Here, a Little There” (April 2026) on one point: the April diesel counterfactual excluded the fund’s simultaneous K1.13 per litre support credit, and the stabilisation architecture described here was active, not idle, from February 2026.

Disclaimer

This article does not constitute legal, financial, or investment advice. The author shares views for perspective and discussion only. Do not rely on them as a substitute for professional advice tailored to your specific circumstances. Always consult a qualified legal, financial, investment, or other professional adviser before making decisions based on this content. The analysis reflects proprietary research undertaken by Canary Compass and the author.

Canary Compass and the author accept no liability for actions taken or not taken based on the information in this article.

The views expressed in this article represent the author’s independent professional analysis and do not constitute an endorsement of any individual, institution, or position. Canary Compass and the author accept no responsibility for how this content is interpreted, excerpted, or recontextualised by third parties not involved in its production and publication. Reproducing any portion of this work in isolation, or in combination with other material, in a manner that misrepresents the author’s original meaning constitutes a distortion of the published record.

The author may hold positions in financial instruments, currencies, or assets discussed or referenced in this publication. Such positions do not constitute a recommendation to buy or sell.

All views, projections, and forecasts reflect the author’s assessment at the time of writing. Data sourced from third parties is believed to be reliable but has not been independently verified. Past performance does not indicate future results.

All content published by Canary Compass is the intellectual property of the author. Reproduction, adaptation, or redistribution, in whole or in part, requires written permission.

About the Author

Dean N. Onyambu is the Founder and Chief Strategist of Canary Compass, a financial research publication focused on African monetary architecture and financial sovereignty. He brings 18 years of experience across trading, fund leadership, and economic policy, with senior roles at Standard Bank, First Capital Bank, and Opportunik Global Fund.

Read and subscribe at www.canarycompass.com.

The Canary Compass Channel is available on @CanaryCompassWhatsApp for economic and financial market updates on the go.

For more insights from Dean, you can follow him on LinkedIn @DeanNOnyambu or X @InfinitelyDean.