Zambia Policy Note: The 2026 Refinancing Wall

A retrospective on domestic debt dynamics and the path forward

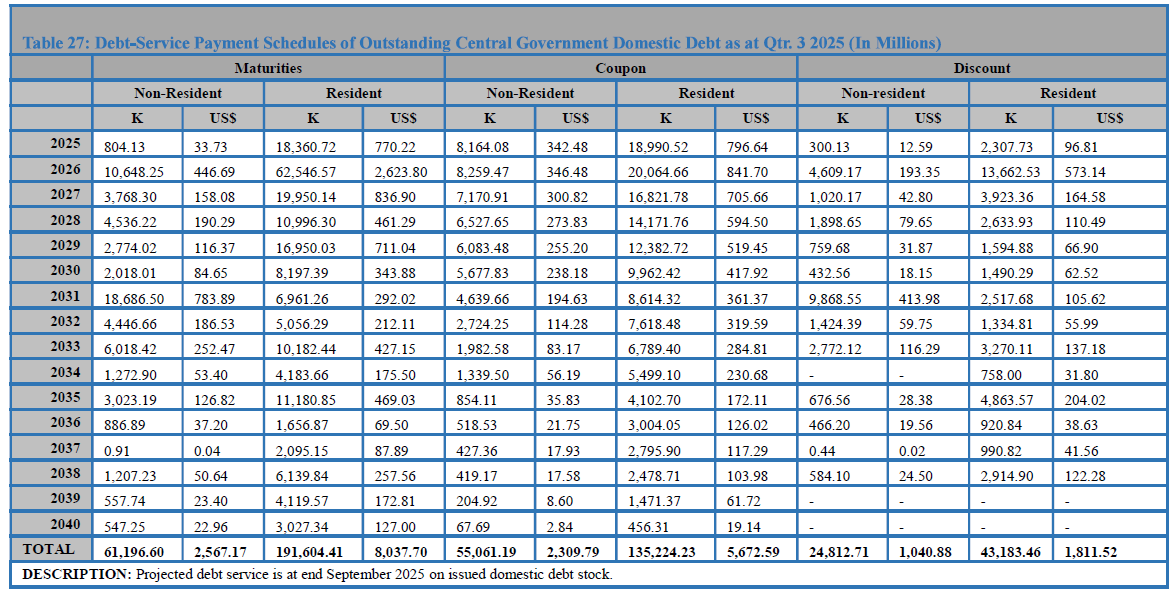

Image: Debt-Service Payment Schedule of Outstanding Central Government Domestic Debt as at end of September 2025 (Source: MoFNP)

0. Executive Summary

On 8 January 2026, the Ministry of Finance confirmed that Zambia will not pursue a one-year extension of the IMF Extended Credit Facility (Reuters, 8 January 2026). Instead, the government intends to conclude the sixth and final review and immediately engage the Fund on a successor programme. This clarification stabilises the intent question but leaves the timing question open.

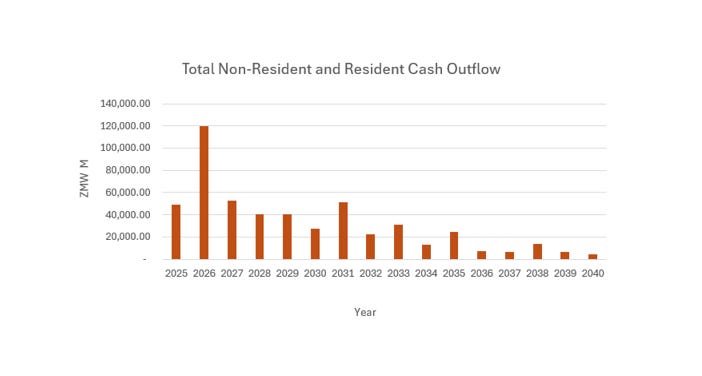

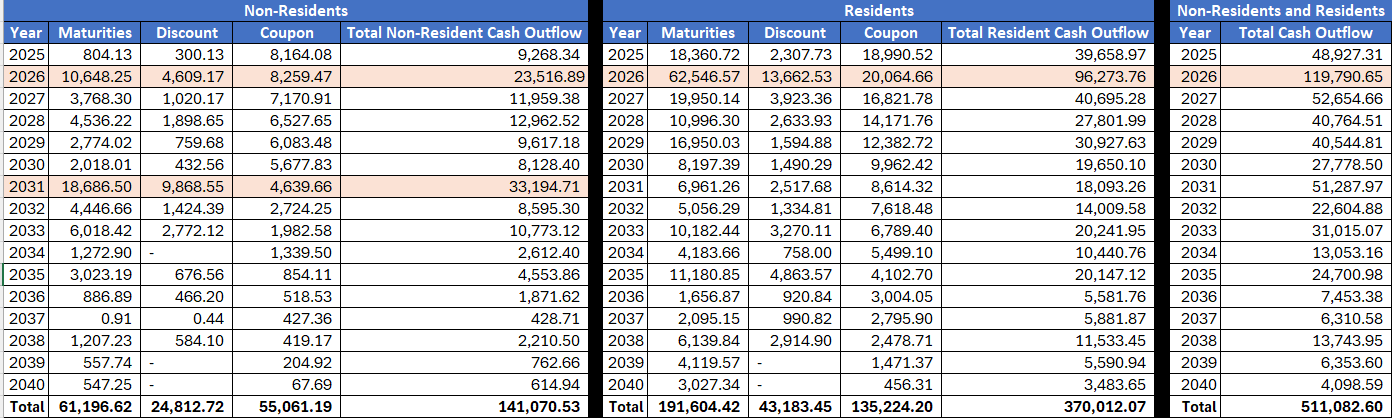

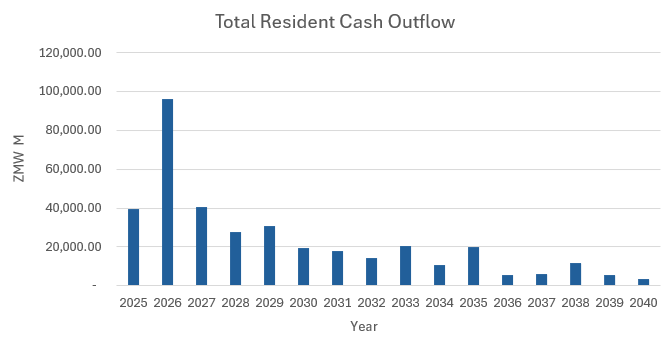

The nature of the refinancing challenge for 2026 remains unchanged. The magnitude, correctly calculated, is larger than our earlier estimates suggested. Total projected domestic debt obligations (maturities, discount and coupon payments) reach ZMW119.8bn. Non-resident obligations amount to ZMW23.5bn (approximately USD1.18bn at a reference rate of USD/ZMW 20, Bank of Zambia daily exchange rate, 7 January 2026), representing 19.6 per cent of total outflows. Resident obligations are four times larger at ZMW96.3bn. These represent different questions. Resident obligations test domestic balance sheet capacity. Non-resident obligations test foreign exchange stability and market confidence. Both matter, but through different channels. The non-resident figure is 25 per cent higher than our earlier estimates that treated maturities at face value rather than at cost.

These maturity walls trace to 2020 and 2021, when the government financed its deficit at yields routinely exceeding 30 per cent, with five-year tenors clearing between 33 and 35 per cent during the post-default period. Five-year bonds issued then mature in 2026. Ten-year bonds mature in 2031.

The hope was always that fiscal consolidation would come fast enough to avoid a restructure of local debt. The IMF programme provided the anchor. The maturity walls remained. The 2026 Annual Borrowing Plan now commits to benchmark bonds and switch auctions to smooth the redemption profile. In economic substance, this is a liability management operation: voluntary exchanges that extend maturities and reshape cash flows. The Ministry frames it as portfolio optimisation. In functional terms, it is a soft restructure of the local bond stock, achieved through switches rather than coercion or principal loss.

The tools are technically appropriate. The sequencing creates political risk that markets must price. Until the successor framework is explicit, markets rationally apply a residual risk premium regardless of intent.

1. The Ministry of Finance Statement

The statement released on 8 January 2026 addresses the Bloomberg report directly. The government is not walking away from the IMF. It is concluding the current programme and pivoting toward a successor arrangement (Reuters, 8 January 2026).

Three elements matter for market pricing.

First, the government frames the decision as programme completion, not disengagement. The current ECF, which began in August 2022, will conclude after the sixth and final review is approved by the IMF Executive Board. The IMF announced the staff-level agreement on the sixth and final review on 18 December 2025 (IMF Press Release No. 25/431). This administration secured and has so far kept an IMF-anchored programme on track through multiple reviews. But programme completion does not eliminate the maturity wall. The bonds issued in 2021 still mature in 2026 and 2031.

Second, the statement commits to strict adherence to the approved national budget during the transition period. Expenditure execution, borrowing, and fiscal balances will remain within Parliament-approved ceilings.

Third, engagement with the IMF will continue through Article IV consultations and other technical dialogue, with discussions on a successor programme to begin immediately after the current programme concludes.

The government could argue that seeking a full successor programme rather than a one-year extension demonstrates greater ambition, not weakened commitment. That interpretation is available. Markets, however, do not price ambition. They price dated frameworks with enforceable conditions. The difference between “we intend to engage” and “we have agreed terms effective [date]” is the difference between direction and anchor. Direction without anchor leaves rollover behaviour exposed to interpretation.

The statement assures that “policy continuity will be underpinned by strict adherence to the approved national budget with expenditure execution, borrowing, and fiscal balances implemented within Parliament-approved ceilings.” But general assurances of strict adherence to the budget are insufficient. Domestic budget ceilings are legally pliable. They can be amended via supplementary appropriations. An IMF programme imposes quantitative performance criteria that cannot be adjusted unilaterally; deviations require formal engagement, waivers, and disclosure. A parliamentary ceiling can be revised by the same parliament that approved it. These are not equivalent constraints, and markets price them accordingly.

2. The Correction: How to Read Table 27

The Ministry of Finance’s Q3 2025 debt service schedules (Table 27) report projected cash outflows on domestic government securities. Reading the table correctly requires understanding what each column means.

Images: Debt-Service Payment Schedule of Outstanding Central Government Domestic Debt as at end of September 2025 (Source: MoFNP)

Table 27 of the Ministry of Finance Q3 2025 debt service schedules uses specific column definitions that determine how cash outflows are calculated. The “Maturities” column reports principal at cost: what the government received when it sold the bond. For discounted instruments such as Treasury bills, cost is less than face value. The “Discount” column reports the implicit interest: the difference between cost and face value. At maturity, the government pays face value, which equals maturities plus discount.

My earlier calculation treated maturities as face value. That understated the 2026 non-resident obligation.

Corrected 2026 non-resident calculation:

Image: Debt-Service Payment Schedule of Outstanding Central Government Domestic Debt as at end of September 2025 (Source: MoFNP)

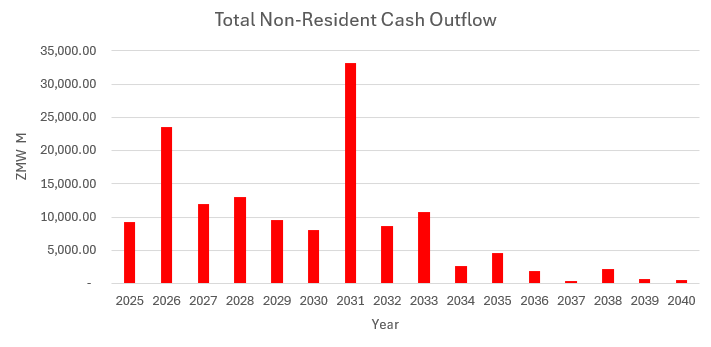

At a reference rate of USD/ZMW 20 (Bank of Zambia daily exchange rate, 7 January 2026), this represents an implied foreign exchange liquidity demand of USD1.18bn. Note that while kwacha depreciation would reduce the dollar-equivalent value of this local currency obligation, it would inversely increase the pressure on foreign exchange reserves should non-residents seek disorderly exit. This is 25 per cent higher than the USD945m I initially calculated.

The 2031 wall is larger still. Non-resident cash outflow that year reaches ZMW33,194.71m (USD1.66bn). Both humps are visible in the attached chart.

Images: Debt-Service Payment Schedule of Outstanding Central Government Domestic Debt as at end of September 2025 (Source: MoFNP)

3. Where These Walls Came From

These maturity concentrations are not random. They trace to 2020 and 2021.

Zambia defaulted in November 2020 when it missed a USD42.5m Eurobond coupon payment. But as I wrote at the time, COVID acted as accelerator, not cause. The fiscal trajectory was unsustainable before the pandemic arrived.

Post-default, the government faced a financing gap with external markets closed. Domestic issuance continued at yields routinely exceeding 30 per cent. Bank of Zambia auction results from November 2020 through March 2021 show five-year tenors clearing between 33 and 35 per cent during this period. Local banks and non-resident investors absorbed the paper. Five-year bonds issued in 2021 mature in 2026. Ten-year bonds mature in 2031.

The banking sector adapted rationally to this environment. Return on equity rose from 13.7 per cent pre-default to 27.8 per cent post-default (Canary Compass analysis, The Imperative for a Bold Approach, November 2023). The advances-to-deposits ratio fell from 51.6 per cent to 38.4 per cent. Commercial bank lending to GRZ climbed from ZMW14.2bn (5.9 per cent of GDP) pre-default to ZMW46.1bn (10.2 per cent of GDP) post-default. I called this “armchair banking” in The Imperative for a Bold Approach (November 2023): profits maximised on the back of fiscal inefficiency, with minimal innovation required.

The new government inherited this structure in August 2021. Non-resident confidence improved as debt restructuring advanced. More capital flowed into longer tenors.

4. What We Said Then

In November 2023, Unraveling Zambia’s Fiscal-Liquidity Nexus stated:

“The crux of Zambia’s liquidity is traceable to the government’s net domestic financing activities. The borrowings in previous years, notably before FY2022, specifically FY2020 and FY2021, set the stage for the significant maturities we observe today. Each year, as the government seeks to finance its obligations, it enters the market for fresh borrowings, thereby increasing the net issuance. This cyclical pattern has not only sustained but also exacerbated the liquidity situation.”

And:

“Looking ahead to the 2024 fiscal year, based on current projections, the net issuance for the upcoming financial year will likely increase... Unless net external financing overperforms, such an escalation will only further entrench the cycle of Kwacha borrowing and liquidity influx.”

In December 2025, Structure Before Sentiment Part 3 stated it plainly:

“As we argued as far back as 2022, slow fiscal consolidation was always going to find its reckoning in 2026, when a heavy cluster of local bond maturities comes due.”

5. What We Hoped For

The bet was always that fiscal consolidation would come fast enough to avoid a restructure of local debt. The IMF programme provided the anchor. External debt restructuring concluded. Copper prices held. Reserves rebuilt to USD5.2bn, equivalent to 5.2 months of import cover by end September 2025 (Bank of Zambia). The Bank of Zambia spent 2025 rebuilding credibility. The revised Currency Directives took effect on 26 December 2025 (Bank of Zambia Statutory Instrument), re-enforcing the legal requirement that domestic transactions must be settled in Zambian Kwacha, with exemptions for mining, tourism, electricity, financial products with foreign currency components, and exports and imports. Inflation is decelerating.

Credit metrics have improved. Fitch Ratings upgraded Zambia to B- in the second half of 2025. Debt-to-GDP is projected to fall below 100 per cent by end-2026. These gains are real. They do not, however, eliminate the maturity concentration. A healthier patient still faces surgery if the tumour remains.

6. What Is Happening Now

The 2026 Annual Borrowing Plan commits to benchmark bonds and switch auctions. The Ministry frames this as portfolio optimisation and redemption smoothing.

In economic substance, this constitutes a liability management operation that reshapes the duration profile of the domestic debt stock. The mechanism is voluntary exchange rather than coercive loss. The effect is maturity extension. Whether one calls this “portfolio optimisation” or a soft restructure depends on perspective. What cannot be disputed is that it changes the timing and shape of cash flows owed to bondholders. The state presents this as redemption smoothing. The market may read it as confirmation that the original maturity profile was unserviceable at fiscal-neutral terms.

This was always the alternative to faster consolidation. The state cannot roll a fragmented bond stock at crisis prices indefinitely. It must either pay down the wall through surplus, or reshape it through exchanges. Zambia chose the latter.

Switch auctions address the resident refinancing question better than they resolve non-resident rollover behaviour. If foreign holders exit rather than exchange into longer tenors, domestic institutions become the marginal buyer by default, not by design. The ZMW96.3bn resident obligation and the ZMW23.5bn non-resident obligation are therefore two distinct problems. The first tests domestic balance sheet capacity. The second tests foreign exchange stability and market confidence. Both matter, but through different channels and with different policy tools.

Narratives of programme graduation assume the crisis is resolved. The maturity profile does not support that assumption. The bonds are legacy. The maturities are not. The 2026 wall is a present constraint that shapes every policy option available to both Treasury and the central bank.

7. The Anchor Question

The liability management tools are technically appropriate. The timing raises questions.

The question is not whether Zambia plans to engage the IMF again. The question is the timing, sequencing, and binding nature of that engagement in an election year with concentrated rollover exposure. The absence of clarity on these points leaves uncertainty that markets must price.

Remaining committed to a reform path during a transition period is not the same as operating under an active programme. The deeper problem is incentive structure, not document status. Governments facing elections have a structural tendency toward time inconsistency: promise discipline now, spend later. Markets do not price the press release. They price the incentive mismatch between pre-election commitments and post-election behaviour. An IMF programme does not eliminate this mismatch, but it raises the cost of deviation through external monitoring and disclosure requirements.

Article IV consultations are surveillance tools. They do not impose enforceable fiscal constraints, nor do they materially alter investor rollover behaviour when uncertainty rises. The signalling value that matters to markets comes from an agreed framework with dates, conditions, and monitoring.

The absence of a timeline is therefore not a neutral omission. Without clarity on whether a successor programme is pursued before the election or deferred until after, the risk premium remains. Ambiguity can be read as preserving discretion during the electoral cycle, with re-anchoring postponed until later. That interpretation may or may not be correct, but it is the one markets are forced to price in the absence of guidance.

As Ken Opalo notes in his 2026 Africa outlook, Zambia faces “a tough reelection battle” with projected growth that “may not be enough.” Rollovers are not politically neutral. They are contingent decisions made by investors who read electoral signals, policy continuity markers, and institutional stability indicators. The concentration of maturities in an election year is not a coincidence to be managed. It is a constraint that shapes the bargaining position of both sovereign and creditor. This is not conspiracy. It is standard portfolio management under uncertainty.

This matters because rollover needs this year are not trivial. Non-resident participation remains an important marginal buyer of government securities. As at end September 2025, non-residents held 30.20 per cent of government bonds (ZMW61.2bn), though they held no Treasury bills. The private issuance dynamics of 2021, centred on three-year, five-year, and ten-year tenors, mean non-resident holdings are disproportionately concentrated in bonds maturing in 2026 and 2031. Confidence in rollover behaviour depends less on backward-looking benchmarks and more on forward-looking constraints.

Markets have seen IMF engagement signalled without delivery before. They will treat vague intent as cheap talk regardless of which administration states it. The question is not whether this government is more credible than its predecessor. The question is whether the signal is specific enough to anchor pricing.

8. The Geopolitical Dimension

As Ken Opalo observes, “a disorganized world with competing major and middle powers that have no time for norms or international law will be a dangerous world for the geopolitically naive.” Rollovers are not just financial decisions. They are increasingly shaped by geopolitical context.

Yuan-denominated mining tax payments began in October 2025, making Zambia the first African sovereign to accept renminbi for mining royalties. Finance Minister Situmbeko Musokotwane said at a 6 January 2026 briefing, as reported by Lusaka Times, that yuan accounted for approximately 2 per cent of mining taxes in 2025, with 15 per cent expected in 2026. The Minister framed this as debt service efficiency, noting that most Chinese loans were denominated in renminbi, not dollars, rather than as a monetary policy shift. The Bank of Zambia began publishing official renminbi-kwacha exchange rates in December 2025 to facilitate settlement.

The pending health partnership signatures with the United States remain unresolved. Zambia’s positioning grows more ambiguous at precisely the moment it can least afford ambiguity.

Non-resident rollover decisions are risk-adjusted, not diplomatic. Western institutional capital does not exit to send a geopolitical message; it exits when the policy environment becomes unreadable and risk-adjusted returns turn negative. The issue is not that investors punish Zambia for engaging China. There are, however, two distinct risk channels at work. The first is implicit political risk pricing: investors may price the tail risk that deeper alignment with Beijing could affect dollar clearing access, US regulatory treatment, or the trajectory of multilateral support. This is not punishment; it is risk adjustment for plausible adverse scenarios. The second is uncertainty pricing: investors cannot model where Zambia sits on the geopolitical spectrum, so they apply a wider risk band to compensate for the unreadable. Both channels widen the premium. Neither requires malice. A clear tilt toward Beijing would be priceable. A clear anchor with the Fund would be priceable. Strategic ambiguity is not.

Alternative bilateral liquidity arrangements, including currency swaps, resource-backed facilities, and renminbi credit lines, could in principle change the sovereign’s options. None are currently in place at the scale required to address 2026 maturities. Chinese institutional capital could theoretically absorb some of the non-resident exit, but has historically shown limited appetite for local currency exposure in frontier markets. The analysis assumes the existing investor base and funding architecture. If that architecture shifts materially, the calculus shifts with it. Such a shift is not visible on the current horizon.

Part 4 addressed this directly:

“With material non-resident ownership of bonds, large maturity walls can translate into FX pressure if exits are disorderly or rollovers fail. That is why benchmark building, switch auctions, and liability-management operations are not optional plumbing. They are sovereign risk management.”

Given an investor base skewed toward Western institutions, what contingency planning exists if market behaviour becomes explicitly geopolitical rather than purely risk-based?

9. The Central Bank Bind

Parts 3 and 4 of the Structure Before Sentiment series prescribed a structural reform programme for the Bank of Zambia. The toolkit included concentration-based risk weights under Statutory Instrument 62 to penalise banks for excessive sovereign holdings, an inverted Countercyclical Capital Buffer that releases capital only when banks expand private credit, and conditionality on Deposit Insurance Fund liquidity releases tied to private sector loan-to-deposit targets. These instruments would, over time, break the sovereign-bank nexus that blocks monetary transmission.

The logic was clear. As at end September 2025, commercial banks held government securities equivalent to approximately 51 per cent of local currency deposits (Structure Before Sentiment Part 2.75). True kwacha-originated private credit stood at only 7.4 per cent of GDP, and total private credit at 13.6 per cent, reaching roughly 10 per cent of firms. The top 20 borrowers absorbed 60 to 65 per cent of the loan book. Banks earned return on equity near 30 per cent with a loan-to-deposit ratio of approximately 46 per cent. The Journey of K100 showed that of every new kwacha deposit, roughly 26 per cent is immobilised as reserves, more than 50 per cent supports government securities directly or through collateral loops, and only a filtered residual reaches the broad private economy.

The reforms assumed fiscal consolidation would create space for transmission reform. The 2026 refinancing wall challenges that space.

The ZMW96.3bn resident maturity wall already requires domestic banks to absorb at scale. If non-residents exit rather than roll, the burden increases further. Either way, the Bank of Zambia faces a near-term trade-off. Imposing concentration risk weights that penalise sovereign holdings becomes politically and practically difficult when the state depends on those holdings for funding. Releasing liquidity through lower reserve requirements risks channelling that liquidity straight into government securities, deepening the nexus rather than breaking it.

The sovereign-bank nexus has shifted from a transmission problem to a financing requirement. In 2020, banks chose government paper because the risk-adjusted returns were superior. In 2026, the state needs them to keep choosing it. What we called “armchair banking” was a critique of profitable inefficiency. It is now a dependency the Treasury cannot do without.

The consequences compound. The Journey of K100 worsens. Crowding out intensifies. Inflation risk rises. Kwacha pressure returns. The reforms outlined in Parts 3 and 4 remain the correct long-term direction. The refinancing wall delays their implementation; it does not invalidate their necessity. They become difficult to implement while the sovereign depends on the nexus for survival. But they remain the path to a transmission mechanism that actually works.

Who, then, is the responsible partner?

This is a fiscal problem, not a monetary one. Switch auctions are the correct tool, but they require credibility. That credibility comes from IMF cover or demonstrated fiscal discipline, not from the Bank of Zambia releasing liquidity to fund government paper. If the Ministry expects the central bank to ease reserve requirements to provide refinancing capacity, it is asking the Bank of Zambia to sacrifice transmission reform for fiscal convenience. That path leads to deeper nexus, worse K100 journey, continued crowding out, and a monetary policy signal that remains blocked by structure long after the refinancing wall has passed.

10. Three Governance Questions

The questions that remain are straightforward.

1. Is the Debt Management Office confident that non-resident rollover behaviour will hold without the signalling value of an active IMF programme?

2. Do domestic institutions have sufficient balance sheet depth to absorb ZMW96.3bn in resident obligations plus any non-resident supply that does not roll, without destabilising yields, liquidity, or the exchange rate?

3. Is the successor framework intended as a pre-election stabiliser or a post-election re-anchoring mechanism after fiscal expansion? Without clarity on sequencing, the distinction between discipline and discretion becomes blurred.

11. Closing

If the objective is to stabilise expectations, the path forward is straightforward. Clarify whether engagement with the IMF is expected before or after the election. Specify the interim fiscal stance in quantitative terms, including adherence to the approved budget deficit and borrowing ceilings. Explain how discipline will be enforced in the absence of an active programme, particularly in managing rollover risks on non-resident domestic debt.

Until then, statements of intent will struggle to move the needle.

Government can signal continued IMF engagement. That is not the same as having a programme in place.

An election window with a refinancing hump is not inherently dangerous. But it requires an anchor markets can price.

The pudding will be judged by its texture, not the recipe.

References

Primary Sources

Ministry of Finance and National Planning, Statement on IMF ECF Arrangement, 8 January 2026

Ministry of Finance, Medium Term Debt Management Strategy 2025-2027 (Table 27: Debt-Service Payment Schedules)

Bank of Zambia, Debt Statistical Bulletin Q3 2025 (Tables 24, 25, 27)

Bank of Zambia, Daily Exchange Rates, 7 January 2026. Available at: https://www.boz.zm

Bank of Zambia, Government Securities Auction Results, November 2020 to March 2021

Ministry of Finance, 2026 Annual Borrowing Plan

Bank of Zambia, Financial Stability Report Q3 2025

Bank of Zambia, Statutory Instrument on Currency Directives, December 2025

IMF, Sixth ECF Review Staff-Level Agreement Press Release (PR/25/431), 18 December 2025. Available at: https://www.imf.org/en/news/articles/2025/12/18/pr-25431-zambia-imf-reaches-agreement-on-6th-and-final-rev-of-ecf

Fitch Ratings, Zambia Rating Action, 2025

Reuters, “Zambia to work with IMF on new programme,” 8 January 2026

External Commentary

Opalo, K. (2026) “Africa in 2026: The 11 trends/factors that will shape African affairs in 2026,” An Africanist Perspective, January 2026. https://www.africanistperspective.com/p/african-in-2026

Lusaka Times, “Government clarifies use of Chinese currency in mining tax payments,” 6 January 2026

Canary Compass Series

Onyambu, D. (2023) “The Imperative for a Bold Approach by the Bank of Zambia as Zambia Continues to Navigate Post-COVID/default Challenges,” Canary Compass, November 2023. https://canarycompass.substack.com/p/the-imperative-for-a-bold-approach

Onyambu, D. (2023) “Unraveling Zambia’s Fiscal-Liquidity Nexus: The Imperative for Another Aggressive SRR Hike Amidst Policy Complexities,” Canary Compass, November 2023. https://canarycompass.substack.com/p/unraveling-zambias-fiscal-liquidity

Onyambu, D. (2025) “Zambia Monetary Policy. Structure Before Sentiment. Part 1: Decision Week,” Canary Compass, November 2025. https://canarycompass.substack.com/p/zambia-monetary-policy-structure

Onyambu, D. (2025) “Zambia Monetary Policy. Structure Before Sentiment. Part 2.75 Interlude: Recap, Corrections, and the Journey of K100,” Canary Compass, December 2025. https://canarycompass.substack.com/p/zambia-monetary-policy-structure-664

Onyambu, D. (2025) “Zambia Monetary Policy. Structure Before Sentiment. Part 3: Foundations for Transmission,” Canary Compass, December 2025. https://canarycompass.substack.com/p/zambia-monetary-policy-structure-092

Onyambu, D. (2025) “Zambia Monetary Policy. Structure Before Sentiment. Part 4: The World Will Not Wait,” Canary Compass, December 2025. https://canarycompass.substack.com/p/zambia-monetary-policy-structure-e7c

Disclaimer

This article does not constitute legal, financial, or investment advice. The author shares views for perspective and discussion only. Do not rely on them as a substitute for professional advice tailored to your specific circumstances. Always consult a qualified legal, financial, investment, or other professional adviser before making decisions based on this content. The analysis reflects proprietary research undertaken by Canary Compass and the author.

Canary Compass and the author accept no liability for actions taken or not taken based on the information in this article.

About the Author

Dean N. Onyambu is the Founder and Chief Editor of Canary Compass. His insights draw on experience across trading, fund leadership, governance, and economic policy.

The Canary Compass Channel is available on @CanaryCompassWhatsApp for economic and financial market updates on the go.

Canary Compass is also available on Facebook: @CanaryCompassFacebook.

For more insights from Dean, you can follow him on LinkedIn @DeanNOnyambu, X @InfinitelyDean, or Facebook @DeanNathanielOnyambu