Zambia’s Kwacha: Short-Term Resilience, Long-Term Questions

Chart Source: Bloomberg

The Kwacha's recent appreciation to approximately 26.650 from levels near 29 has attracted significant interest. I have not tracked the Kwacha closely since authorities raised the tradable narrow-spread threshold to $5 million. More recently, new legislation, particularly the Cyber Security Act No. 3 of 2025 and the Cyber Crimes Act No. 4 of 2025, has introduced legal complexities that have made public economic commentary more difficult.

In a country contributing barely 0.03 percent to global GDP, macroeconomic perspectives that differ from the official fiscal narrative may now attract legal scrutiny. The Ministry of Finance and National Planning [MoFNP] and the Bank of Zambia [BoZ] should consider issuing clear and consistent guidance on acceptable public financial analysis, especially for professionals engaging in non-partisan, evidence-based discourse.

Global Context

The Kwacha's appreciation reflects broader global patterns of U.S. dollar softness and selective capital inflows into emerging markets, though distinct underlying factors drive each.

Recent weakness in the U.S. dollar stems primarily from positioning unwinds and market recalibrations around U.S. interest rate expectations. Investors have pared back overweight USD exposures amid shifting global risk sentiment and signs of moderating economic momentum in advanced economies.

In parallel, selective capital has flowed into emerging markets as investors search for yield and portfolio diversification, particularly in countries exhibiting external account resilience or relative macroeconomic stability. Zambia has benefited from improved mining-related inflows, which have supported the Bank of Zambia's foreign exchange operations and contributed to Kwacha's stability; this has occurred alongside relatively subdued dollar demand from the energy sector within the FX market.

However, the currency's recent strength does not reflect a structural improvement in Zambia's underlying fundamentals. Rather, it presents an opportunity to accumulate USD at more favourable levels. Historically [since the dollarization of mining taxes in June 2020], the Kwacha depreciates in multi-month cycles, occasionally interrupted by sharp reversals before reverting to its long-term trajectory. The current divergence between the onshore rate, around 26.650, and the offshore rate, near 27.00, suggests that external investors may share this view. Following the bond market rally, some near-term profit-taking by offshore investors is a rational expectation.

Domestic Fundamentals

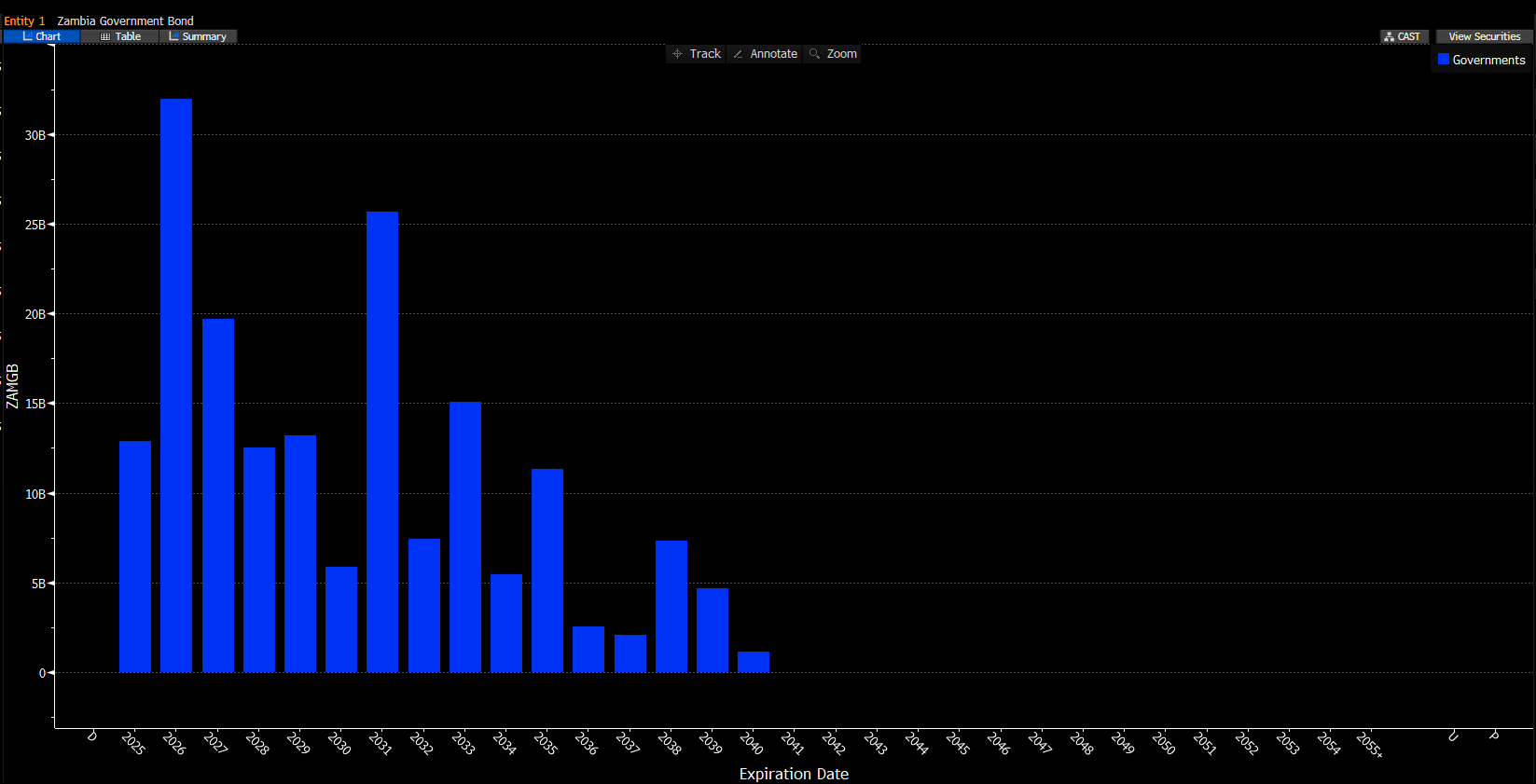

Zambia continues to face acute debt stress on both external and domestic fronts. In 2026, domestic bond maturities currently stand at ZMW 31.955 billion. As of May, Treasury Bills add another ZMW 14.663 billion to the rollover burden, and this figure will likely rise with continued issuance in 2025.

These maturity pressures stem primarily from the borrowing cycle of 2021 under the previous administration. Unless policymakers act preemptively, Zambia may need to reprofile its domestic debt. While politically sensitive, such an outcome now represents a material and rising risk. A structured reprofiling, executed well before the first quarter of 2026, could help mitigate systemic stress and prevent disorderly rollover dynamics in the local market.

Any reprofiling effort will need to balance financial stability with political and social considerations. Pensions and retail investors are likely to be exempted to preserve public confidence and avoid broader market panic. This will place the adjustment burden on institutional holders, particularly commercial banks.

That burden, however, reflects the concentration of benefits. Commercial bank holdings of domestic government securities rose from ZMW 19.30 billion at the end of 2019 [6.42% of GDP] to ZMW 30.15 billion at the end of 2020 [9.08% of GDP], ZMW 34.75 billion in 2021 [7.86% of GDP], and ZMW 43.90 billion by the end of 2022 [8.89% of GDP]. Over the same period, credit extension to the private sector remained relatively subdued. Banks have profited from government paper while largely stepping back from real sector lending. Authorities must now be willing to test the resolve of the banking sector. If banks are not lending to the private sector and have become dependent on government securities [and lending], their claim to systemic fragility under restructuring loses credibility.

To anchor investor confidence and preserve macro-financial stability, any reprofiling should form part of a broader adjustment package. A clearly sequenced and credible IMF-supported programme would help reinforce expectations around fiscal restraint, inflation management, and future debt issuance discipline.

While Zambia has taken steps to establish fiscal anchors through the Public Debt Management Act of 2022, particularly by requiring parliamentary approval for the Annual Borrowing Plan and setting limits on debt accumulation, key operational tools remain absent. The Act does not provide for binding expenditure ceilings or enforceable debt service caps. To strengthen fiscal credibility and improve investor confidence, policymakers should move beyond legislative intent and formalise these anchors within a transparent, rules-based fiscal framework. A credible and enforced anchor would support long-term policy discipline, reduce uncertainty across the sovereign yield curve, and help stabilise market expectations following any debt restructuring.

Policy Coordination and Inflation Dynamics

Zambia's fiscal and monetary policies remain poorly coordinated. This disconnect may widen as the government enters a period typically associated with elevated public expenditure. If fiscal expansion proceeds without corresponding monetary tightening or anchoring, macroeconomic instability may return, particularly in an election-adjacent period.

Much of the inflationary pressure observed since mid-2019 has stemmed from fiscal-driven demand expansion, backed by growth in the money supply rather than private sector productivity. Elevated government outlays have coincided with liquidity injections that have complicated inflation control and undermined policy credibility.

Although headline inflation declined to 16.5 percent in April 2025, it remains far above the Bank of Zambia's 6 to 8 percent target range. Inflation has exceeded this upper bound since April 2019, averaging 14.4 percent over the past six years. This persistent inflation has eroded household purchasing power, compressed real wages, and intensified cost-of-living pressures. A short-term moderation in consumer prices cannot reverse these cumulative effects.

Any durable fiscal adjustment strategy must also place a ceiling on public sector credit extension by the domestic financial system. Without this, Zambia risks repeating a domestic debt spiral that undermines macroeconomic stability and investor confidence.

External Buffers and IMF Programme Outlook

Zambia's international reserves reached a record high of $4.31 billion in December 2024, providing 4.6 months of import cover [the BoZ's most recent fortnightly statistics report puts the figure at $4.29 billion]. These reserves offer meaningful space to manage exchange rate volatility but cannot substitute for coherent policy alignment. External concessional financing remains structurally constrained, and Zambia has only recently resumed debt service payments following its restructuring.

Later this year, the IMF's Extended Credit Facility [ECF] expires. Whether Zambia transitions smoothly into a successor programme will serve as a critical signal for markets and development partners. Any delay may indicate political hesitation, particularly if authorities prefer to defer structural reforms until after the August 2026 elections.

If IMF engagement lapses, investors could question Zambia's policy commitment and financing assurances, particularly among bilateral and commercial creditors. The government should clarify its intentions regarding programme continuity and publish a credible roadmap before the current facility expires.

De-dollarization Trajectory

The BoZ has made significant progress in preparing for a de-dollarization pivot. Measures such as foreign exchange trading caps, tighter import payment rules, and enhanced export revenue frameworks indicate clear policy intent.

Authorities intend to introduce these measures to encourage local currency use, reduce balance sheet dollarization, and restore monetary policy effectiveness. The critical question now concerns the timing and credibility of execution.

Policymakers must decide whether to implement de-dollarization before or after the 2026 elections. Success will depend on effective sequencing, sustained private sector confidence, and a transparent local currency framework regardless of timing. Avoiding widespread exemptions is essential to prevent arbitrage, loopholes, and credibility loss.

Final Thoughts

While the Kwacha's recent appreciation provides short-term relief, Zambia's deeper fiscal and structural vulnerabilities remain unresolved. The sustainability of the currency's strength will depend on external market dynamics and internal policy coherence.

Over the next 12 to 18 months, three questions will shape Zambia's macroeconomic trajectory:

Will authorities confront the fiscal realities that lie ahead?

Will Zambia secure a successor IMF programme before year-end?

Will de-dollarization move from policy framework to implementation, and when?

Dean N Onyambu is the Founder and Chief Editor of Canary Compass, a co-author of Unlocking African Prosperity, and the Executive Head of Treasury and Trading at Opportunik Global Fund (OGF), a CIMA-licensed fund for Africans and diasporans (Opportunik). Passion and mentorship have fueled his 17-year journey in financial markets. He is a proud former VP of ACI Zambia FMA (@ACIZambiaFMA) and founder of mentorship programs that have shaped and continue to shape over 50 financial pros and counting! When he is not knee-deep in charts, he is all about rugby. His motto is exceeding limits, abounding in opportunities, and achieving greatness. #ExceedAboundAchieve

The Canary Compass Channel is available on @CanaryCompassWhatsApp for economic and financial market updates on the go.

Canary Compass is also available on Facebook: @CanaryCompassFacebook.

For more insights from Dean, you can follow him on LinkedIn @DeanNOnyambu, X @InfinitelyDean, or Facebook @DeanNathanielOnyambu.